- Canada’s economy isn’t perfect, but isn’t exactly begging for easing either

- Q1 GDP beat with mixed details…

- ...as the BoC won’t much care about the Q4 was downgrade...

- ...and soft momentum is continuing into Q2

- We are maintaining our longstanding hold call for next week’s BoC decision...

- ...but the reasons for a hold call go well beyond GDP

- GDP q/q % SAAR, Q1:

- Actual: 2.2

- Scotia: 1.7

- Consensus: 1.7

- Prior: 2.1 (revised from 2.6)

- GDP m/m % SA, March:

- Actual: 0.12

- Scotia: 0.2

- Consensus: 0.1

- Prior: -0.2

- April GDP ‘flash’ estimate: 0.1%

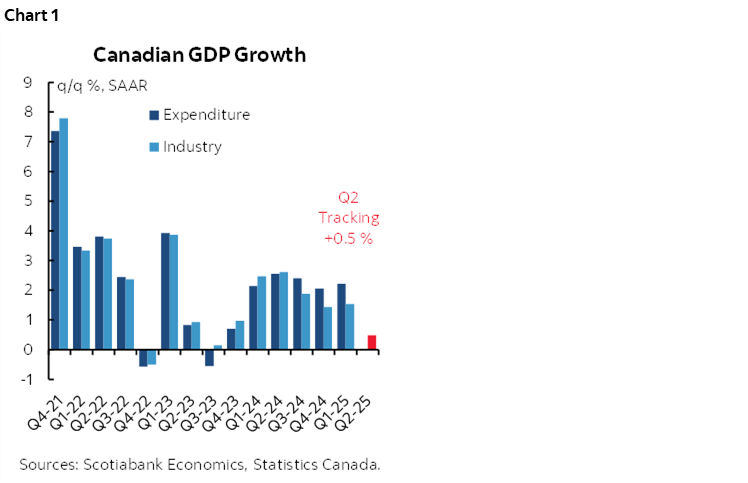

Canada’s economy is strong enough for the Bank of Canada to remain on hold next Wednesday alongside other reasons for doing so. Our longstanding call remains no rate change. Chart 1 shows growth using both quarterly expenditure- and monthly income-based GDP accounts with tracking into Q2.

THE NUMBERS

Q1 GDP growth of 2.2% q/q SAAR was a half percentage point higher than expected with the caveat that the prior quarter’s 2.1% growth was revised to be a half-point weaker than the previously understood pace of 2.6% that I’ll come back to.

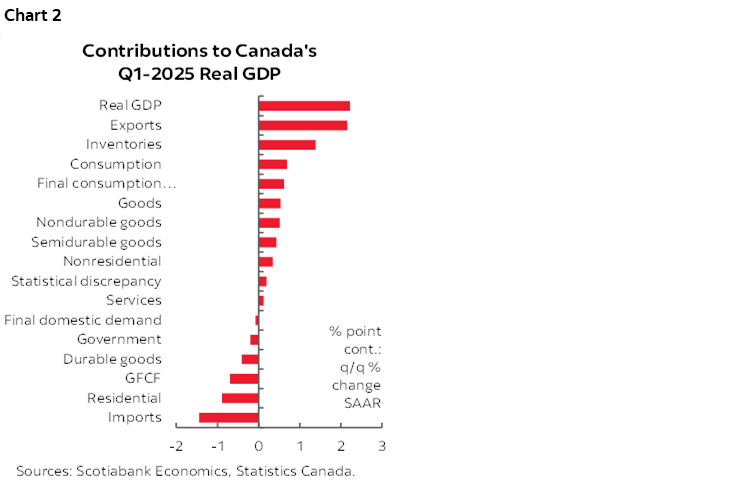

Chart 2 shows the weighted contributions to Q2 GDP growth by expenditure category. The details were not great, but not terrible either. Inventories added 1.4 ppts to Q1 GDP growth as companies stockpiled in the face of the threat of tariffs to supply chains. That doesn’t on its own give reason for fading the Q1 beat without also considering that imports were an offset by dragging 1.4 ppts from Q1 GDP growth as the inventory surge likely came heavily through higher imports. Exports added a strong 2.2 ppts to growth as exporters likely scrambled to get product to market before tariffs. What’s left is that consumption added 0.7 ppts to Q1 GDP growth mostly through semi-durable goods, residential investment dragged 0.9 ppts off growth, non-residential structures investment subtracted 0.4 ppts and investment in machinery and equipment added 0.7 ppts to growth. Government spending knocked 0.1 ppts off Q1 GDP.

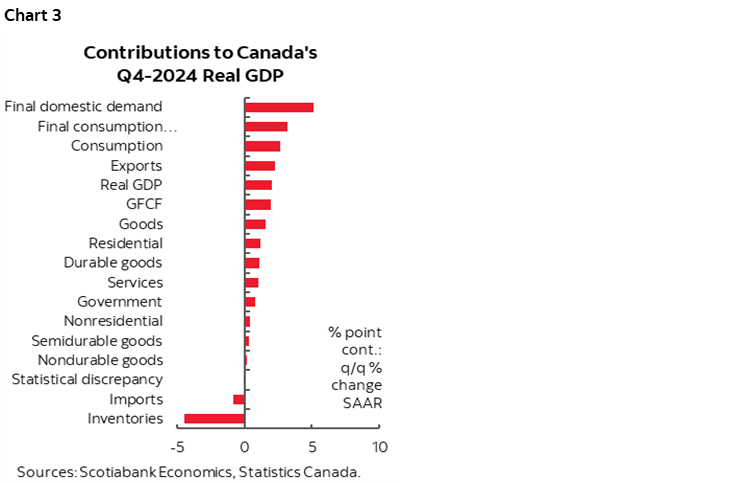

The BoC is unlikely to be fussed by the Q4 negative revision because it was almost entirely driven by a bigger inventory drag effect that knocked 4.5 ppts off of Q4 GDP growth versus 3.3% in earlier estimates. Imports are now less of a drag on Q4 GDP at –0.8 ppts instead of –1.8%. The rest of the Q4 GDP revisions were relatively little changed across other components (chart 3).

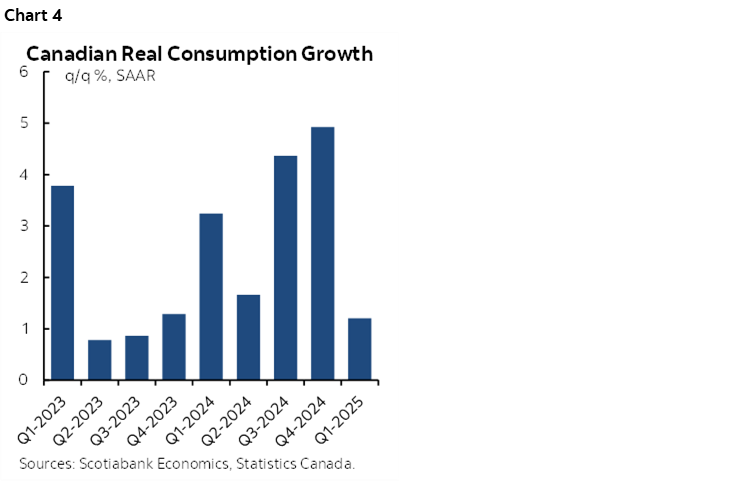

Consumption wasn’t great, but was still up by 1.2% q/q SAAR for a contribution of 0.65 ppts to Q1 GDP growth in weighted terms. Taking a bit of a breather after torrid rates of growth in each of Q3 and Q4 last year is understandable and frankly it’s a plus that after about 5% growth in Q4 that Q1 didn’t retreat (chart 4). Still, there are important forward-looking risks to further growth.

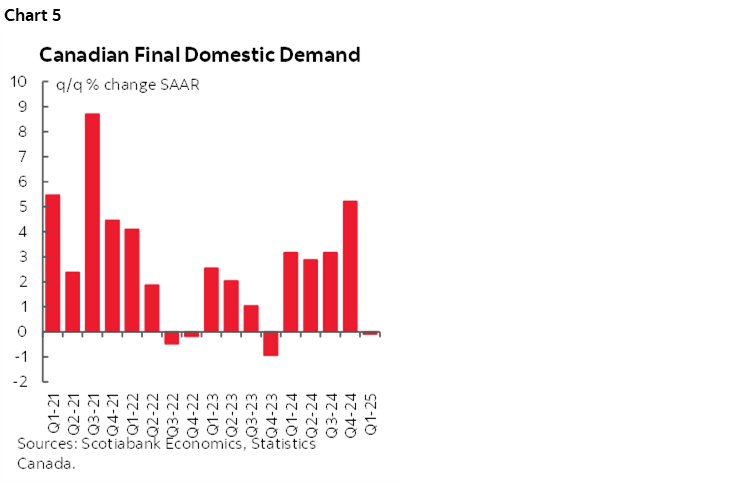

Chart 5 demonstrates a reason to be concerned about Q1. Final domestic demand adds up consumption, investment and government spending and hence doesn’t include inventories and net trade. It’s a rough measure of strength in the domestic economy and it was flat in Q1. That was mostly because of weakness in residential investment despite all the talk about expanding housing supply which remains just that—talk.

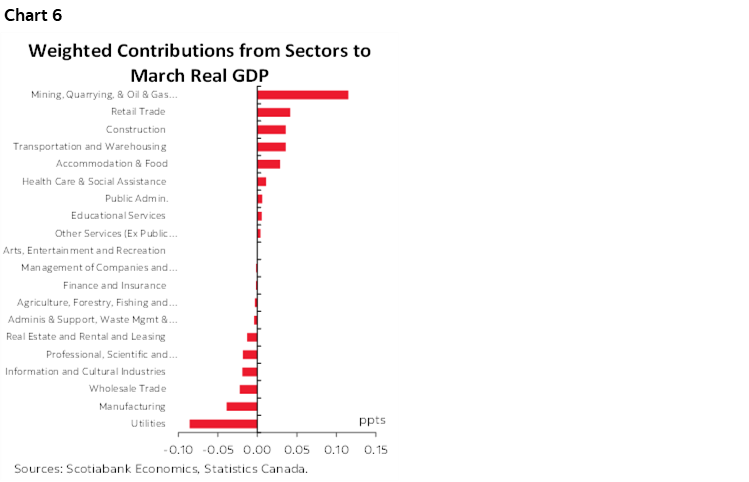

March GDP at +0.1% m/m matched Statcan’s earlier ‘flash’ estimate. Chart 6 shows the contributions by sector. In my opinion, the economy was sounder than the GDP headline for March because a tenth was knocked off growth by the utilities sector which is more of a volatile weather report than anything else.

April’s ‘flash’ GDP estimate landed at 0.1% m/m. That keeps momentum going into Q2 such that very tentative growth tracking points to 0.5% q/q SAAR in Q2 based solely on Q1 and the April reading while assuming the rest of the quarter is flat solely in order to focus upon the effects of what is known to date.

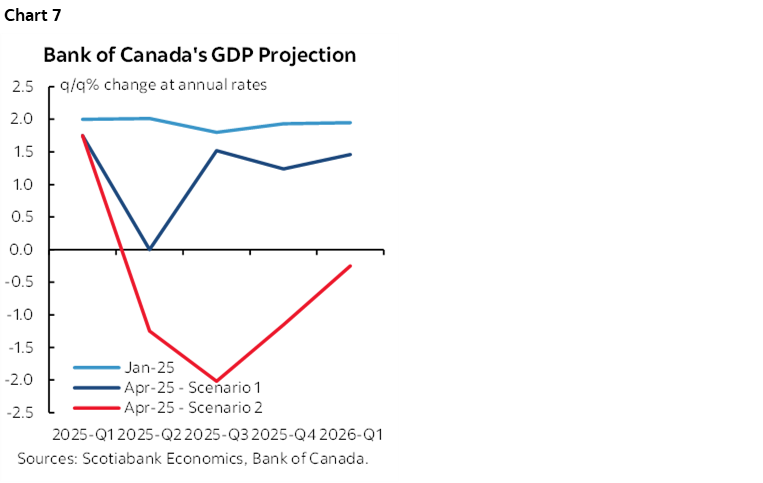

Key is that Q1 growth was higher than the BoC expected in either of its April MPR scenarios and warmer than they had previously forecast in the January MPR (1¾%). See chart 7. Furthermore, Q2 is very tentatively tracking slightly better growth than their ‘Scenario 1’ and much better growth than their feared ‘Scenario 2’ that are also shown in the same chart.

THE BROADER CASE TO HOLD

The case for holding the policy rate is based on much more than GDP. Here are a few points to consider.

1. Cut because of jobs?

- Some say so, but inflation is their mandate, not jobs, and the tie between jobs and inflation is tenuous.

- The BoC won't overreact to a limited number of job market readings with so many distortions (election, GST fiddling, weather).

- Real wage growth and wage settlements are still well above what productivity would merit.

- and the key is that I don't trust the Jan–April numbers one bit. About 50k ytd job growth is driven by statcan's choice to use the lowest SA factors on record for each and every month so far this year. Take historical average SA factors for each month instead and ytd job growth would be about 3.5–4 times more than officially reported (180k+). There is a strong recency bias to how they SA factors calculated that assumes the wonky seasonal patterns of the pandemic should still apply now. I don’t have faith that this is the correct thing for the data agency to be doing and therefore I think they are understating job growth by a material amount.

- those SA factors all turn to overstating jobs from June through August. Cut into overstated job growth figures??

2. Cut because of inflation?

- After 4.5% m/m SAAR trimmed mean and weighted median average inflation in April, the BoC would have to have very strong arguments for why inflation is headed to being down for the count if it chose to cut. I’m not convinced. And it’s not just a flash in the pan. It's a serial pattern stretching back over the past year. Canada hasn't come close to licking inflation. There has also been a recent increase in the breadth of rising prices.

- History trivia: Since its new reference rate was adopted in the mid-1990s, the BoC has never cut after the immediately preceding print for core inflation has been anywhere close to this level. The next closest was just over 3% and they almost always cut only after much weaker core inflation readings.

3. Cut because of demand side risks?

- That's mostly a reference to housing so far and you can't do anything about ytd housing. It has serious problems that rates can’t fix and that are best left to other policymakers and private industry to fix. Cutting rates to help housing a) isn’t assured of working versus facing inelastic demand, and b) may very well cause bigger problems elsewhere by sustaining inflation risk.

- There is very likely going to be weakness ahead on the demand side.

- But the same applies to the supply side through curtailed immigration policy, reduced confidence to invest, supply chains are getting rattled again etc.

- Don't make the same mistake! BoC's job is to align supply and demand, not just focus on one side. To ignore developments on the supply side is why so many got it so wrong in the pandemic and post-pandemic periods.

4. Markets aren't pressuring the BoC. That doesn't necessarily matter to them given their history of surprises, but it doesn't risk any negative market surprises if they whiff. Markets are giving them a pass to further reflect upon developments.

5. Fiscal easing. It's here now, in the form of ways and means motions. And there is a likely deluge of fiscal stimulus coming in a Fall budget to add to provincial measures. Fiscal policy is substituting for monetary easing. If anything, I’m worried Canada overdoes it again on fiscal stimulus which when combined with supply side challenges would risk a repeat of the inflation surge we’ve had.

6. Tariffs. There will be modest pass through via three channels. One is limited retaliation. More important may be pass through from crazy US import tariffs via their supply chains into Canada's. Three is the impact on supply chains and product availability that in some categories may be drying up as we speak. Until you know more about pass through via complex channels a central bank mandated to target low and stable inflation shouldn’t be doing anything.

7. Still no clarity on what to forecast and when. The BoC boycotted forecasts six weeks ago in favour of two scenarios and a shrug. I can't see them having more confidence in what to forecast and hence the appropriate course of action going forward now. If anything, I think uncertainty is higher now because of the fight between courts and the US administration and whatever emerges from it. They don't have to decide whether to forecast or not until the end of July's MPR. So for now, sit tight. If they cut, they'd have no framework to back it up.

8. Policy is already neutral, possibly even easy. 2.75 is in the middle of the 2.25–3.25 neutral band. It's not like the Fed. Plus they've already ended QT long ago. The BoC has more policy optionality.

9. Inflation expectations are also elevated. It's not just about actual inflation.

10. Go Oilers! Oh what the heck, that’s totally irrelevant to the discussion at hand, but we can’t be one short of ten on a list!

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.