- Job growth was disappointing, but marginally positive

- Despite soaring mobility and falling stringency, sickness might have held back jobs

- So might the Easter Bunny effect have done so

- Wages and hours worked tumbled

- The BoC is likely to remain fixated upon inflation

CDN jobs / UR, m/m 000s // %, SA, April:

Actual: 15.3 / 5.2

Scotia: 125 / 4.9

Consensus: 40 / 5.2

Prior: 72.5 / 5.3

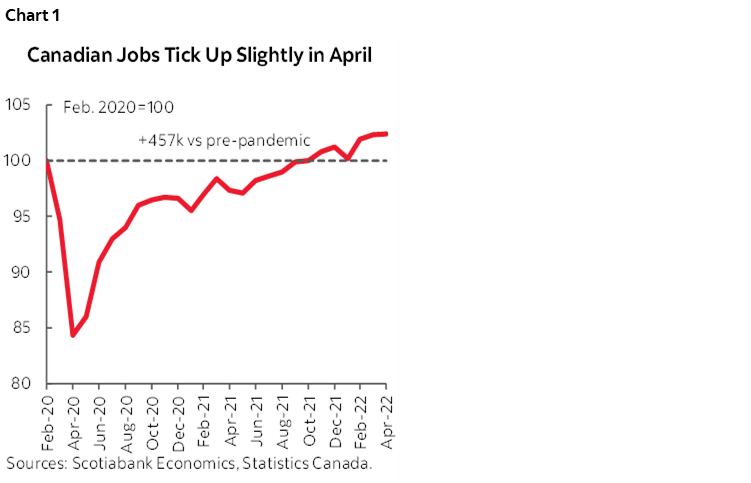

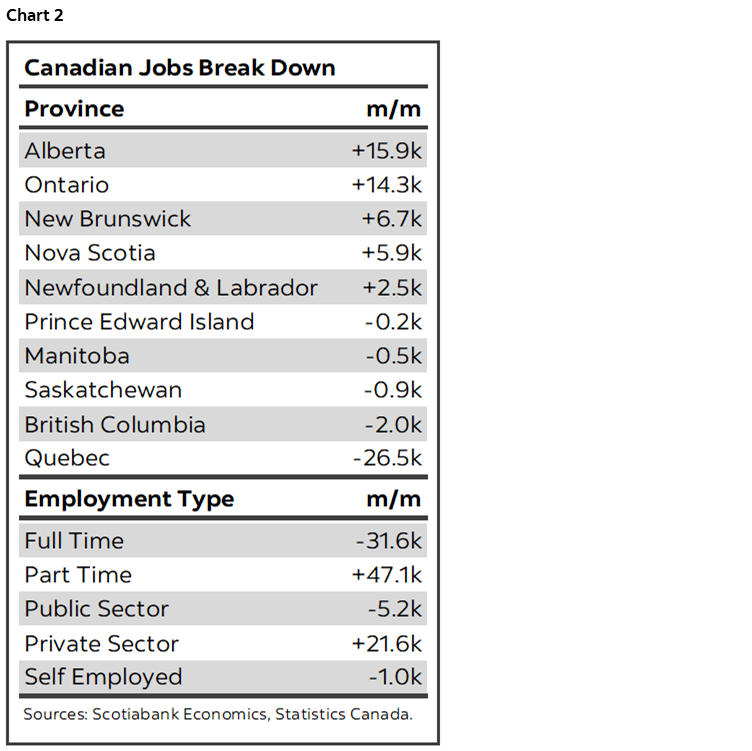

I think it’s possible but hard to prove that Canada’s job market may have been stronger than it appeared last month notwithstanding minor progress (charts 1, 2). Statistics Canada says that only 15,300 jobs were created in April and the underlying details were quite soft as reviewed below. We’ll need next month’s readings to offer a clearer picture of whether job growth is slowing in Canada than just one month alone.

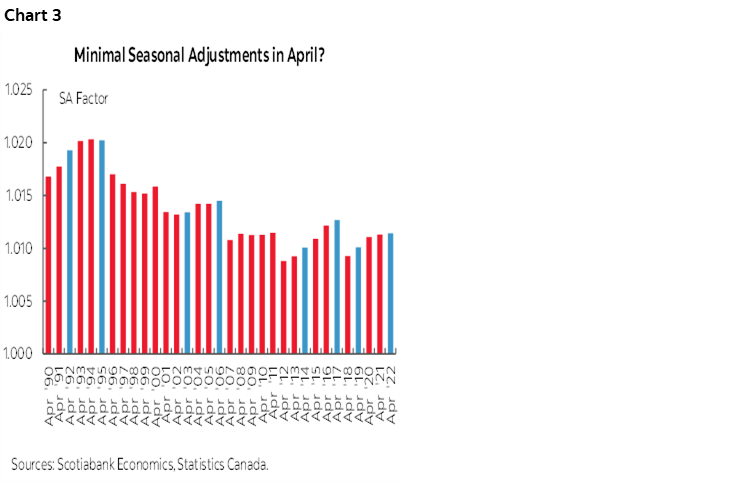

It’s possible that seasonal adjustment factors did not adequately compensate for the Good Friday holiday that landed in the Labour Force Survey reference week this time. The Good Friday/Easter holiday bounces around from year to year and commonly outside of the reference week for April.

Chart 3 shows seasonal adjustment factors for months of April over the years. This year’s did not change compared to last April’s or the April before that despite the fact those prior Aprils did not have Good Friday in their reference weeks.

Now on the one hand we know that the Labour Force Survey’s questionnaire (here) asks whether “last week” you were employed and how many hours were worked which would imply that during the survey reference week people are being asked—only by telephone—about their labour force status for the prior week. That would imply that Good Friday should not have impacted things this time and hence not merited a changed seasonal adjustment factor.

Then again, how people actually answer the survey could well be another matter. It’s also possible that reference week distortions are introduced by greater difficulty by Statcan’s callers to reach people on the holiday Friday into the Saturday. So we turn to data.

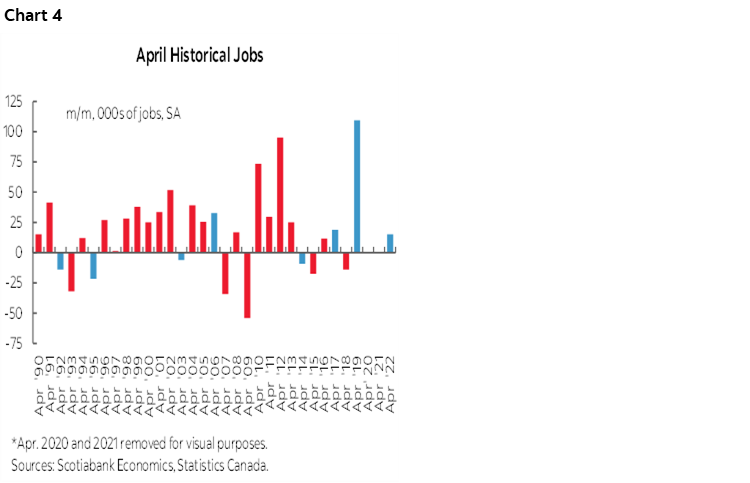

Chart 4 shows that Aprils when Good Friday lands in the April reference week that April tends to post weaker jobs reports than other months of April.

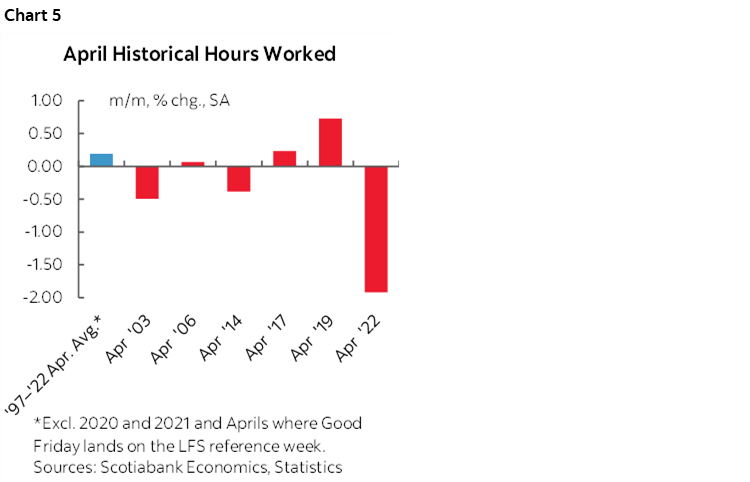

Chart 5 does the same thing for Statcan’s measure of seasonally adjusted hours worked. Aprils with Good Friday in the reference week tend to be weaker compared to other Aprils. We also know that average hours worked during the reference week are massively volatile over history during months when there is a long weekend that occurs around the reference week which is an unusual data anomaly.

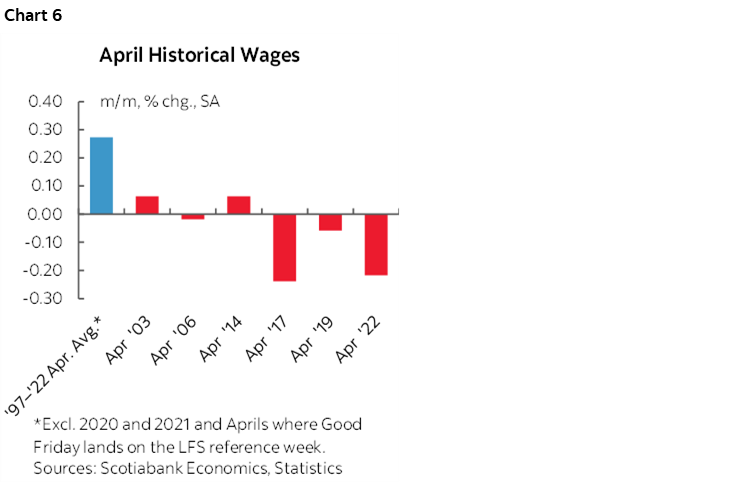

Chart 6 does the same thing for Statcan’s measure of seasonally adjusted wage growth in m/m seasonally adjusted and annualized terms. Again, Aprils with Good Friday in the reference week are noticeably weaker.

This could all be mixed and spurious, or it might not be. At a very minimum I would caution against reading too much into the figures, look to the trend and wait for further data on the status of the labour market. That’s especially so if sickness held back job growth and hiring behaviour despite plunging stringency measures and strong mobility readings that failed us this time in forecasting strong job growth. In short, a hacking, sneezing, headachy Easter bunny might have stomped all over this one.

SOFT DETAILS

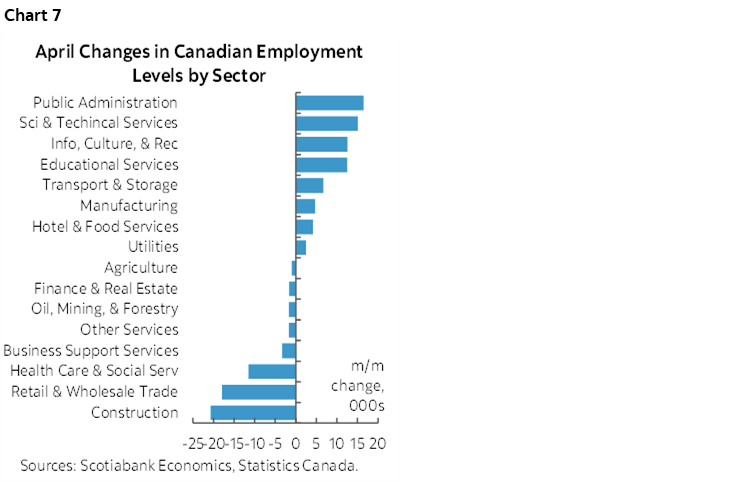

The breadth of employment gains was soft as shown in chart 7 that breaks down the change in employment by sector.

Full-time jobs fell by 31,600 and part-time jobs were up 47.1k which is a weak detail.

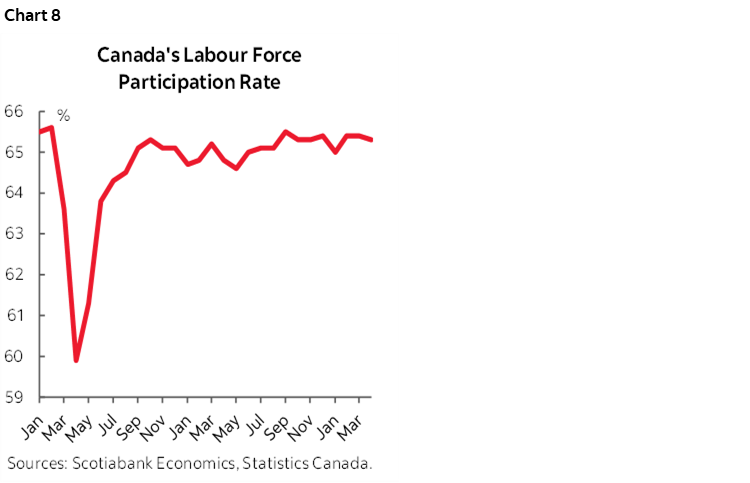

The participation rate ticked lower to 65.3% (65.4 prior) in chart 8 and so the fact that mild job growth occurred was enough to edge the unemployment rate down to 5.2% (5.3% prior).

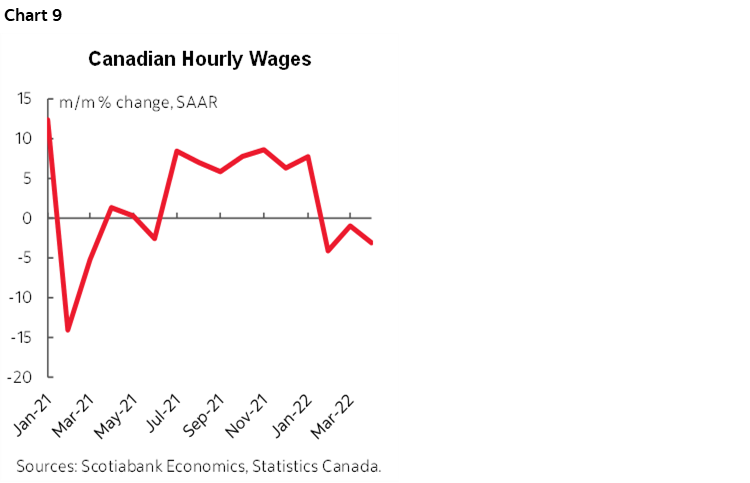

Wage growth was awful (chart 9). Seasonally adjusted wages fell 3.1% m/m at a seasonally adjusted and annualized rate (SAAR) in April. That follows a drop of 1% in March and 4.1% in February. Three months of weakness follows a string of seven strong monthly gains in the 6–9% range.

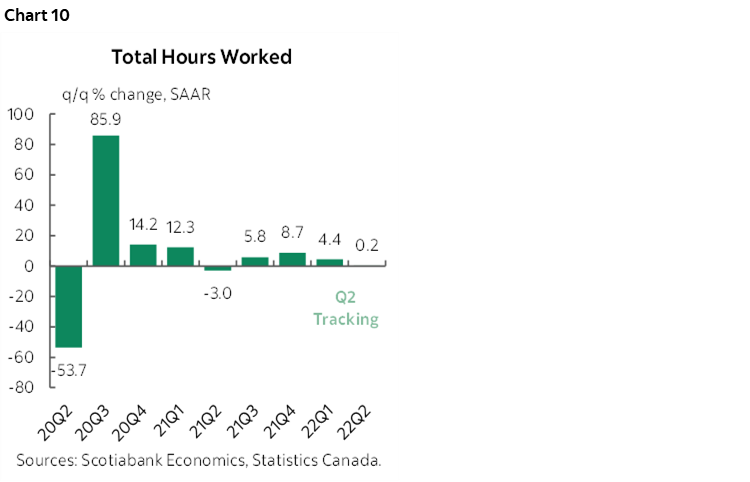

Hours worked fell by 20.7% m/m SAAR. After rising 4.4% q/q SAAR in Q1 they are tracking no growth so far in Q2 (+0.2% q/q SAAR) based solely upon April, the Q1 average and assuming May and June land flat in order to focus the effects upon what we know so far (chart 10).

BANK OF CANADA

In my opinion, the BoC won’t alter its course in any way on the basis of one soft jobs report, albeit a still positive one. The BoC’s nearly singular focus is now upon inflation. That’s probably why the two-year yield is essentially unchanged on the day as the rise into the report was subsequently reversed. The Canadian dollar depreciated to the US in part on USD strength given their jobs numbers.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.