- High odds that the BoC hikes again in June with July as a backup option

- Core inflation gauges are reaccelerating

- No further set up is required

- CDN CPI m/m % / y/y %, April:

- Actual: 0.7 / 4.4

- Scotia: 0.5 / 4.2

- Consensus: 0.4 / 4.1

- Prior: 0.5 / 4.3

Canadian inflation surprised higher than expected on the headline and underlying measures and details. The result vaulted the Canadian dollar to the top of the heap versus major crosses to the USD and CAD would have been stronger yet if not for strong US data (retail sales, industrial output) that drove broad USD strength. Canada’s rates curve is getting crushed with a double digit increase in yields across most maturities concentrated in a 14bps spiked in the two-year yield on the day. OIS markets bumped up terminal rate pricing post-data and rate cuts have been wiped off the map for the rest of the year’s meeting calendar.

So far so good. Guidance to lean against an overvalued front-end has worked but now faces the debate over whether it’s mission accomplished for the BoC or if further hikes are required. I think they have more work to do.

CORE INFLATION IS ACCELERATING AGAIN

Headline inflation landed at 0.7% m/m NSA and 0.6% m/m SA which was hotter than my slightly above-consensus estimate. The concern runs much deeper than headline inflation.

At the heart of the matter is the need to look at the figures in the correct way by examining core price pressures in the highest frequency manner possible and by considering the breadth of price pressures. That’s not the year-over-year rates.

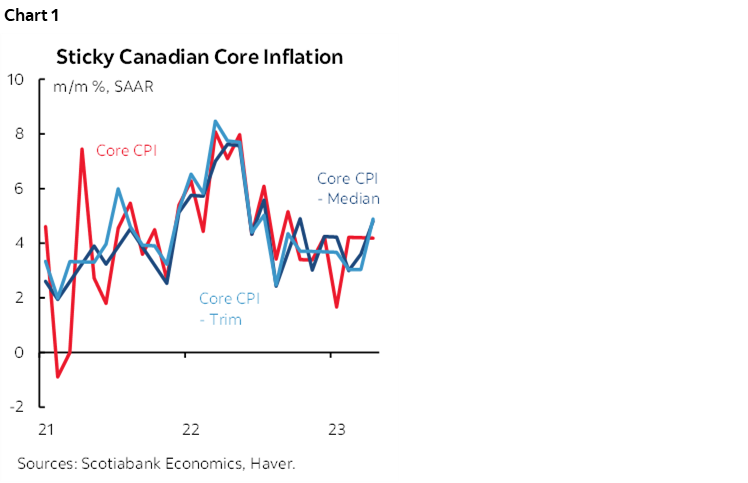

Enter chart 1. It shows three measures of core inflation at m/m seasonally adjusted and annualized rates. They are all running at a four-handled pace. Traditional core CPI was up by 4.2% m/m SAAR. Weighted median CPI was up by 4.8%. Trimmed mean CPI was up by 4.9%. Even headline all-in CPI was up by 7.2% m/m SAAR.

These measures suggest that inflation continues to run far above the BoC’s 2% headline target. Core inflation ebbed from the peak rates early last year, but these preferred measures have been remarkably sticky since then.

...WITH HIGH BREADTH...

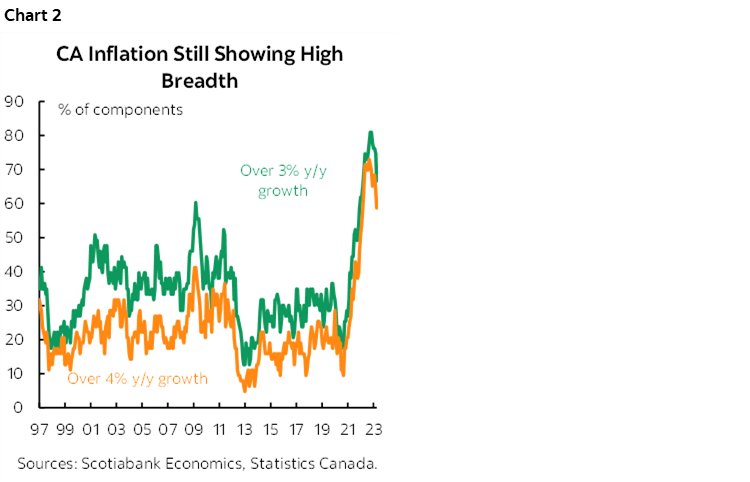

Breadth to even the year-over-year rates remains exceptionally high (chart 2). 67% of the CPI basket continues to increase by over 3% y/y. 59% of the basket continues to rise by over 4%. 44% of the basket is still rising by over 5%.

...AND UPWARD REVISIONS...

As if forecasting isn’t difficult enough. Revisions destroyed the credibility of the BoC’s common component CPI that they no longer even reference. Traditional core CPI was just revised up from 3.4% m/m SAAR in March to 4.2% in March for an eight-tenths upward revision. Trimmed mean and weighted median were left intact. Our shop believes simple traditional core CPI inflation is the superior gauge and therefore core inflation has been hotter than previously understood.

...AS THE INFLECTION POINT HAS ARRIVED

Furthermore, I continue to think that Canadian core inflation is at an inflection point toward persistently higher inflation risk.

- No material progress is being made to open up disinflationary slack in the economy or labour market. Estimates vary depending upon what gets fudged, but the BoC’s April MPR estimated that the output gap was still in net excess demand at between 0.25% to 1.25% in 2023Q1. There are long lags after opening up slack for disinflationary forces to occur and that process has not even begun for those who believe output gaps are the bee knees. I don’t.

- In my opinion, we can’t put much stock in a Philips curve framework that has underestimated out of sample pressures during the pandemic era.

- Housing is on a tear again which is directionally consistent with arguments I’ve given for why this would happen and why consensus was too bearish toward housing dating back to last year. The problem is that I didn’t think it would happen by quite this magnitude and this soon with much of the Spring housing market still ahead of us along with longer-wave influences. For starters, there is practically no inventory on either the new build or resale sides of the market. That’s a problem with surging immigration as the country put little thought into where to house all of these new arrivals. A domestic demand story is getting a lift from first time home buyers that are ready to pounce with bigger down payments on cheaper prices. Another stimulus program was introduced on April Fool’s Day. Job markets remain very tight. Expected capital gains are driving FOMO behaviour and the renewed risk of extrapolative behaviour that would concern the BoC. I think this combination is bringing the return of rampant speculation in Canada’s housing market that pre-adjusted to some of the higher rates on the originations part of the picture through the B20 mortgage stress test. The direct effect on Canadian CPI is likely to turn positive going forward alongside spillover effects.

- Wage pressures remain well in excess of Canada’s moribund performance on labour productivity. Collective bargaining is putting upward pressure on wage settlements and setting wage gains above the 2% target for years to come.

- The BoC’s measures of inflation expectations continue to indicate pressures well above the 2% inflation target for years to come.

- The broad macro backdrop has a number of supporting arguments that can drive resilience.

- There isn’t enough evidence that domestic lending conditions are tightening rapidly or significantly enough to do the BoC’s work at the margin. Apparently folks are able to get the requisite mortgages!

Overall, recent data has reinforced the narrative that I have been communicating to clients throughout this year that the Bank of Canada’s job is not finished after it quit hiking too early back in January. There is a highly compelling case for returning with a hike at the June meeting and if not then July’s odds go up. I would assign high market probability to a June hike with info to this point.

NO SET-UP REQUIRED

I don’t believe that the BoC thinks it has to hold anyone’s hand in setting up a hike with explicit guidance. After all, it surprised on three out of eight meetings last year!

Furthermore, Governor Macklem could well say that he has provided enough forward guidance in any event. I won’t repeat the arguments here, but what they have said to this effect is spelled out here and in subsequent communications. Perhaps we’ll hear from him on Thursday, but he has tended to divorce monetary policy discussions from that day’s planned focus on financial stability.

DEBT CEILING BASE CASE

Obviously if the US defaults on its obligations then all of our forecasts go straight back to the drawing board in a dire scenario, but I don’t find that to be a reasonable base case. Our base case assumption is that the US debt ceiling eventually gets resolved after some market turbulence. It may be settled by the June 7th BoC decision or kicked down the road. We are assuming there will be no default and that market turbulence will be transitory. Therefore, absent material default risk, Canadian monetary policy should be crafted with domestic conditions in mind and while considering idiosyncratic drivers unique to the country—while being prepared to adjust to a possible tail event if needed. US politics will remain dysfunctional for a long while yet and cannot hold up BoC policy.

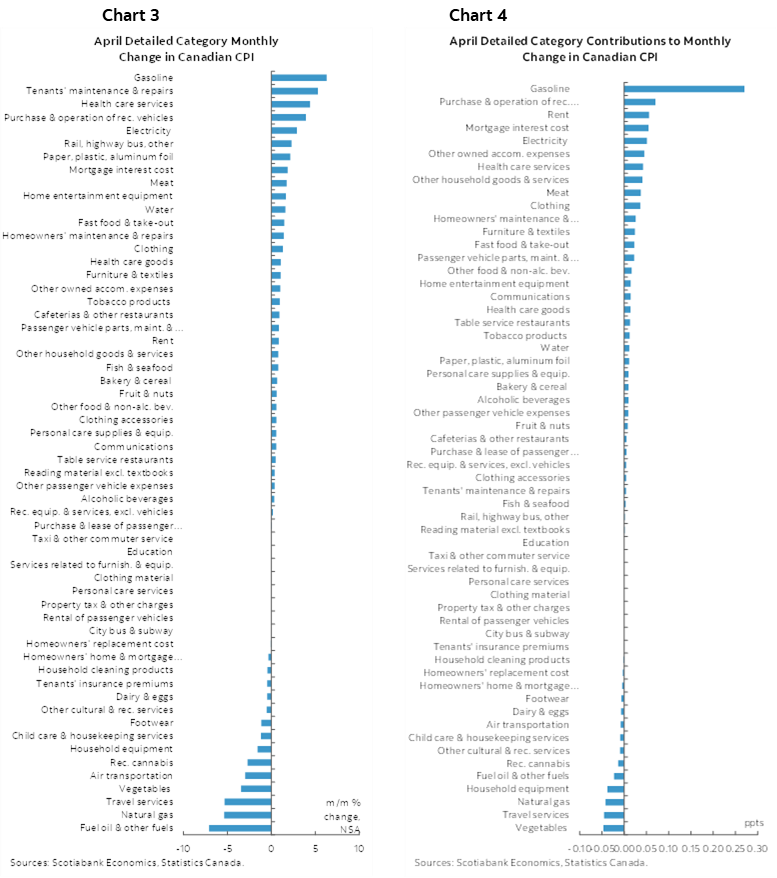

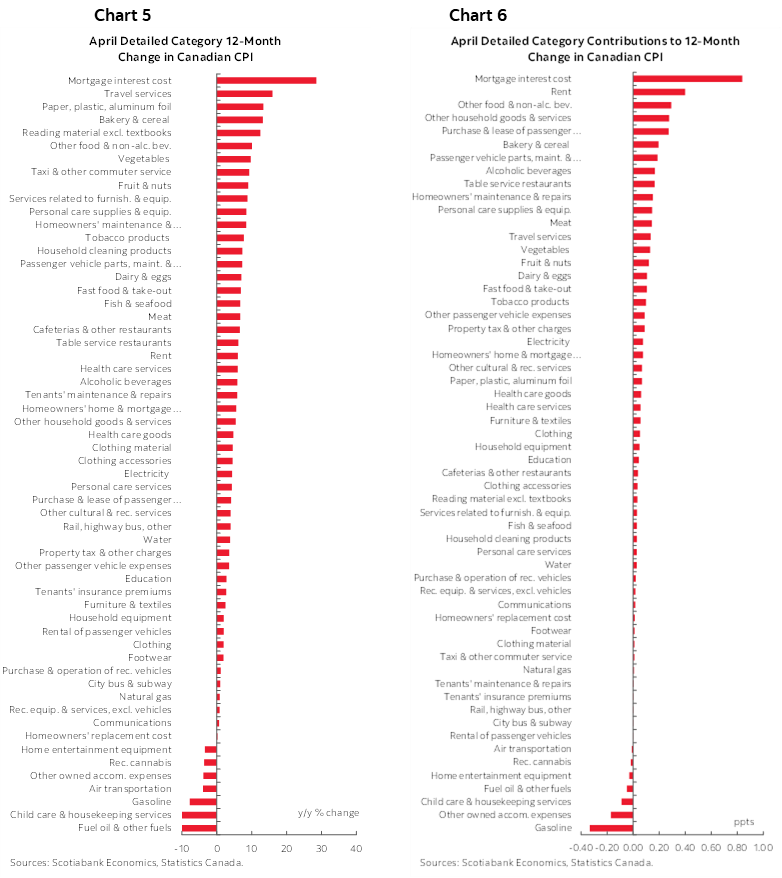

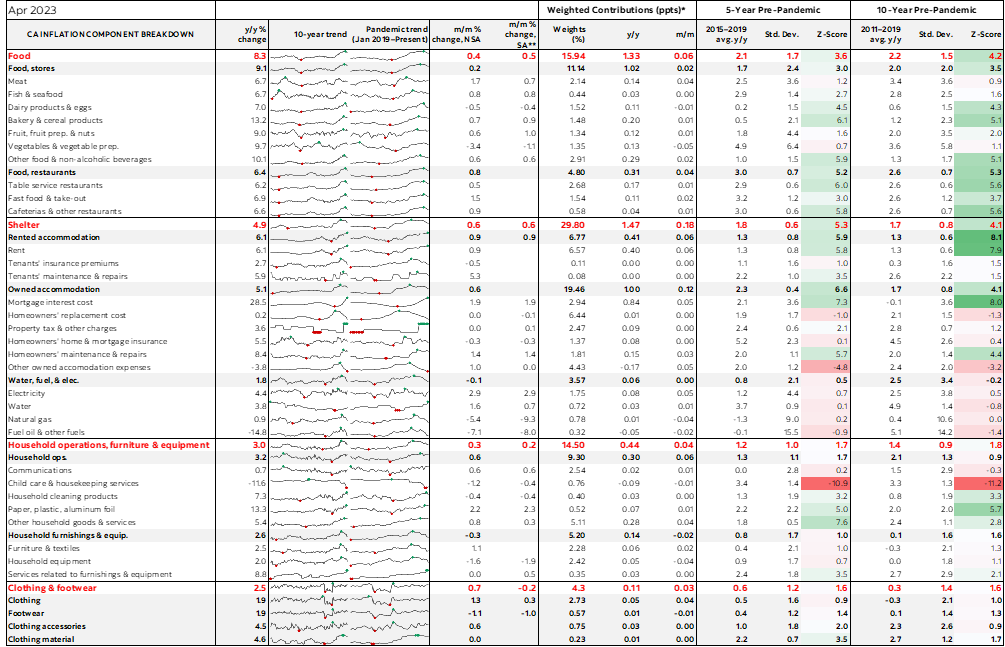

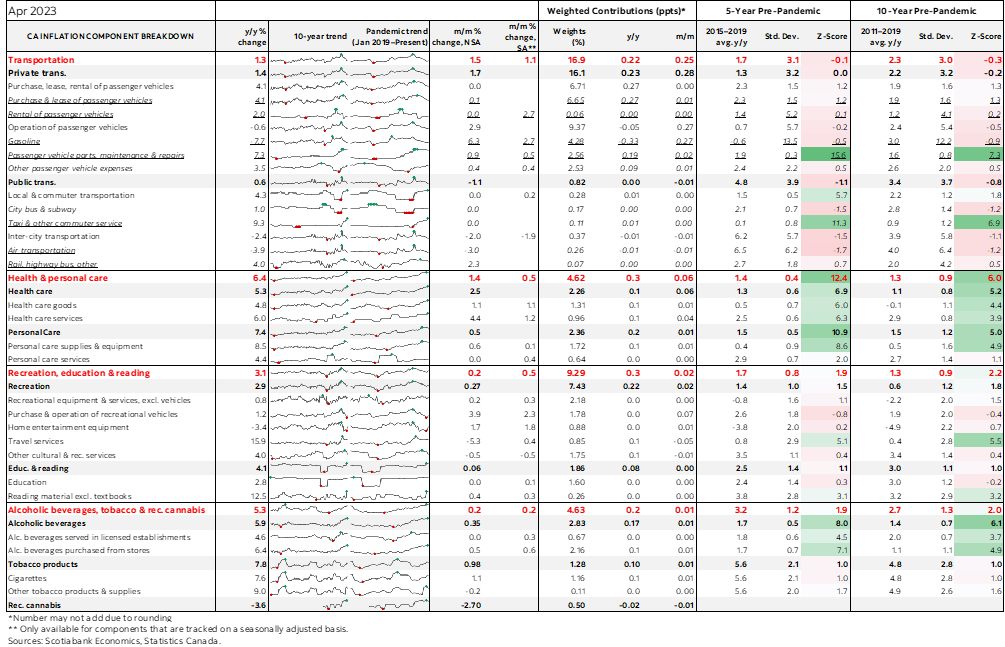

For further details please see the accompanying table showing the breakdown of the CPI basket along with micro charts and z-score measures of deviations from historical tendencies.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.