- BoC stays on hold at 2.25% as widely expected

- Our off-consensus hike call for later this year remains on track…

- ...with markets leaning toward two Q4 increases

- Slack and soft momentum in core inflation give the BoC time to assess….

- ...but removing ‘appropriate’ language may signal less patience than we thought….

- ...as the message was clear that a prolonged energy shock would risk tightening

- Waiting for clarity on inflation risk could let the cat out of the bag once more

- The BoC may be misinterpreting financial conditions

- The BoC may be partly understating the income benefits of higher energy prices

- The BoC needs to clarify its risky stance on courting lower house prices

The Bank of Canada stayed on hold at a policy rate of 2.25% as universally expected but the suite of communications had a mildly hawkish tone to it. The statement is here, Governor Macklem’s opening remarks to his press conference are here and I’ve included an attempt at a press conference transcript in what follows. Also see the attached statement comparison that emphasizes select changes compared to the now stale January statement.

Markets Lean Toward Two Hikes this Year...

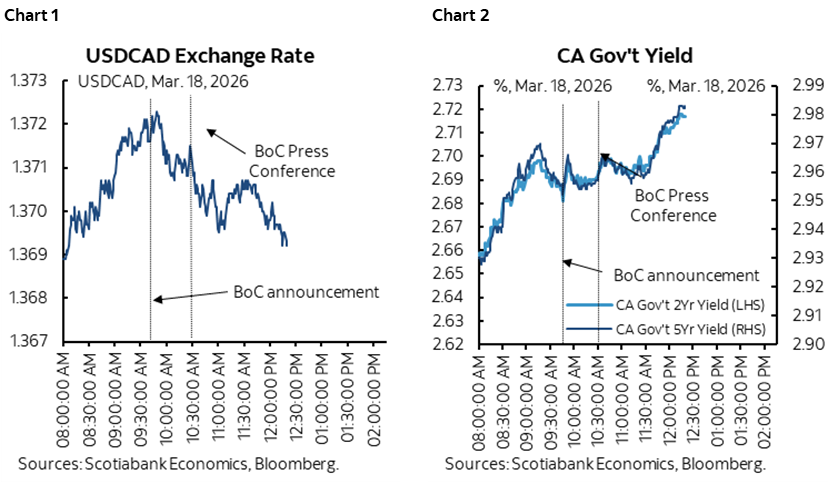

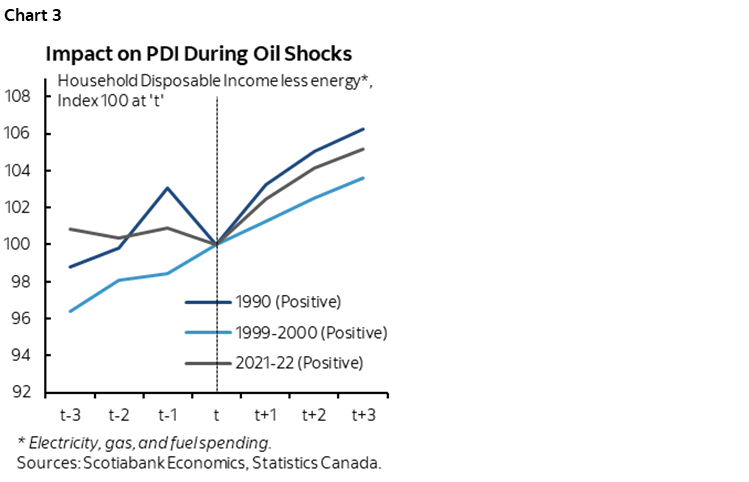

Markets reacted by at first consolidating a run up in short-term bond yields ahead of the communications and then adding to it as the 2-year GoC yield is holding about 6bps higher on the day so far. OIS markets are pricing an October 25bps hike with almost half of another hike in December. Our forecast remains two hikes this year in Q4. CAD is little changed ahead of the Fed. Charts 1–2.

One key is that when given the opportunity to shoot down a future hiking bias, Macklem declined (see Q#3 in the accompanying press conference transcript).

...Tentatively Supporting Our Forecast

It’s nevertheless obviously far too early to raise confidence that far out. There is an awful lot of ground to cover over coming meetings and a lot of uncertainty throughout the period that lies ahead.

For instance, we need to assess the duration and magnitude of the oil shock and how it trickles through, plus other developments in the local economy independent of the positive income shock Canada is getting and how fiscal policy evolves further with I think more compounded stimulus.

Trade negotiations will be important and more important is the outlook for the US economy. The latter matters more because with just under 90% of Canadian exports to the US being CUSMA compliant and a depreciated CAD from past years, trade competitiveness for most exporters has improved and has been benefiting from an income pull-effect from the US economy. If the US economy goes down amid mounting risks, then we've got bigger problems than trade negotiations. In that scenario, Canada would depend upon a commodity shock and fiscal to outperform the US as it grapples with tariffs, energy and uncertainty but disconnecting would be a rare occurrence

With that, let’s turn to how the BoC views this uncertainty.

BoC Statement and Opening Remarks

One immediate observation is that the statement struck out reference to "the current policy rate remains appropriate." They’re clearly more unsure of that being the case now which is probably correct. I found that striking out this reference was incompatible with what was otherwise a patient nearer-term message and that could signal openness to acting sooner than previously thought if conditions merit. Otherwise, why not just repeat that for now the policy rate is appropriate?

They did not explicitly reveal their hand on the likely direction of risks but hinted at it depending upon what happens going forward. Forecasters are left to weight the probabilities of the direction and timing of any future moves by making assumptions on the path forward that conservative, risk-avoiding and typically lagging central bankers would not make. I continue to believe this will be a long, drawn-out affair with a permanent oil and gas price shock at levels well above early January prices for an extended period of time. At the same time, I’m still cautiously optimistic toward CUSMA/USMCA negotiations while fiscal policy additions remain in motion at the hands of a federal government that is only just beginning to roll out initiatives particularly in defence- and infrastructure-related spending.

On which direction the BoC may tilt, I'd flag references to "inflation risks have gone up due to higher energy prices" and "it's too early to assess the impact of the conflict in the Middle East on growth in Canada" and "Governing Council will look through the war's immediate impact on inflation but if energy prices stay high, we will not let their effects broaden and become persistent inflation." That’s a combination of what was said in the statement and opening remarks.

As for the nearer-term inflation risk, I figure that next month's (March) inflation reading will get about a 0.5 ppt lift to the y/y rate from gasoline prices based on tracking so far to mid-month. All else equal, that would drive the y/y headline CPI rate up toward 2.3%. It will go even higher in April when last April's elimination of the consumer portion of the carbon tax shakes out and that base effect will persist for many months. Canada will soon be getting headline CPI inflation in the 2.5–3% y/y range, above 2% target, with uncertainties around duration and pass through. And then the real debate on sustainability of the energy shock and pass through begins.

Against this was the comment that “With inflation close to target and the economy in excess supply, the risk that higher energy prices quickly spread to the prices of other goods and services looks contained.”

So, you mean to say you’d wait until you definitely think higher inflation is here to stay and will be passed through core before you have confidence to act? My gosh we’ve learned nothing on monetary policy. I’d prefer a more gradual approach that responds if information gradually leans in the direction of such risks rather than waiting until it’s standing right in front of you. That’s how we got out of control inflation the last time around with a lagging central bank.

Governor Macklem also referenced tighter financial conditions through higher bond yields, lower equities and tighter credit spreads but committed the same sin central bankers often make. The reason bond yields have moved up and equities have softened—both modestly so—is because they expect central bankers to react hawkishly. You can’t then turn around and intimate that your job is then done by markets since if you don’t follow through, conditions may ease again. Chicken meet thine egg.

The BoC then went on to note that “the longer this conflict lasts and the wider it gets, the bigger the risks.”

That makes it reasonably clear that a prolonged conflict and turmoil in energy markets would drive the central bank of a net energy exporter toward removing some policy accommodation in the event that headline inflation trickles into core inflation which would be directly tied to the longevity and magnitude of the shock. Of course, if markets were to meltdown and truly nasty developments arise then we’d revisit.

Nevertheless, this is clearly not a central bank in a rush but the message is extremely clear—the oil shock is too early to assess now and so far raises little pass through risk to core inflation because of modest slack and prior softening of inflation, but if it persists or worsens, they're going to have to respond and that probably would mean hiking.

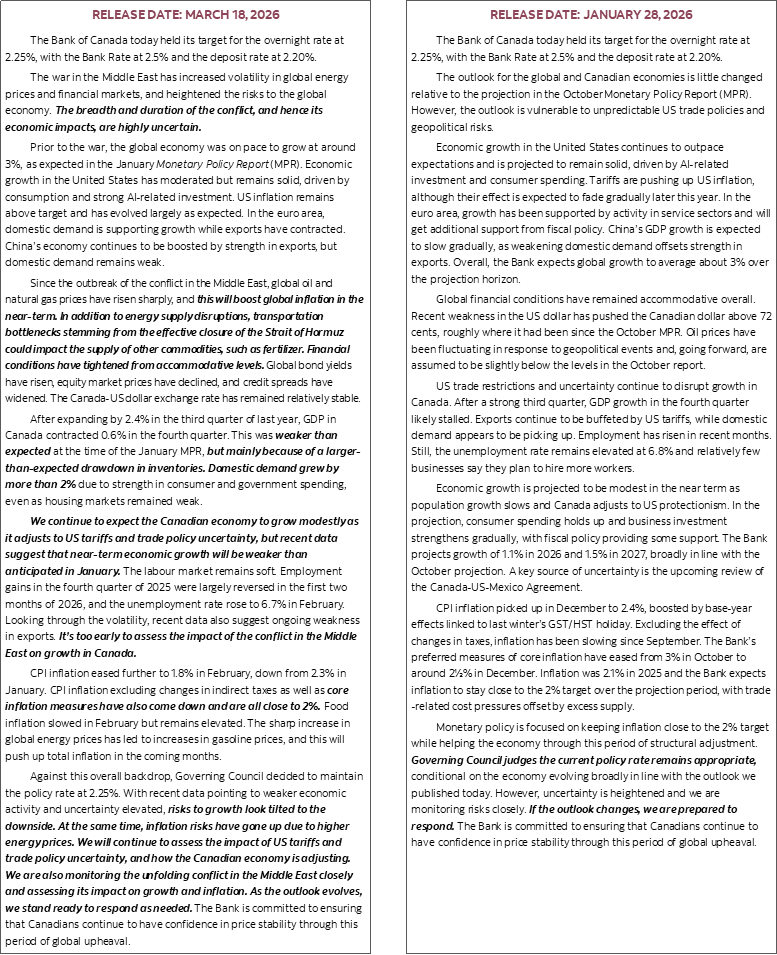

Macklem explained the terms of trade shock from higher oil prices rather clearly in that it raises incomes and adds to potential inflation risk, but I’m not sure of his remarks on one part of it. Higher energy prices do raise overall national incomes and benefit fiscal and corporate balances in aggregate, but his comments on what they could do to household income seem debatable. Macklem’s point is that higher energy prices squeeze inflation-adjusted take home pay. That depends on a lot of other assumptions, like how wages respond and how substitution effects evolve such as driving less, using less A/C or heating, or flying less and how shareholder distributions are impacted on top of trading off divergent regional effects on incomes. Chart 3 shows what happened to disposable (after-taxes and transfers) income minus spending on electricity, gasoline and fuel in past positive oil shocks. Incomes net of energy spending did not suffer in any of the recent experiences so perhaps the BoC is understating the benefits of higher oil.

Macklem also emphasized the importance of inflation expectations and particularly whether long-term expectations remain well anchored. Unfortunately we won’t get much insight on that for months to come. Canada’s measures of inflation expectations are poor. The next BoC surveys of consumers and businesses may show only a little pick-up in inflation expectations because, for instance, the consumer one's sample period is likely to be from the end of January to around February 20th and hence before the war. It won’t be until the July editions when the surveys more adequately capture inflation expectations. In the meantime, business expectations on a monthly basis from the CFIB may be more useful but here too they don’t provide enough information over an extended time period.

The statement largely dismissed Q4 GDP growth of –0.6% q/q SAAR relative to the January MPR forecast of 0% due to the inventory draw down while referencing solid growth in final domestic demand as expected. They note that Q1 growth is tracking below their January forecast and using monthly production side GDP I’m tentatively tracking +¼% q/q SAAR GDP growth versus the BoC’s January forecast of 1.8% using quarterly expenditure-based GDP. Some of that gap may be closed by a rebound from the Q4 inventory drag.

The statement hinted at a continued bias into the next April MPR forecasts for “the Canadian economy to grow modestly” going forward.

They remain cautious on the job market. In January, they referenced the unemployment rate remains elevated and hiring intentions are soft. Now they say "the labour market remains soft" and flag the Q1 slowdown from Q4 job growth. I was disappointed that no journalist probed further on the job market; jobs may have weakened very recently because the supply of workers is ebbing as population is contracting.

The BoC Should Be More Careful on Housing

I'm sorry, what did I hear?? During the presser, SDG Rogers said “We need house prices to come down so that homes are more affordable.”

You mean to say that the BoC has an explicit bias toward getting house prices lower? That’s dangerous ground. Does that mean the BoC would set a high bar against easing if needed going forward because they wouldn’t want house prices to rise? Courting lower house prices is a very dangerous thing to say. It conjures up the ‘catch a falling knife’ problem whereby if people expect house prices to fall, then they’ll hold off on purchases and prices will keep falling and perhaps more rapidly so. That makes monetary policy less effective in an inelastic demand for money sense. Ask China. Getting house prices lower with a negative wealth effect would make things worse.

Policymakers should be laser-focused upon getting incomes higher by improving growth compared to ten wasted years.

And when the BoC says things like this, they feed generational divides. They pit those invested in housing versus those looking to get in. The latter should also understand they wouldn't benefit in terms of overall economic conditions from free falling house prices. Again, ask China.

PRESS CONFERENCE RECAP

What follows is my attempt at providing a full transcript of the Q&A portion of the press conference after Governor Macklem finished reading his published opening remarks. Typos/errors/omissions are my own doing absent a full transcript.

Q1. Is an oil shock net positive or net negative for the Canadian economy?

A1. It depends very importantly on the duration. If oil prices stay high for an extended period, the income coming into the country from exports of oil will be higher and that will support the economy. For consumers and most other businesses, higher oil prices are going to squeeze them. There are other effects like some tightening in financial conditions like stocks down, bond yields up, credit spreads tighter. The longer this conflict goes on there are other potential implications such as for fertilizers that go through the Strait of Hormuz. The short answer is it's too early to assess the effect on growth as it depends on duration and how this conflict materializes. What we can say is that if it lasts, whether it is net positive or net negative there will be shifts in the composition of growth with the energy sector doing better but consumers getting squeezed.

Q2. How is the BoC thinking about food inflation now? Are impacts there transitory or more persistent?

A2. SDG Rogers. Depends on duration. Canada imports a lot of food. It's a bit early to tell. Energy is a big input cost to food.

Q3. Do you view policy moves as equally balanced or do you lean to a potential increase?

A3. Uncertainty is high. We're prepared to respond as needed. We're watching the war in Iran. The risk right now of energy transmitting into core is low so it made sense to hold today. We know inflation is going to go up in March CPI. The issue for us is not the immediate increase in inflation. We know that's going to happen. It's whether it persists and gets more generalized. We're also monitoring trade negotiations, structural changes in the economy, tariffs etc. We have to look at the whole picture and take it one week at a time.

[ed. key is he didn't shoot it down....]

Q4. What is the biggest risk to the Canadian economy right now?

A4. We have to look at the whole situation. Growth and inflation are related and there are additional cost shocks coming from energy. It's not a matter of saying one thing is bigger than another.

Q5. What are the wider implications of the war on the Canadian economy and how concerned should consumers be about inflation over the coming months?

A5. The biggest cost is the human tragedy but it's also an economic shock. The fact the Strait of Hormuz is essentially closed is cutting off a lot of energy and pushing prices higher. The impact will depend on how long it lasts. The longer the conflict goes on, inventories get depleted and the economic consequences rise. You expect to see more impact in financial markets so the longer it goes the bigger the effects. Higher prices means more income coming into the country through things like energy and fertilizers but incomes get squeezed. The issue for us is not about the near-term. What we will do is ensure that if energy prices stay high they do not become ongoing generalized persistent inflation. [ed. english translation is hike]

Q6. Think it was a Q on new developments and what to monitor.

We will be watching total CPI as our target and whether it is persistent. Core measures are helpful and strip out volatile components like energy and inform whether it's spreading. We can look at the whole distribution/breadth. The more components the more worry. And importantly we'll be looking at inflation expectations. We're also assessing the impact of tariffs, what's happening to employment, investment and hiring intentions, spillover effects from all of this and how it impacts the economy and inflation.

Q7. How long will you assess the war's effects? In weeks?

A7. We don't measure this in weeks. We're not looking at this as measured in weeks. CPI is released monthly. Our starting point is excess supply, decelerating core inflation measures, so we don't think we'll see rapid pass through into broader prices. We've got some time to make that assessment. You've got to look at the situation of the whole economy and multiple developments.

Q8. Would officials have talked about more accommodative policy were it not for the war in Iran?

A8. It would be great to talk about another economy! Looking forward, we would be looking at lower rates if the economy continued to deteriorate absent an energy shock but that's not what we face.

Q9. How worried are you that higher gas prices push inflation expectations higher? How would the BoC respond if growth remains weak and inflation moves higher?

A9. What we saw in the pandemic was that households' near-term inflation expectations moved up but longer-term did not and that allowed us to get inflation down relatively quickly. We do focus upon longer-term inflation expectations because if they become unhinged then it becomes much harder to get inflation down. That's what happened in the 1970s. We are prepared to look through the immediate effects but we will not let it spill over and become persistent. [ed. yes, but Canada's measures of inflation expectations are garbage]

Q10. How do you know when to move? And what is that move?

A10. There are important differences today versus coming out of the pandemic. Back then there was huge pent-up demand, accumulated savings, supply couldn't keep up, then Russia attacked Ukraine and global energy prices moved higher with inflation already above target and the economy already overheated. This energy price shock needs to be evaluated in terms of persistence, and is coming in the backdrop of inflation close to target for about a year with our core measures decelerating and there isn't a lot of pent-up inflationary pressure in the economy. We don't think this is going to spread quickly so we've got some time, but if energy prices stay high or move higher then that increases the risks and it becomes more persistent inflation. I can say what we will be following to make those judgements and we will update you each meeting.

A10 cont'd: Rogers this time. We learned a lot about supply shocks in the pandemic. If the Strait reopens quickly then that could be a quick bounce-back. As infrastructure is damaged that will take a long time to remedy. Some supply can come back quickly, other supply takes longer.

Q11. Manufacturing and housing in parts of the economy are weak. How is the BoC thinking about divergent regional conditions in setting a single policy rate?

A11. That's not something we can address with monetary policy. We have to look at the situation in the whole economy. We have one target and that is inflation for the whole economy. Over time, inflation across the whole country averaged over a year or two is pretty similar across regions. Our job is somewhat limited—to keep inflation low and stable for the country as a whole. [ed. to which you could add regional variations are the responsibility of governments and fiscal policy to address]

Q12, What high frequency indicators are you relying upon in real time?

A12. We can look at websites. Get data from businesses that are adjusting their prices more frequently than they used to. We put a premium on talking to businesses, our surveys, our outreach, invitations to come and speak to Governing Council etc.

Q13. House prices have fallen over a five year span. How much could a further decline weigh on inflation?

A13. Rogers speaking. The housing market is looking weaker than we had incorporated in our January outlook. The early data in March looks like a possible rebound but it's early. We need house prices to come down so that homes are more affordable.

Q14. Muddling question on country by country differences in an oil shock.

A14. There's nowhere else in the world I'd rather be than Canada. The impacts on growth and inflation depend upon whether you are a big energy exporter or big energy importer. Canada is a net energy exporter so we have more income coming into the country so our currency has been more stable than other countries versus other countries where their currencies are depreciating and adding to the inflation risk [ed. CAD is also firm because they are pricing hikes....].

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.