- Fed funds policy rate was left unchanged at 3.75% as widely expected

- Yields up, stocks down, dollar firmer as cut pricing was reduced & oil soared

- Iran crashed the FOMC, striking LNG plant in Qatar, driving oil and gas sharply higher

- Key is that the dots are more of a coin flip on a cut this year…

- ...as GDP and inflation forecasts were revised up

- The FOMC is in standby mode on the energy shock…

- …but may be overly discounting upside risks to inflation…

- …while also still discounting downside risks to jobs

The FOMC left its benchmark policy rate unchanged as universally expected but displayed less conviction toward the need for easing that sparked a mildly hawkish reaction in financial markets. Policy was described “as appropriate” for now. Chair Powell deferred judgement on the effects of the war with Iran, saying it was premature to judge. The press conference had a generally sloppy feel to it.

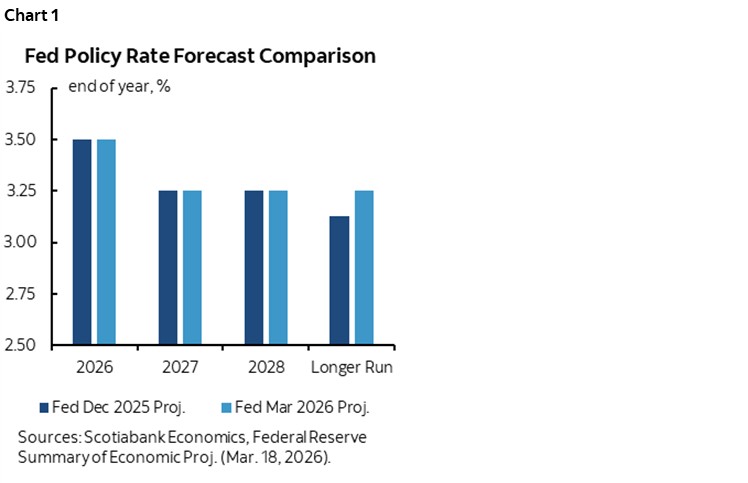

DOT PLOT REVISIONS SHOW LESS CONFIDENCE IN EASING

The Committee continues to guide that the fed funds target rate will fall by 25bps at some point this year and by another 25bps next year after which it is held in the 3.0–3.25% range. The fed funds median projections were unchanged (chart 1).

And yet key here was that the distribution of opinions is much less confident that there will be a cut this year. Chart 2 makes this point while chart 3 shows the full dots. It’s practically a tie among most participants as to whether there will be a cut or a hold. Also recall as always that the dots are not vote weighted. Given the rotation of the regional Presidents toward a generally more hawkish set, you can likely tilt the vote-weighted dots very slightly more toward a hold than if you were to take all of the dots into account.

MARKET REACTIONS

Markets responded by shaving pricing for rate cuts (chart 4), pushing up Treasury yields (chart 5), driving equities lower (chart 6) and the dollar firmer (chart 7). That said, oil surging on escalating Iran risks was probably more important than the Fed today.

FORECASTS

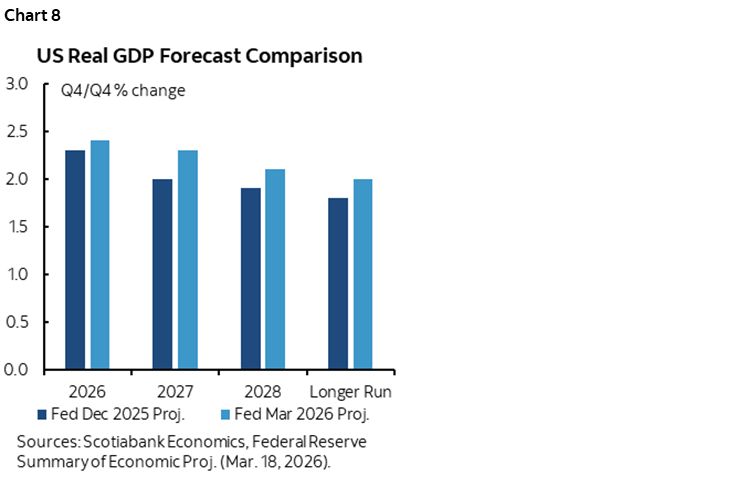

GDP forecasts were revised up across the board (chart 8). I'm surprised they revised 2026 GDP up a tenth to 2.4% this year as our house view will be materially weaker. It wasn’t clear that markets believed backing off rate cuts was ok because GDP was revised up somewhat.

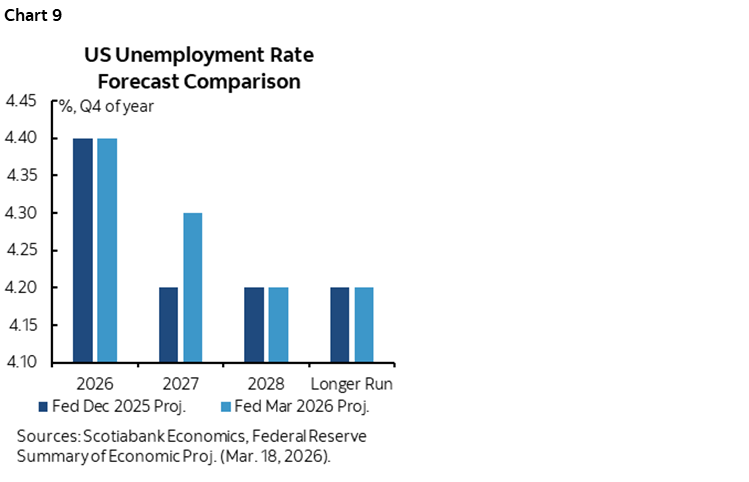

The unemployment rate projection was left unchanged this year at 4.4%, pushed up a tick next year to 4.3%, and then unchanged at 4.2% thereafter (chart 9).

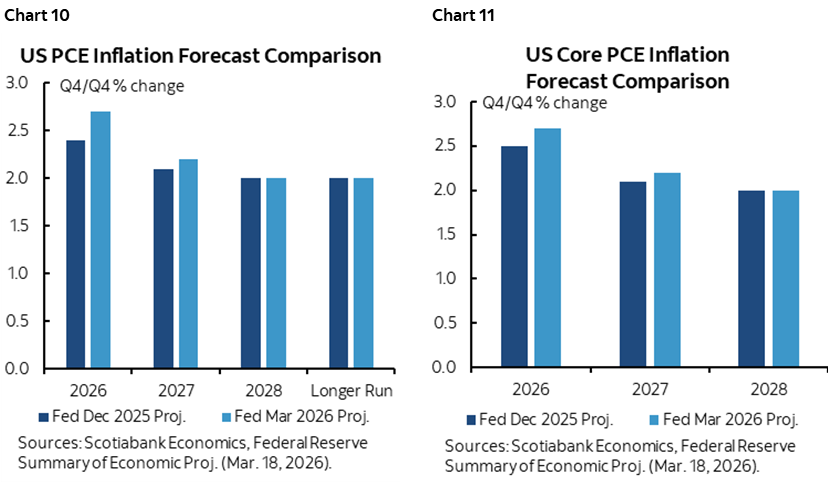

Core PCE inflation was raised two-tenths to 2.7% this year, increased a tick to 2.2% next year, and left unchanged at 2% in 2028 (charts 10, 11).

STATEMENT CHANGES

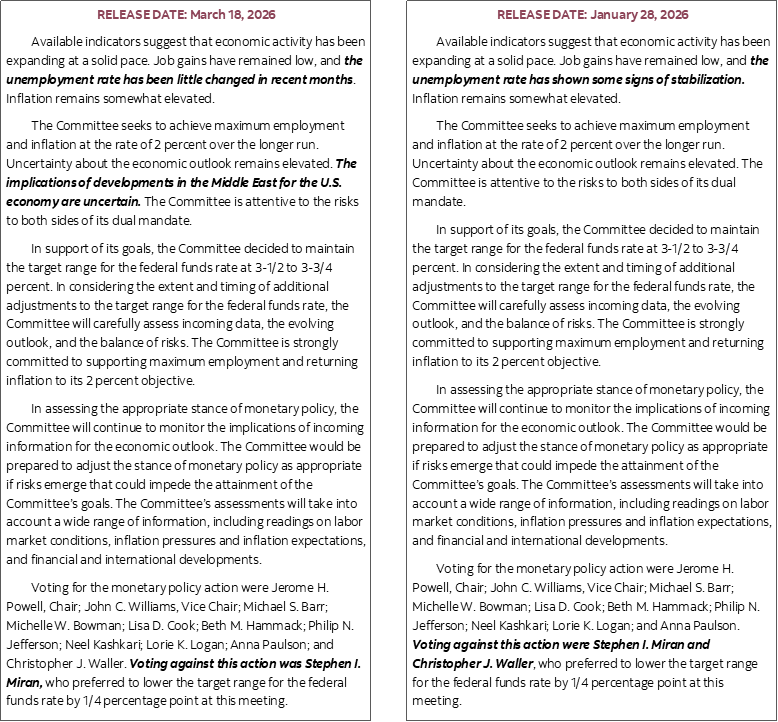

Please see the accompanying statement comparison.

They added reference to how “The implications of developments in the Middle East for the U.S. economy are uncertain.

They tweaked reference to the unemployment rate by now saying that “the unemployment rate has been little changed in recent months” versus previously stating “the unemployment rate has shown some signs of stabilization.” This is not material in my opinion.

Governor Miran was the lone dissenter this time as he preferred a 25bps cut. Despite expressing concerns about the labour market, neither Governor Waller nor Bowman dissented which was also a bit of a hawkish signal by the Committee.

ADDITIONAL KEY POINTS

- Powell candidly told everyone to ignore the SEP in the strongest language to date. He said “This was one of those times when if we were ever going to skip an SEP this would be a good one. But you gotta write something down.” That doesn’t give markets any confidence the FOMC knows what it’s doing. Markets need confidence during highly uncertain times whereas repeatedly saying I don’t know doesn’t help.

- There were a few hints at what to expect in the FOMC minutes three weeks from now. For one, they discussed the possibility of a rate increase but concluded the vast majority did not have that as their base case and so that’s why they did not introduce a more clearly symmetrical policy bias; watch for the range of opinions and reasons. For another, they discussed alternative scenarios at this meeting and that’s likely to be laid out in the minutes which may inform possible reaction functions around future developments.

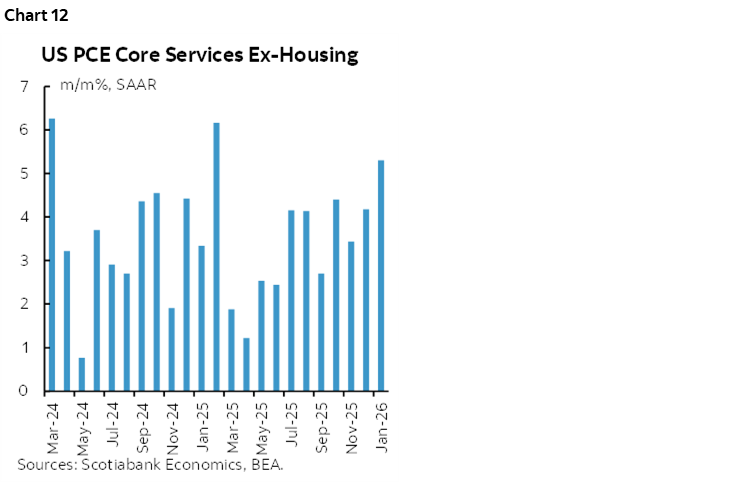

- Powell was called out for basically intimating that only goods inflation has been an ongoing problem to date. A reporter questioned him on core services inflation (chart 12) but the fact he had to have it pointed out was a touch disturbing.

- Chair Powell was also challenged on his view that tariffs would be a transitory driver of goods inflation adding 0.5–0.75 to core PCE inflation. When pressed, he said he didn’t want to sound at all certain this would be the case. In my opinion, the Fed is discounting the broader effects of restrictive US trade policy on supply chains and longer-run inflation. Take, for example, the reverse case here when China was welcomed into the WTO in 2001. That wasn’t one-time disinflation in a short time frame. It took 10–20 years to fully evolve. Supply chain disruptions start with a catalyst and take years to work through.

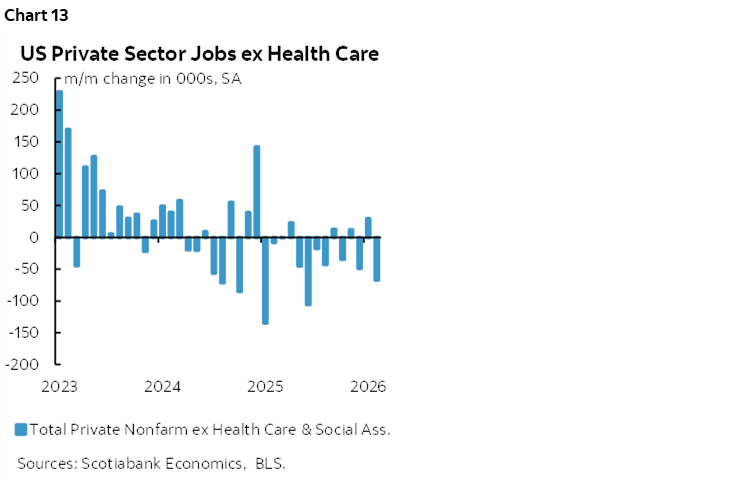

- Powell’s stance on the labour market seems a little too indifferent. He said to smooth through the January nonfarm gain and February nonfarm loss while not explaining the underlying drivers and the trend in private nonfarm payrolls ex-health (chart 13). It’s worrisome to me that a Fed Chair would significantly shake off longstanding labour market weakness. Just look at the chart! The break even for private nonfarm payrolls ex-health has not been negative for what amounts to years!

- For the first time, Chair Powell stated that if Kevin Warsh is not confirmed by the Senate before Powell’s term as Chair is up, then “I would serve as Chair until he is confirmed. I have no intention of leaving the Board until the investigation is well and truly over. On the question on whether I will continue to serve on the Board after the investigation is over I have not made that decision.”

PRESS CONFERENCE

What follows is an attempt at providing a transcript of the press conference with any errors/omissions being attributable to me particularly in some areas of the press conference where the questions were weaker.

Q1. Should the Fed look through higher oil prices stemming from the war and does persistent overshooting of inflation relative to target influence your thinking?

A1. The thing that's really important that we see this year is progress on a reduction of goods inflation as the one-time effect of tariffs move through. We need to be seeing that to know we are actually making progress. Total core inflation is about 3% and about 1/2 and 3/4 is due to tariffs. We don't address whether we look through energy shocks until we learn more. We need to see inflation expectations in the context of persistent above-target inflation.

Q2. Why is there still a bias to cut this year despite upward revision to growth and inflation? What's the need to cut?

A2. There are 19 people with different submissions. There was a meaningful amount of movement toward fewer cuts within the distribution. Each person has different stories. The forecast is we're making progress on inflation and it should come as we see progress on tariffs. If we don't see that progress then we won't cut.

Q3. Is higher inflation forecast solely due to the oil shock?

A3. Some is also in core. We haven't seen the progress we hoped for on core goods. In addition to Middle East risks.

Q4. Is the lack of change in the SEP more due to the expectation the oil portion will pass through or that consumption and growth suffer?

A4. Nobody knows. The economic effects could be much smaller or much bigger. People have no conviction. If we have a long period of much higher gas prices it will weigh on consumption but we don't know. We might have much lower pass through. This was one of those times when if we were ever going to skip an SEP this would be a good one. But you gotta write something down.

Q5. What are the offsets of higher energy prices in terms of consumption and production and employment and spending now?

A5. There isn't much of that happening now. Drillers are saying they want a persistent rise in oil prices for a fairly long time. The net effect of the oil shock will still be some downward pressure on spending and employment and some upward pressure on inflation.

Q6. How much would looking through the oil shock undermine your credibility around the 2% inflation target?

A6. You don't want to overreact. You have to base your decision on the best judgement and facts. It's a repeated set of things [driving inflation] and you worry that's the kind of thing that could influence inflation expectations. We're very strongly committed to keeping inflation expectations under control.

Q7. What gives you confidence that inflation returns to 2%?

A7. We're waiting for tariffs to work through and bring goods inflation lower. That's not coming from standard Phillips curve restrictive policy, it's coming from a one-off thing. We think it's important to keep policy mildly restrictive given labour risks to the downside versus inflation risks to the upside.

Q8. Why has non-housing services inflation slower to fall?

A8. We do expect it to come down. We should be seeing this. We're not seeing progress there.

Q9. Is the employment side a far greater risk than the inflation side?

A9. I wouldn't say that at all. We've been well above the 2% inflation target for some time and that's a concern.

Q10. What happens if no Chairman is not confirmed by the end of his term?

A10. I would serve as Chair until he is confirmed. I have no intention of leaving the Board until the investigation is well and truly over. On the question on whether I will continue to serve on the Board after the investigation is over I have not made that decision.

Q11. To what extent do you agree that the Fed should be focused on the growth risks as in earlier energy Gulf shocks?

A11. It's really hard to say. Depends a lot on what happens and inflation expectations.

Q12. It doesn't seem like your view on the labour market being driven by the supply side has changed. Is that correct?

A12. I think you have to take Jan and Feb together as positive and negative surprises. There are a number of indicators that suggest stability but the thing that concerns is the very very low level of job creation. Effectively there is zero net job creation in the private sector. Maybe the breakeven rate on nonfarm payrolls is zero.

Q13. The economy has experienced multiple supply shocks. Is that just bad luck or has something changed in the world to make the central bank to take account of a more common problem?

A13. I don't know that the world has changed but there are people who have made that case. We have seen more supply shocks in the last five years than many years before that.

Q14. What happened to revisiting the SEP as part of your framework review?

A14. Not much. There weren't many changes that had broad support on the Committee.

Q15. The minutes said two-sided guidance was supported by some members. Did that come up today?

A15. It did come up. The possibility of a rate increase was discussed but the vast majority did not see that in their base case.

Q16. How much concern do you have about whether this becomes an inflation problem beyond oil whether there is anything you can do about?

A16. It's completely out of our hands. We just have to wait and see. It will come down to how long the current situation lasts and the effect on prices and how do consumers react.

Q17. Was there a discussion around inflation expectations possibly being less sticky and the risks from higher oil and gas prices?

A17. Short-term expectations moved up quite a lot but long-term expectations have generally been pretty solid where they need to be consistent with 2%. We didn't have a lot of conversation about that but we'll be watching that extremely carefully as we see the effects of the price increases come through.

Q18. Some members were previously saying there could be a slow down in growth but that doesn't seem to be case in the SEP. Why. Was there any discussion of stagflation?

A18. The slight upward revision to GDP growth was driven by productivity expectation. We don't have the misery index readings we had in the 1970s. Calling today's unemployment rate and inflation rate combination is inappropriate. I reserve stagflation for the period of the 1970s.

Q19. Trump says inflation will go down very rapidly as soon as the war ends. Do you agree?

A19. I don't have a forecast for that.

Q20. Should consumers be bracing for higher costs?

A20. I don't want to characterize that in any way. We hope that's not for a long period of time. I don't want to speculate because that would sound like I have some idea of what's actually going to happen.

Q21. What might guide action at your next meeting? If oil remains high would it change your wait and see stance? Or are you on hold indefinitely?

A21. We'll have to wait and see. It's six weeks until the next meeting. It's going to be very important for how the outlook evolves, what happens in the Middle East. We did talk about alternative scenarios but I wouldn't bring that in here.

Q22. Is it a comment on how the US economy can be durable?

A22. Yes. The US economy has really been just doing pretty well through a lot of significant challenges.

Q23. Why would tariffs be a one-time effect?

A23. I would not use the word certain. I'm uncertain. It's a one-time increase in the price of a good. Inflation is ongoing increases in prices, it's not a one-time increase in prices. Tariffs should be one-time unless they expect more tariffs. I don't have tonnes of confidence on that. I think the theory is probably right but it takes time.

Q24. Are there any signs that persistent affordability problems are impacting the psychology of the consumer?

A24. It can take years for full effects to work through. Like insurance premiums. What it does for us is to make us even more committed to getting back to 2%.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.