- The Bank of Canada delivered a hawkish hold…

- ...aided by spiking oil prices amid escalating Iran risks

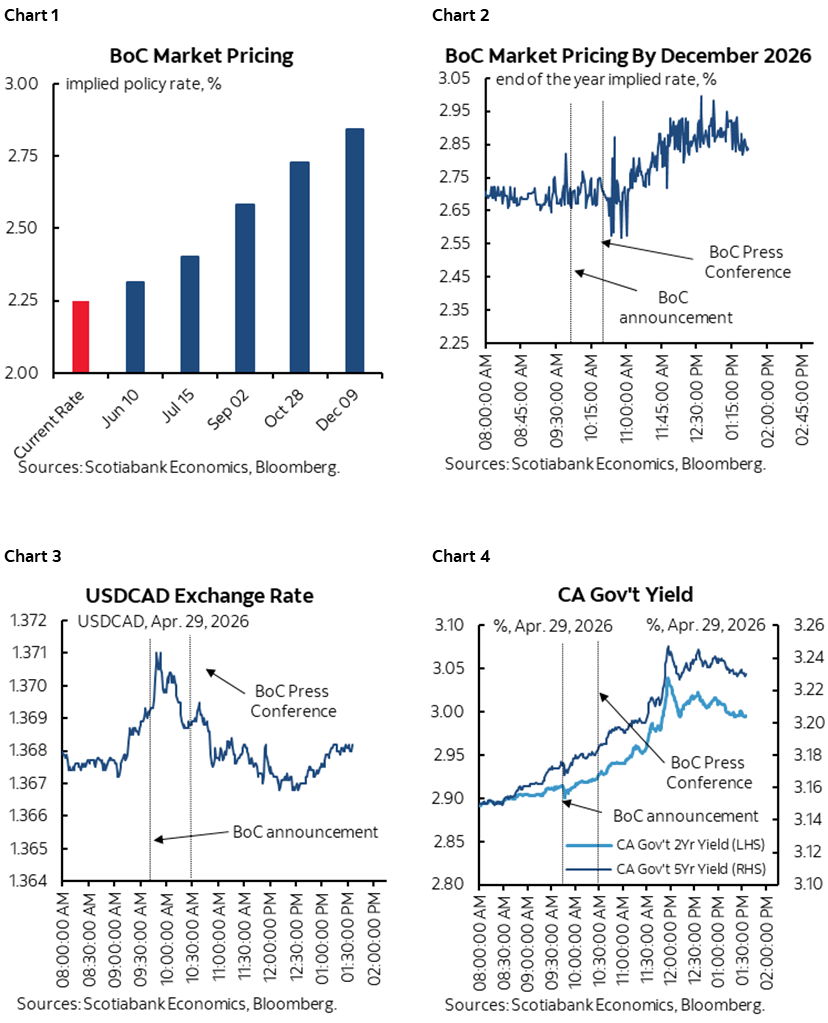

- Markets are pricing a decent shot at a July hike, between 50–75bps by year-end…

- ...in keeping with our long-held forecasts

- This was a placeholder, with plenty of room for seeing things differently

The BoC left its overnight rate unchanged at 2.25% as unanimously expected and priced. The bias was incrementally hawkish in my view and especially when reasonable views around several of their arguments are presented. The statement is here, Governor Macklem’s opening remarks are here, and the MPR with forecasts is here.

I’ll do my best to present highlights of the BoC’s fresh case but with the strong caveat that I’ll work into key areas of what follows where I don’t believe their communications. I think they’re buying time. I think their communications are stale on arrival. The journalists in the presser failed to ask the obvious money questions; perhaps the BoC should open up the field. The Governor exited stage left far too easily.

Nevertheless, markets couldn’t really have cared less about the BoC’s communications. They’re chasing higher oil prices that are on fire. WTI and Brent are up about US$7–8 on a bet that war may be back on, if it ever subsided. This is partly fed by resistance remarks by Iran’s parliament speaker Ghalibaf that makes it increasingly clear that both sides are digging in for the longer haul. Trump rejected Iran’s offer to open the Strait and talk about nuclear program options later and Axios reported from three anonymous sources that the US is considering a “short and powerful” wave of strikes.

Accordingly, the post-communications market reactions are mixing market pricing of oil impacts and BoC communications while treating the latter as stale on arrival. July is now 50–50 priced for a BoC hike. June is not a base case at this point, but is underpriced in my opinion; six more weeks of this and it will be harder for Macklem & Co to sit tight and the BoC doesn’t have to have an MPR to move. Volatile markets are swinging between pricing about 55–70bps of our 75bps of forecast hikes by year-end. Our 2026H2 hike forecast that we’ve had since November and that we added to in March has made money for clients who listened.

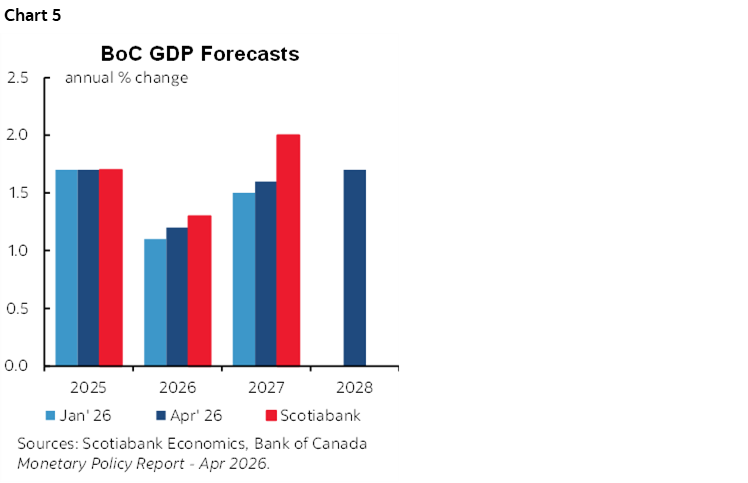

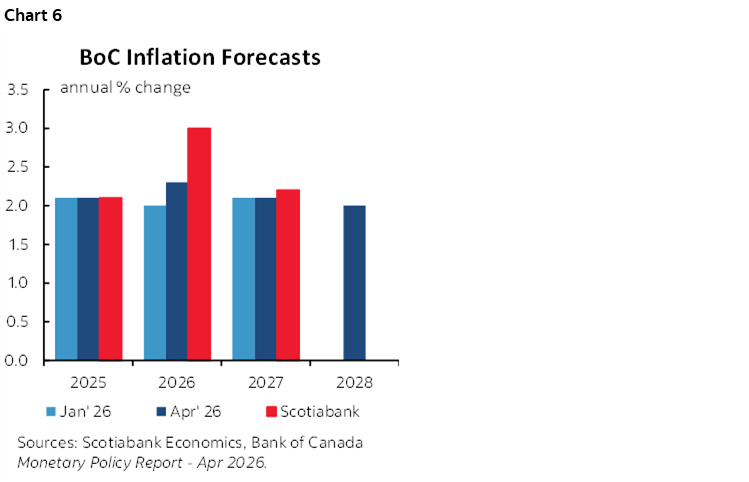

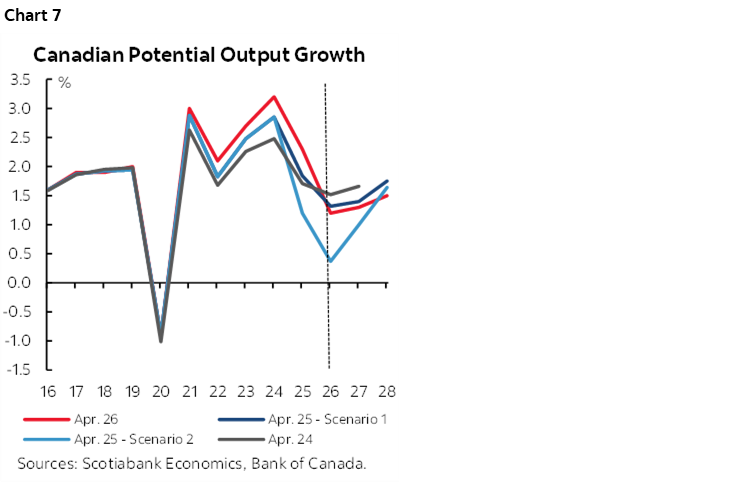

Charts 1–4 show market pricing for the BoC’s policy rate at the point of publishing, and the intraday market moves in Canadian rates and CAD.

WHAT THEY DID

GDP growth was little changed in their fresh projections (chart 5). They see GDP up 1.2% y/y this year (1.1% in the January MPR) and growth at 1.6% next year (from 1.5%).

In fact, the compositional change in their forecasts was more bearish than the headline. That’s because to keep GDP growth little changed, they added 0.4 ppts to 2026 GDP growth from inventory contributions which implies they downward the rest of the growth picture. I’ll come back to this. Still, they sounded more negative on the underlying domestic economy and net trade where they revised export growth contributions down a bit and import leakage effects higher.

The BoC revised up inflation this year, but only a bit from 2.0% to 2.3% y/y. They left inflation unchanged at 2.1% next year. Chart 6.

They left potential GDP growth little changed on balance compared to prior estimates (chart 7).

The statement was a convoluted mixture of forecasts and guidance as per the norm for an MPR meeting. See the appendix. I don’t think the statement changes were the key feature of their guidance relative to forecasts and relative to the next part.

MACKLEM TALKS HIKES AND CUTS

It was the Governor’s written opening remarks that were somewhat more impactful than the statement. In it, he spoke of two tail risks to the policy rate outlook.

“If the United States imposes significant new trade restrictions on Canada, we may need to cut the policy rate further to support economic growth. Alternatively, if oil prices continue to increase, and particularly if they remain elevated, the risk that higher energy prices become ongoing generalized inflation increases. If this starts to happen, monetary policy will have more work to do—there may be a need for consecutive increases in the policy rate.”

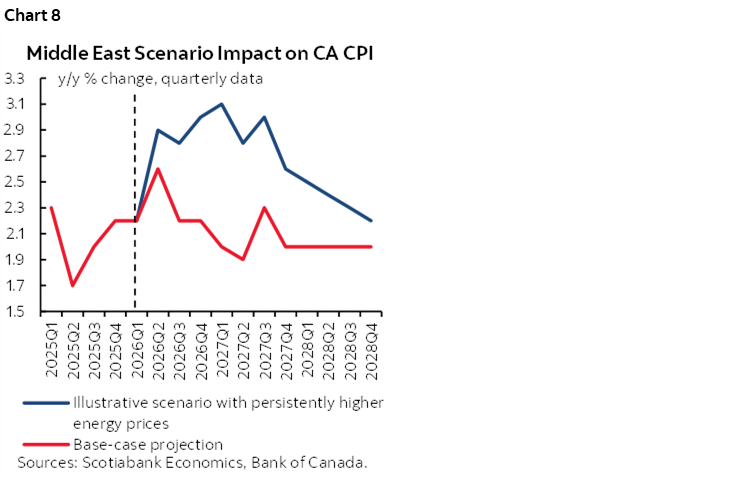

Macklem also noted "However, uncertainty is unusually elevated, and there are many possible outcomes. " Chart 8 shows their control-shock scenario of higher energy prices for longer.

Still, Governor Macklem’s opening of the door to future rate changes introduced optionality that was less evident in prior communications. It’s clear their head is in risk management mode and that the probability of a rate change of some sort is higher, leaving it up to you and I to determine direction and magnitude. I’ll return to which end of the spectrum is most likely.

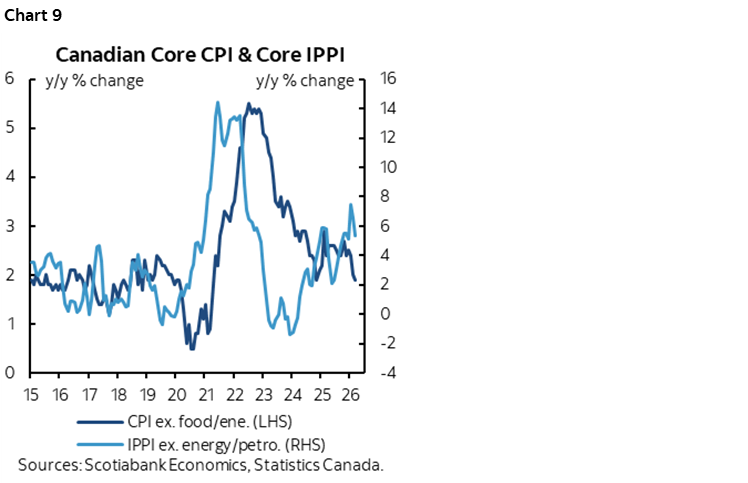

Key was also Macklem’s press conference which backed up the assertion there is little evidence that the oil spike has pushed into core inflation and a bias toward seeing little risk of this occurring. There are multiple caveats to saying this and I’ll come back to some others in a moment, but for now, it’s worth noting that of course there isn’t such evidence of core transmission at time t=0 since the oil shock is very recent. That’s almost absurd to think it might otherwise have been the case. Nevertheless, Canada may already be reemerging from a temporary core inflation soft patch (here) in the wake of the latest data and with more to possibly follow (chart 9).

See the transcript of the (short) press conference later in this note. It felt like the press conference was deliberately kept short.

WHERE I HAD ISSUES WITH THE COMMUNICATIONS WAS IN THE FOLLOWING RESPECTS:

Yet the forecasts and guidance left one wanting more in several areas where the assertions are controversial or incompletely addressed.

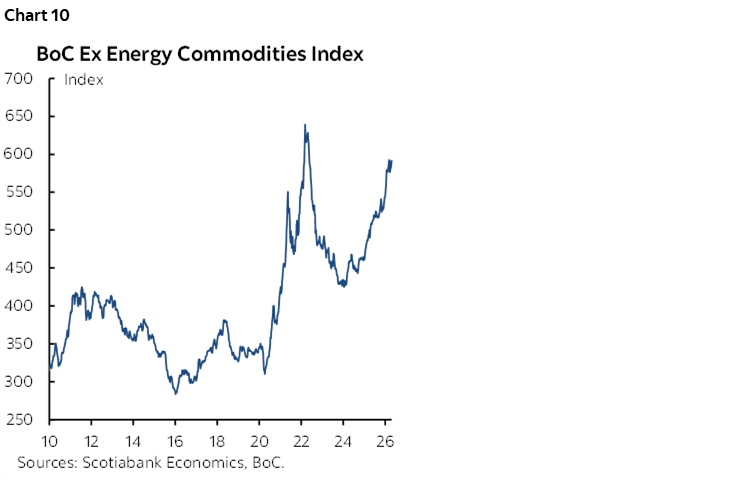

1. The BoC never once mentioned commodities ex-energy. Whoopsidaisy. All they spoke about was oil. And nobody asked them why in the presser. The BoC’s own commodity price index ex-oil is on fire (chart 10). Practically every commodity this country produces is lit up. Yet they only spoke about oil and gas. As a consequence, the BoC is heavily underweighting inflation risk from a headline perspective and probably from an underlying core pass through perspective.

2. They never mentioned the Spring Economic Statement that was delivered last evening and not a single journalist asked them why in the presser. Extra whoops. The federal government added C$38B of extra spending with much of it front-loaded and equal to ½% of NGDP this year and ¼%+ next year. And nobody asked about fiscal easing and what it could mean to the BoC. Macklem might have passed on it, saying they’ll need to take a closer look and haven’t had the time since last evening to do so in order to avoid bombing the FinMin’s efforts, but he should have been asked. And it’s material to how the BoC could behave.

3. Judging by the BoC’s growth forecasts that were unchanged ex-inventories it seems Ottawa doesn’t think Canada produces any of the commodities that are on fire. Nah, how could that possibly benefit growth, they say. It’s only a headwind, they say. In the past, the BoC more clearly enunciated the terms of trade effects on GDP growth that can be positive in a commodity-producing country when commodities are rising, negative when falling. Macklem’s predecessor did it all the time. The way Governor Macklem spoke today would almost have you believing this is Europe that is a heavy importer of many commodities.

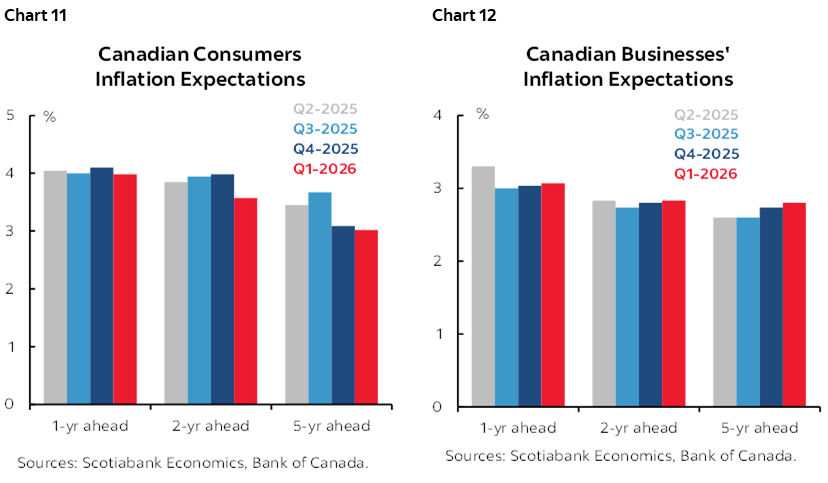

4. We were told in the presser that inflation expectations remain close to target but that they would be concerned if that wasn’t the case over the medium-term. Yet the BoC’s own consumer and business surveys showed inflation expectations at or above the top end of the 1–3% inflation target range throughout all horizons (charts 11–12). And those surveys were conducted in February, before the war. The next surveys available in July based on May answers will light up. Will you fade those too by saying more about consumers not understanding inflation (which they don’t) in which case why do you place emphasis upon them now? When saying medium-term inflation expectations are controlled around the target, what measures are you referring us to since that’s not even in your stale surveys and RRB breakevens are useless in Canada? I can get that consumer and business expectations have plenty of caveats. So do BoC forecasts. So do consensus street forecasts which is onto the next point.

5. The BoC has the lowest inflation forecast on the street compared to major forecasting shops. At 2.2% y/y in 2026Q4 they are below the median 2.5% forecast with some—like us and a few others—in the high 2% and low 3% range. Yet the BoC is using the same WTI futures curve as input to their views as we are. I’m having a hard time understanding how they’d be a full percentage point below us using very similar oil price inputs. Maybe it’s because they’re apparently ignoring all other commodities that are on fire. Maybe it’s because they seem to believe in unusual views that a commodity price boom wouldn’t be of any use to a commodity-producing country.

6. When discussing their two scenarios—a trade shock and oil shock—and when they were asked about combinations in the presser, the combination that wasn’t addressed may be the most realistic. What if a revised CUSMA/USMCA trade deal is achieved and the commodity price shock remains elevated with trickle through? I think that’s the most likely combination and have written about my views on trade elsewhere.

7. There was only emphasis placed upon the policy rate measure that doesn’t matter. The nominal one. 2.25%. The BoC did not opine on the real rate and again nobody asked. No modeler would say it’s the nominal rate that’s key versus the real rate that is arguably plunging in an expectations sense. Easing, in a country that produces all of this stuff. With fiscal policy stimulus being added. Why is the BoC passively easing in a positive commodity shock in a commodity-producing economy?

8. There was little emphasis upon current GDP tracking. The prior statement emphasized downside risks to growth that didn’t make the cut this time. And yet at 1.5% for Q1 GDP growth the BoC is tracking below our current efforts around tracking that point to 2%+. We’ll get GDP for Feb and March tomorrow that will further inform tracking even though it’s on a monthly production basis, not the expenditure-based readings the BoC and consensus forecasts on a quarterly basis.

PRESS CONFERENCE TRANSCRIPT

Here is my usual attempt at a press conference transcript with any errors or omissions to be blamed on my speed typing into chat rooms during the live event with commentary.

Q1. What is your message to households and businesses who might start demanding higher wages and if inflation expectations go up?

A1. Speaking generally about what the BoC can control. Preventing surge in gasoline prices and other fuel prices doesn't become generalized inflation. Maintaining the policy rate was the right thing to do today. If things evolve broadly in line with our forecasts and oil prices come down then something close to the policy rate is about right but there might be a need for a small adjustment. If energy prices go higher and stay higher for longer then there could be a need to raise the policy rate by more.

Q2. Is AI and the productivity impact yet factoring into the policy setting and how do you think about it?

A2. There are a few things affecting potential output. We do a review once a year and that is each April so we have an appendix on that in the report. Three things affect potential in the outlook. Population growth is historically low so we're not adding new workers and consumers and that lowers potential output going forward. Secondly the Canadian economy is going through a structural adjustment and our trade relationship with the US has fundamentally changed and through that adjustment this will weigh on productivity growth. Those two things are weighing on potential GDP growth particularly in the near term. The third factor is AI which is a transformative technology. As more businesses use it we do expect to see a modest pick-up in labour productivity growth going forward and it adds about 0.2 to productivity growth in the projections. Those three things taken together mean potential is wek in the nearer term but eventually picks up somewhat.

Q3. You spell out two risks: higher oil prices than assumed, trade risks. Those aren't mutually exclusive. How do you balance the risks if both happen?

A3. We outlined two scenarios particularly important. Monetary policy may need to be nimble. We provided a couple of examples. If oil goes up we would probably need more than one and probably consecutive increases. We also highlighted trade risks if tariffs go up and cut risk. An abrupt correction in financial markets could be another shock. We're trying to convey the rough magnitude of certain scenarios but a combination would be even more complicated. [ed. I think he wasn't prepared to answer that Q...]

Q4. What is the timeframe that Canadians could expect you to be looking at oil prices and hike risk?

A4. The higher and longer oil prices go the more likely we would have to raise interest rates but there is no set timeline. It would depend on the conditions. It's all going to depend on what we think thereafter and what we see such as increases in other prices. What I would stress is it's about the shock itself and the propagation of that shock.

Q5. What does the BoC think is a more pressing threat? Oil or trade?

A5. [Rogers answering]. In the near-term it's the war in the Middle East. Over the longer term, the trade tensions are the bigger threat to the Canadian economy. We have the restructuring underway and negotiations. If there is a big change that could be another shock.

Q6. Does having the policy rate at the lower end of the neutral range make you more nervous and is that why you are talking about the potential of consecutive hikes?

A6. There is no risk-free path for the policy interest rates. If we had raised rates now and then oil prices come down then by the time those higher interest rates are impacting the economy they wouldn't be needed and we'd have wished we hadn't raised. If we wait too long and oil prices are higher for longer then we would wish that we had raised earlier. Right now we think the policy rate is appropriate.

We are starting with some slack and recently weaker core inflation. We don't think in that context that higher prices are going to be rapidly passed through the rest of the economy. We don't expect it will be rapid. You are already seeing it in some places like fuel surcharges but we don't expect it to be rapid. We know uncertainty is high and monetary policy may need to be nimble. We may need to change course. If oil prices stay higher for longer it would increase the risk of generalized inflation and we may well need consecutive increases in the policy rate to get inflation back to target.

Q7. CORRA is still above the target. You have given no indication you plan to fix this. Is that still the case?

A7. [Rogers answered] Our market operations are back to normal course. We wouldn't characterize this as a dislocation.

Q8. What motivated you to provide this form of forward guidance on when rates may increase or decrease?

A8. I wouldn't characterize this as forward guidance. It's really more about our reaction function. Governing Council is aware there is a wide range of outcomes that is possible. We discussed what would we do in some of these other outcomes.

Q9. What do you plan to do differently this time to avoid lessons from the pandemic on inflation?

A9. One of the key reasons from Covid was as we were coming out of it there was a combination of shocks. Supply shocks, Russia's invasion of Ukraine, the impact on inflation was large and rapid. When the economy is already overheated in excess demand, a supply shock that boosts commodities can spread quickly. Today's situation is different. The economy is in excess supply. Businesses are more cautious about passing on cost increases. That doesn't mean they won't pass it on and some will.

Q10. The latest BoC surveys show higher inflation expectations in the medium-term. If the next surveys showing inflation expectations rising again perhaps to 4% would you still say that is close to being anchored?

A10. [Rogers]. Inflation expectations are very affected by current inflation and frequently purchased items so we keep this in mind. You need to be careful to look for trends on inflation expectations.

[Macklem]. Given the pandemic experience, people may be more attentive to inflation and inflation expectations may not be as well anchored as they were before Covid. On the other hand we acted to bring inflation back down relatively quickly without causing a recession. What we saw in our own surveys of public trust toward the BOC it went down and has since gone back up suggesting confidence in keeping inflation controlled has not been eroded.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.