- The Fed kept its policy rate on hold and balance sheet plans unchanged as expected

- Minor statement changes added reference to tightened financial conditions...

- ...which just repeated Powell’s remarks from two weeks ago

- Each meeting remains ‘live’ but not very convincingly

- The effects eased financial conditions at a curiously vulnerable point for inflation risk

The market theme of the week appears to be to react twice to the same information. That’s true in terms of the Treasury issuance statements on Monday afternoon and this morning’s repeated guidance that volumes will be lower than feared. It’s once again true in the reaction to the Fed as they statement-codified Chair Powell’s earlier warnings on tightened financial conditions. The result was to send a signal that they wish to rein in some of the bond selloff in terms of the overall mixture of policy measures.

The Federal Reserve kept its fed funds upper limit rate unchanged at 5.5% as universally expected and waffled on the bias in deference to the next meeting that is still described as ‘live’ but not in terribly convincing fashion. I think it was a misstep.

MARKET REACTION ADDED TO THE DAY’S EASING BIAS

The day's first big move lower in bond yields was after weaker US data (ADP, ISM-mfrg) and the Treasury refunding announcement that largely repeated Monday's guidance.

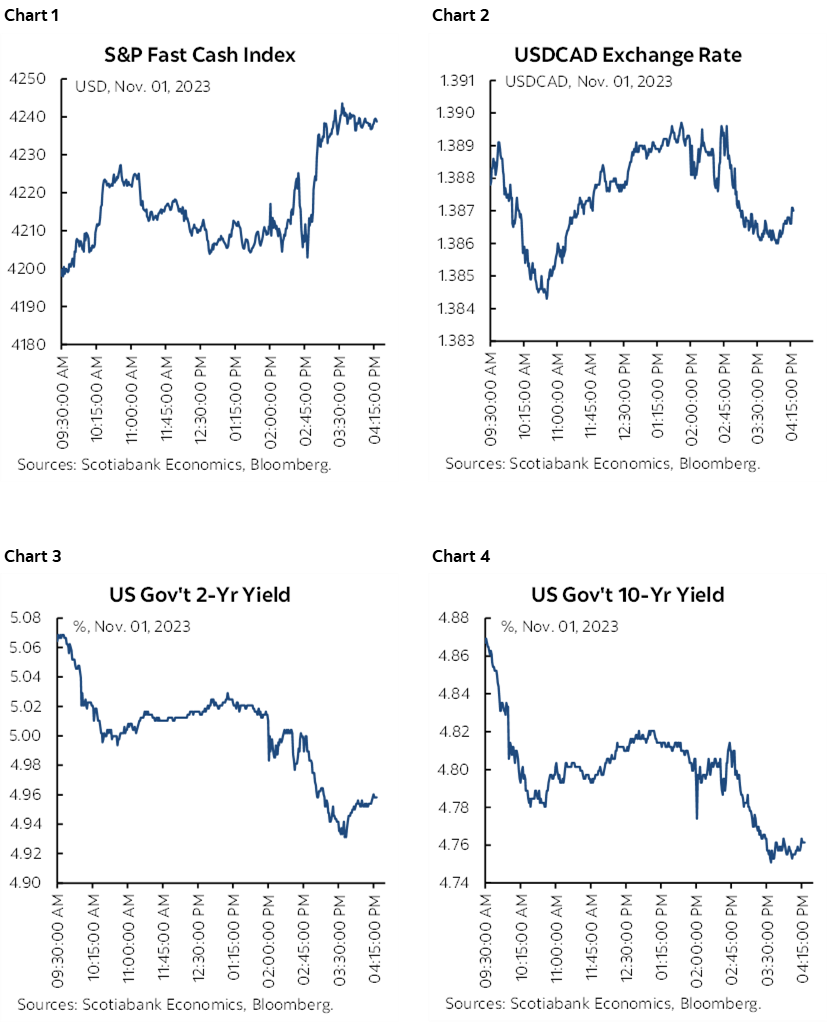

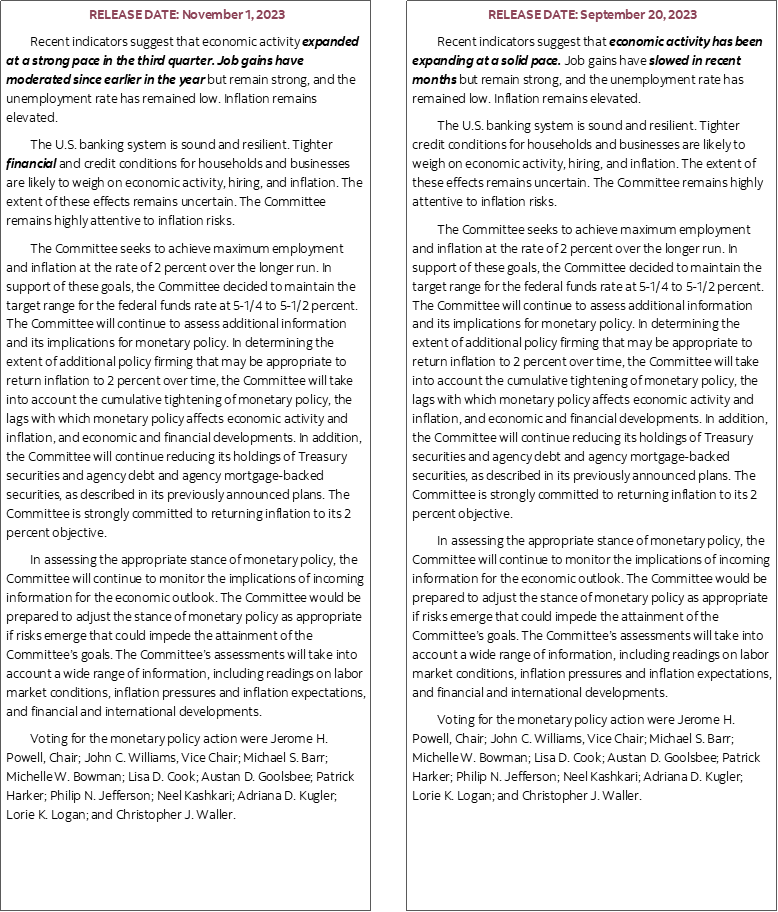

Powell added a bit more to this reaction (charts 1–4). The two-year yield fell a further 6bps throughout the Fed’s communications and is down 13bps on the day. The 10-year Treasury yield is down 17bps on the day mostly after this morning’s developments with the Fed’s communications adding about 4bps to the drop. The dollar modestly weakened throughout the Fed’s communications and is little changed throughout the day as a whole. Stocks liked it with the S&P 500 up by just over ½% post-Fed.

Markets are now pricing the first cut by June and almost a full percentage point of cuts over the next year which is double the guidance offered by the Fed in its last dot plot.

There is a lot of waffling and two-sided speak here which reflects a need to acquire a lot more information before arriving at any next phase whether higher or lower.

STATEMENT CHANGES BOILED DOWN TO ONE SINGLE WORD MATTERING

There were very few statement changes in a unanimous decision and only one of them seemed to matter to markets whether justified or not. The statement comparison is available at the back of this publication.

One word seemed to rock the boat and that was the statement-codification of the reference to how tighter financial conditions are likely to weigh on the economy. The statement did this by inserting “financial” alongside tighter credit conditions. That’s a clearer nod to how they view the impact of higher bond yields along with a strong dollar and equity market developments.

That’s basically what Powell had already told us in his comments before the Economic Club of New York on October 19th. Recall his full quote at the time when asked to comment on developments in bond markets up to that time and with bolded emphasis upon the most material part of that:

“It's hard to say what's exactly going on. It's not about expectations about higher inflation or shorter-term policy moves. The move is in longer-term bonds and term premiums and not principally looking at shorter-run matters. Markets are seeing the resilience of the economy to high interest rates and revising their views on longer-term rates. There may be heightened focus upon fiscal deficits. And QT. Also, if markets think we're going through rolling supply challenges. Then the question is does it matter to us? Actual and expected changes in our policy affect financial conditions. Persistent changes in financial conditions affect the economy. Are we seeing these higher longer-term bond show through financial conditions and yes, I think they are. Financial conditions indices are showing tightening and a lot because of longer-term rates. Then the question is whether it is endogenous, in other words if it's because they expect us to do more and that doesn't seem to be the case. We need to see evidence over time. It's clearly a tightening in financial conditions and we have to watch it carefully."

Other than that issue, the rest of the statement changes were fairly minor. The opening paragraph’s depiction of current conditions tweaked some of the language by upgrading recent growth to “strong” from “solid” and saying job gains have “moderated” instead of “slowed” which is a slight upgrade given how the Fed’s vernacular works.

PRESS CONFERENCE ADDED TO THE EASING OF FINANCIAL CONDITIONS

Powell’s press conference was basically about buying time to assess more data and developments while warning in somewhat unconvincing fashion that they stand prepared to tighten further if necessary.

He said that risks to inflation are “more two-sided now” and inflation expectations are expecting inflation to come down toward target.

Powell repeated references to “how far we have come” and that “the Committee is proceeding carefully” and that “We will make decisions on potential further tightening based upon the totality of the evidence.”

While saying labour demand still exceeds labour supply, he repeated that supply and demand in job markets continue to come into better balance with strong job creation accompanied by a rise in the participation rate alongside rebounding immigration to pre-pandemic levels. He nevertheless repeated that labour demand still exceeds the supply of available workers.

Powell also repeated caution that inflation still remains "well above" 2% and that “the process of getting inflation sustainably down to 2% has a long way to go.”

On the policy rate bias, he said “Evidence of growth persistently above potential or that labour markets are not coming into balance could warrant further tightening” and 'the Committee is proceeding carefully' and will make decisions on a meeting-by-meeting basis.

On higher bond yields, he said “We require persistent changes that are material and that remains uncertain. Secondly, higher longer term rates cannot be just a reflection of higher policy rates but it does not appear that this is the case. These higher Treasury yields are showing through to higher borrowing costs for households and businesses and impacting their decisions.”

When pushed on whether tighter financial conditions are acting as a substitute for rate hikes that are restrictive enough, Powell said “We are not confident yet. We are still evaluating whether policy is appropriately restrictive” and “We haven't made a decision about December“ while also keeping the door open to tightening even after December if they decide to pause at that time.

Finally, when asked whether the Committee's bias is neutral now, he said “I wouldn't say that at all. The language is about determining the extent of additional tightening. The question we're asking is should we hike more. In December we'll write down another forecast.”

In conclusion, it is my opinion that the Fed inappropriately eased financial conditions and egged on financial markets to more aggressively price rate cuts next year. Inflation risk remains pointed higher in my view in an economy that is performing very well. If easing financial conditions continue, then the Fed might have set itself up to behave more erratically next month.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.