- The Fed broadly met expectations....

- ...by hiking 25bps...

- ...and leaving options open into the June meeting...

- ...while leaning against rate cut pricing

The FOMC raised the fed funds target range by 25bps to 5.0–5.25% as widely expected but against tail bets they may have held unchanged. The Committee tweaked the forward rate guidance to retain optionality on whether to hike again. Chair Powell’s press conference emphasized that they are keeping options open in highly data dependent fashion into the June meeting. He was noncommittal toward whether they were signalling a pause, said it wasn’t considered for today, leaned against rate cut pricing and deferred further decisions to the June 13th–14th FOMC meeting. Overall this met my broad expectations for the overall tone that kept options open. This will further amplify market volatility around coming nonfarm and inflation reports along with monitoring developments across the banking sector.

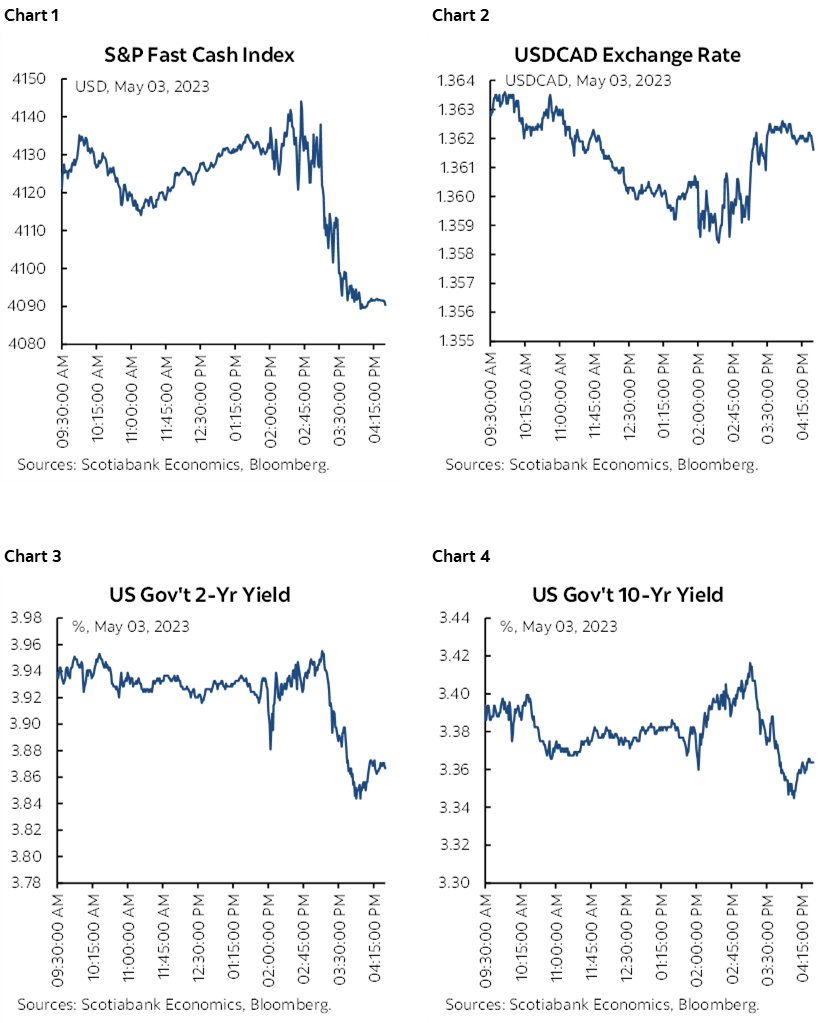

Charts 1–4 depict the reactions in financial markets from 2pmET onward. Stocks ended lower, the USD very slightly firmed versus crosses like CAD, and Treasury yields were volatile throughout the communications from 2pmET until about 3:20pmET but ended slightly lower. Further reaction into the Asian overnight session may be key.

STATEMENT CHANGES ENHANCED OPTIONALITY

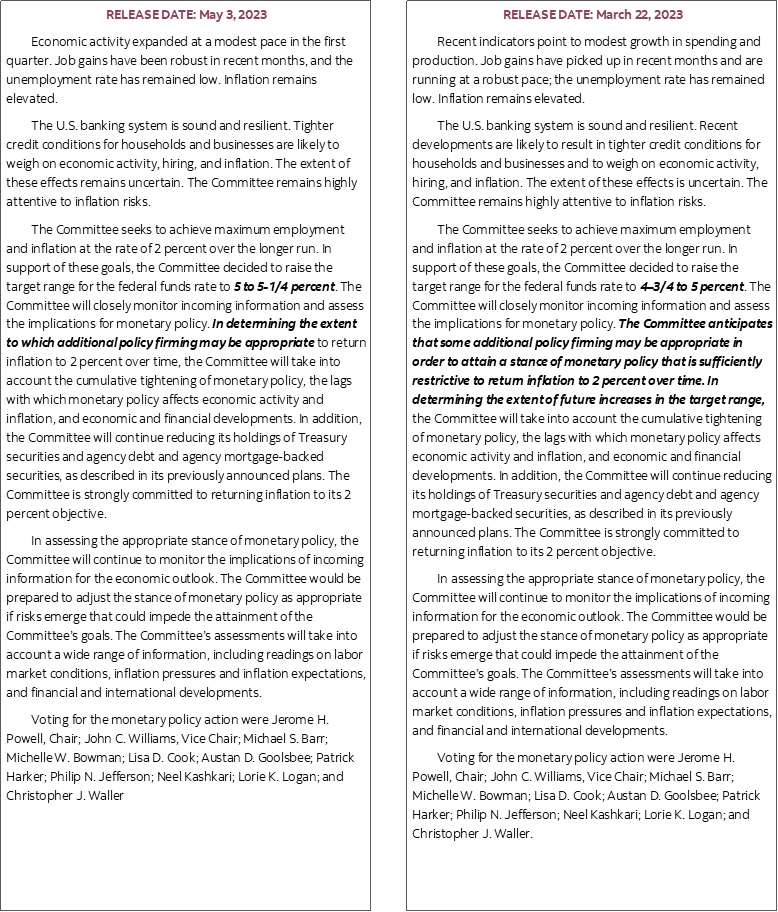

The accompanying statement comparison at the back of this note highlights the few key changes that were made compared to the prior version.

The description of current conditions and references to how tighter credit conditions are likely to weigh on economic activity, hiring and inflation were essentially unchanged.

Key is that the language around forward guidance for the policy rate was tweaked to make additional tightening more conditional while not ruling it out.

The relevant passage now says:

“In determining the extent to which additional policy firming may be appropriate….”

Which simplifies the prior statement’s reference that went as follows including the portion that is struck out in what is shown as it was not retained:

“The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the extent of future increases in the target range…”

The statement also indicated that the decision was unanimous.

POWELL CAME OUT SWINGING

Powell’s opening remarks during the presser set a mildly hawkish tone. He started with comments on banks and noted that “conditions have broadly improved since early March." He went on to emphasize their focus upon price stability and spelled out that “looking ahead, we'll take a data dependent approach to determining whether further tightening may be appropriate."

His opening remarks went on to describe how the "labour market remains very tight" after flagging how interest sensitive sectors are weakening but that there are some signs that supply and demand in job markets are moving back toward balance but overall demand still exceeds the supply of available workers.

Powell noted that "inflation pressures continue to run high and the process of getting inflation back down to 2% has a long way to go" while inflation expectations remain anchored.

He elaborated upon how the FOMC is viewing credit conditions by stating that “the economy is likely to face further tightening from credit conditions" and that "the strains that emerged in early March appear to be driving even tighter financial conditions for households and businesses but the effects remain uncertain."

Powell said that in light of these uncertainties they will be data dependent over time and in reference to possible further hikes said that "we will make that determination meeting by meeting based on the totality of the incoming data but we are prepared to do more if monetary policy restraint is needed."

He sounded skeptical toward the progress that has been achieved toward getting inflation down to 2% thus far by noting that "reducing inflation is likely to require a period of below trend growth and some softening of labour market conditions" which hasn’t really begun as of yet.

NO SUPPORT FOR A PAUSE TODAY

Chair Powell was asked whether they considered a pause today and said no. Specifically he said “Support for the 25bps increase was very strong across the board. People did talk about the possibility of pausing but not at this meeting. There is a sense we're getting close or maybe even there but that's going to be an ongoing assessment."

GUARDED AGAINST SIGNALLING A FUTURE PAUSE

When asked whether he was signalling a pause, Powell flatly said "A decision on a pause was not made today. We will be driven by incoming data meeting by meeting and will approach that question at the June meeting."

When asked again, he said “The assessment of the extent to which additional policy firming may be required is going to be determined meeting-by-meeting.”

In case the reporters in the room were hard of hearing, his response to whether the bar is now set higher to tighten further he said “I can't really say. We can look at the data and make a careful assessment.”

Powell did leave open the possibility they may be done by stating that they may be at their peak policy tightening through the combination of tools they have been using, or close to it.

RATE EQUIVALENCE

Powell was asked whether he has changed his prior guesstimate that the rate equivalence to credit tightening since banking turmoil began from a quarter point but with high uncertainty and said “It isn't possible to estimate. We have to be honest and humble about our ability to estimate. Conceptually we think we won't have to raise interest rates quite as high than if this had not happened, but the extent is uncertain.”

IS THE FED SUFFICIENTLY RESTRICTIVE NOW?

When asked whether dropping reference to tightening until conditions are “sufficiently restrictive” meant they believe they are now sufficiently restrictive, Powell said “It's not possible to say that with confidence now. You will note that the SEP in March indicated that the median participant thought today's action would be the ultimate level for the policy rate. We don't know that now until we get to the June meeting.”

LEANED AGAINST MARKET PRICING RATE CUTS

Powell was asked whether he was inclined to rule out the rate cuts that markets are pricing by the end of the year and while he did not rule them out he set a high bar for doing so by stating the following:

“We on the Committee have a view that inflation is going to come down not so quickly and that it will take some time. In that world if the forecast is broadly right then it would not be appropriate to cut rates. If you have a different forecast then it may be, but that's not our view. We think demand will have to weaken and the labour market will have to cool in order to achieve lower inflation."

He also said that they "will want to see a few months of data" that they are achieving 2% inflation and that they are not close to that yet. He went on to note all of the false signals that inflation is ebbing that we have seen in recent years and how they have to be careful not to reach premature conclusions.

OPTIMISM AROUND THE RECESSION DEBATE

When he was asked whether Fed staff have revised their forecasts for a mild recession, he explained that there are a variety of views at the Fed and that “My own assessment is that the economy will continue to grow mildly this year."

Powell went on to express amazement toward the strength of the labour market and suggested that this cycle’s response to tightening could prove to be different than in past periods which has been an argument I’ve been advancing. He said “It wasn't supposed to be possible for job openings to decline as much as possible without unemployment going up but it's happening. It's possible we will have a cooling in the labour market without big job losses. That would go against history, but I think that with so much excess demand with wage gains moving down still makes it possible. The case of avoiding a recession is more likely than the case of having a recession that I don't rule out either."

DEBT CEILING DISCUSSED

When asked to comment on the debt ceiling and its possible effects, Powell gave a sanitized and predictable response and said “These are fiscal policy matters for the elected representatives to deal with. It is essential that the debt ceiling be raised in a timely way. A failure to do that would be unprecedented and quite averse. No one should assume that the Fed can protect against the failure to pay our bills on time."

When asked whether a possible debt ceiling standoff affected their decision today, he said “I wouldn't say so, it came up, but I wouldn't say it was a factor in today's decision.” I’m not sure one should have expected a different answer!

PREDICTABLY AVOIDED PICKING WINNERS IN BANKING

Powell was asked whether further consolidation in the banking sector would increase or decrease financial stability and whether he had any concern about the biggest bank getting bigger. His answer was predictable for a Fed boss who serves as one of the regulators of a vast array of banks. He cited evidence on the ongoing consolidation trend over a long period of time from 14k banks earlier in his career to 4k now. He went on to emphasize that it's healthy to have a range of different kinds of banks (imagine a Fed boss saying otherwise...) and that “It's probably good policy that we don't want the largest banks doing big acquisitions but this is an exception that is a good outcome for the system. Ultimately the law says it has to go to the least cost bid” in reference to JP Morgan’s acquisition of First Republic.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.