- Core CPI was a smidge lighter than expected, but largely ignored by markets

- US CPI, headline/core, m/m % April, SA:

- Actual: 0.22 / 0.24

- Scotia: 0.3 / 0.3

- Consensus: 0.3 / 0.3

- Prior: -0.1 / 0.1

Stale CPI was a touch lighter than expected. At 0.24% m/m, core CPI was on the heavy side of 0.2 and one one-hundredth away from rounding up to the 0.3% consensus call.

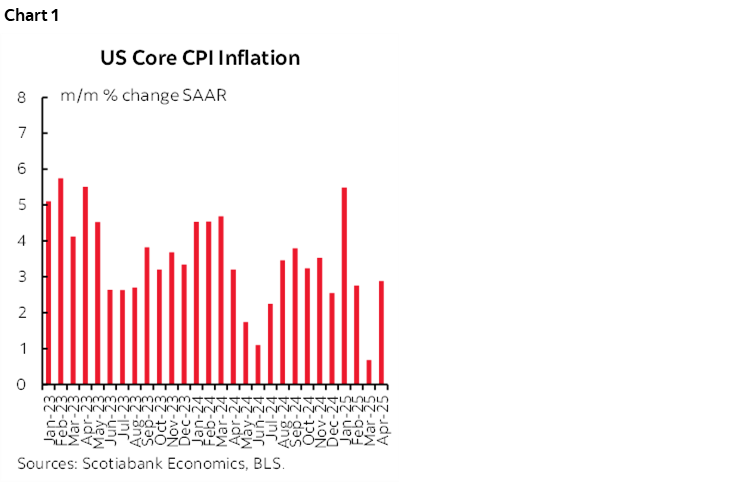

At 2.9% m/m SAAR in April, 0.7% in March, 2.75% in February and 5.5% in January, don’t expect the FOMC to describe ytd underlying inflation as being light (chart 1). They'll still emphasize above-target underlying pressures for core CPI, and for core PCE that arrives on May 30th. At 2.6% y/y in March, core PCE was still on the high side.

Having said that, it’s the last CPI print before things begin to get more interesting through incorporation of tariff effects over coming months. Hence stale.

That’s probably why markets largely ignored the readings. The 2-year Treasury yield is down 1bp with June still a hold. The dollar is flat. S&P futures were basically unchanged.

The FOMC—particularly Chair Powell—also won’t much care about the figures. They want reams of dual mandate data in order to be able to determine whether policy effects—namely from tariffs—cause more of a departure for price stability or full employment goals before determining what to do. That is likely to take a long time yet, and year-to-date data doesn’t matter in that regard versus forward-looking risks. And so I’ll keep this one brief with the usual top notch help from Jay Parmar.

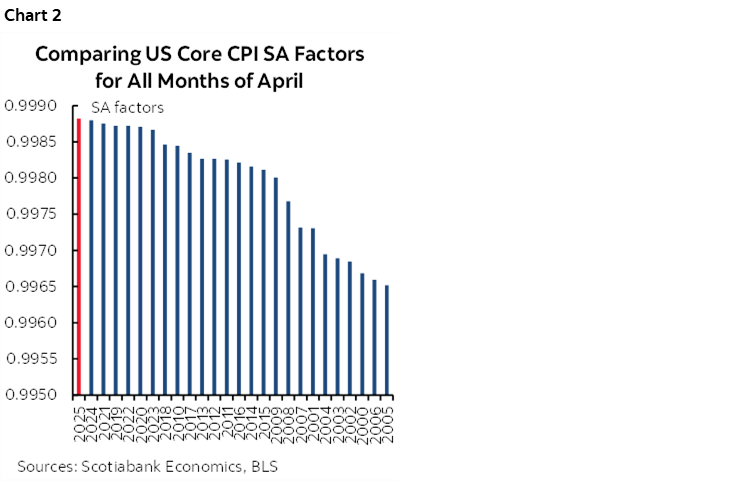

Even at a hair beneath consensus, core CPI was overstated by a new record high SA factor when comparing like months of April over time (chart 2).

Core goods prices (ex-food and energy) were soft at 0.1% m/m SA which was mildly firmer from -0.1% previously, but several categories are likely to be hit by tariffs going forward.

Core services CPI (ex-shelter and energy services) was up 0.2% m/m SA from -0.2% prior.

Shelter CPI performed about as expected at 0.3% m/m with primary rent up 0.3% and owners’ equivalent rent up 0.4%.

Several other goods categories were light but awaiting tariff effects that could also move through services.

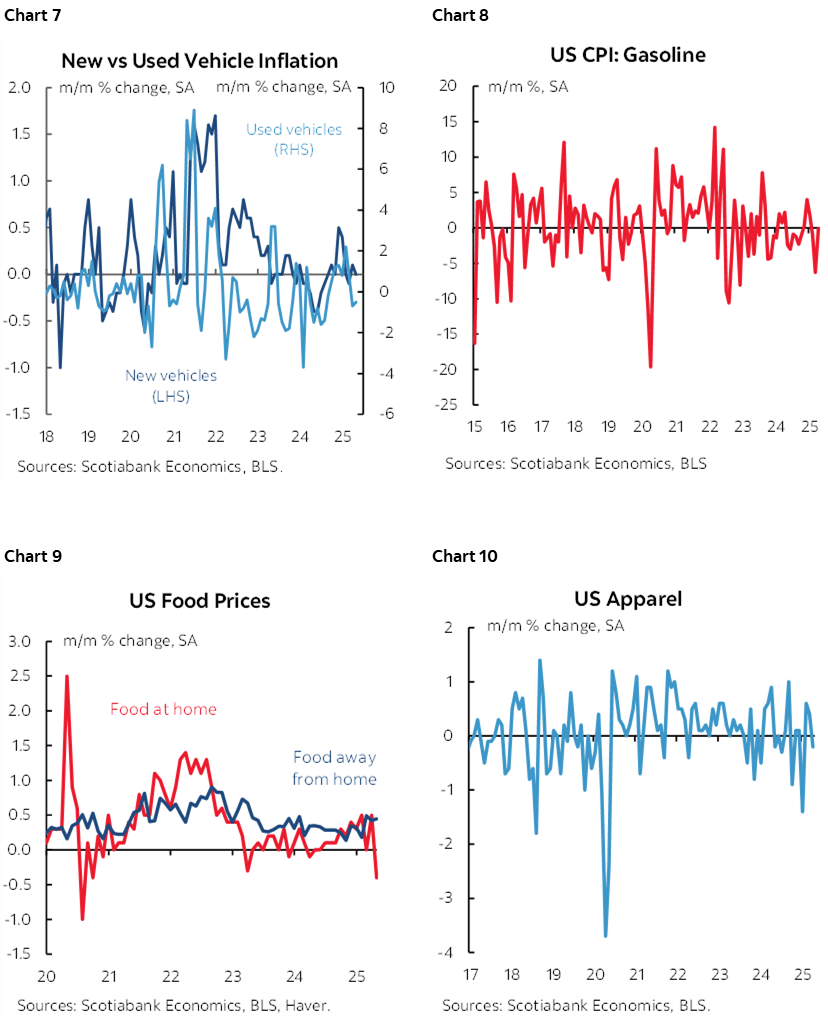

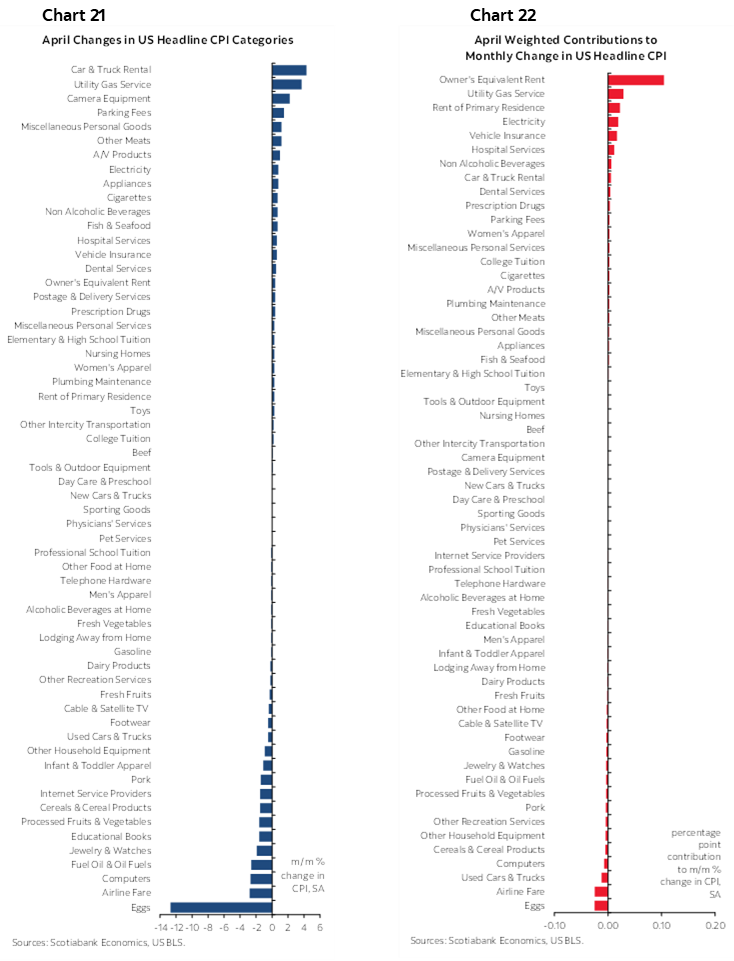

Vehicles were softer than expected with new vehicle prices flat (about as expected) but used vehicle prices were down 0.5%. Just wait for tariff effects on new vehicle prices and for substitution effects to raise used vehicle prices.

Clothing prices slipped -0.2%. Again, wait for tariffs.

Food was surprising at -0.1% m/m and led by groceries (-0.4%) but again, just wait for tariffs. Food away from home (restaurants, take-out etc) was up 0.4% and also likely to be hit by tariff pass through effects.

Gasoline prices were soft at -0.1% and inconsequential to the report as expected.

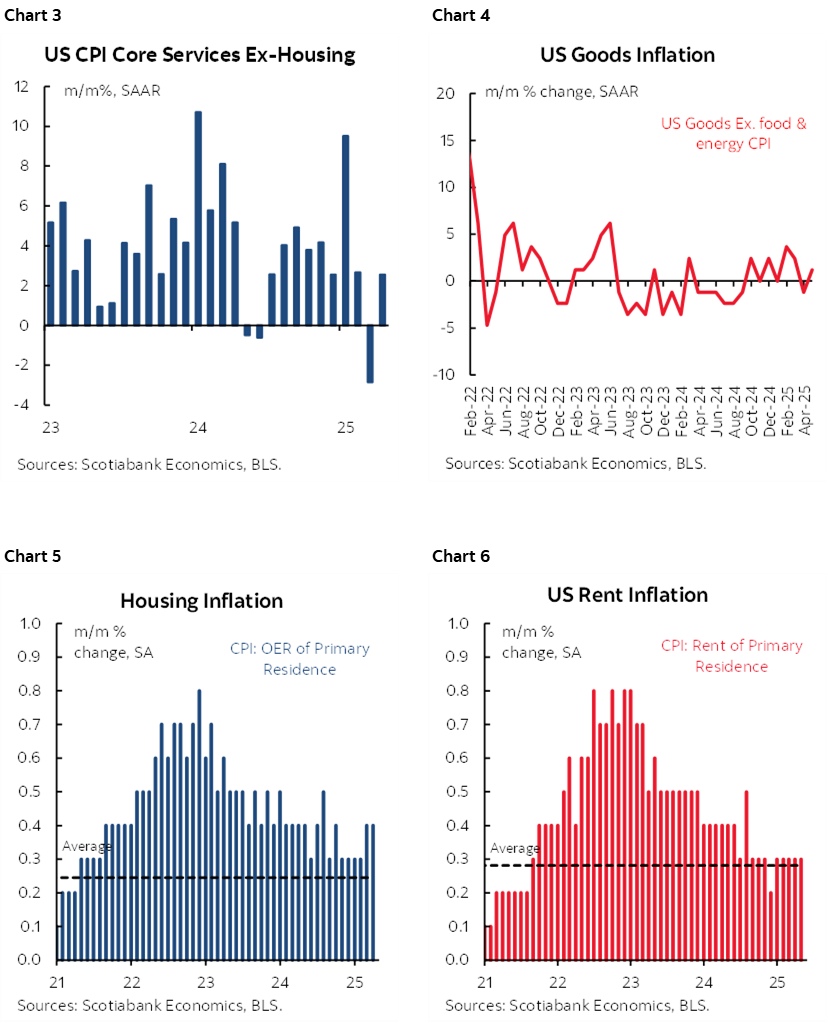

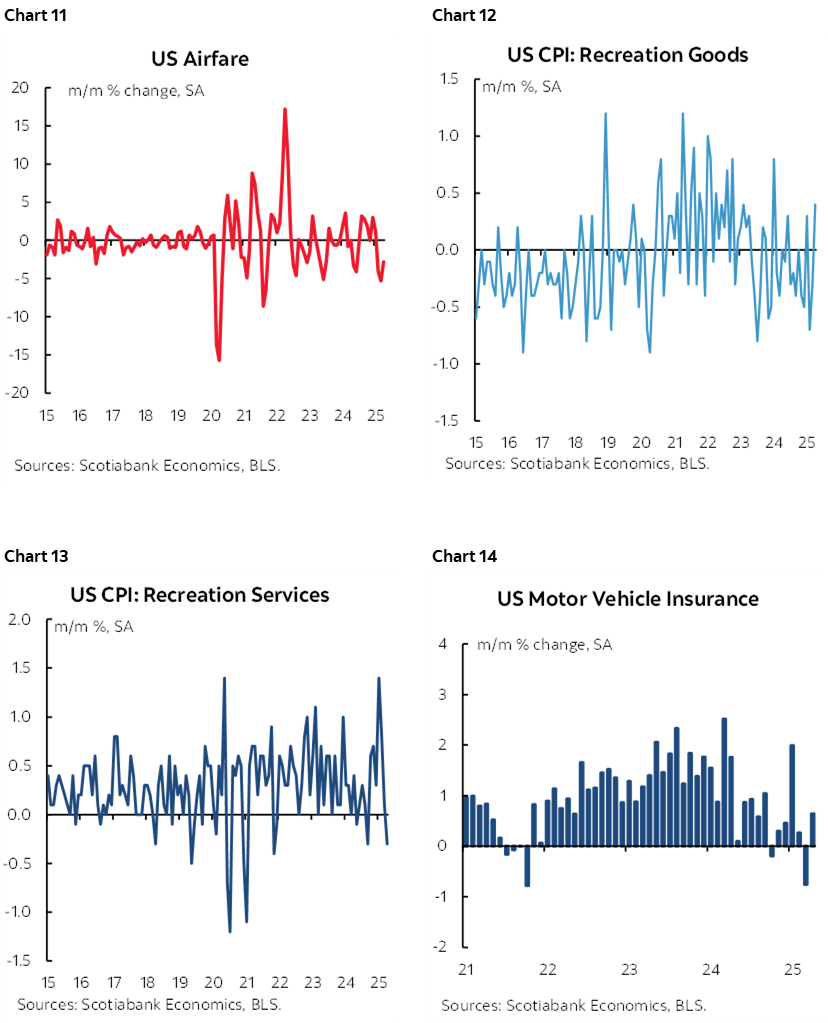

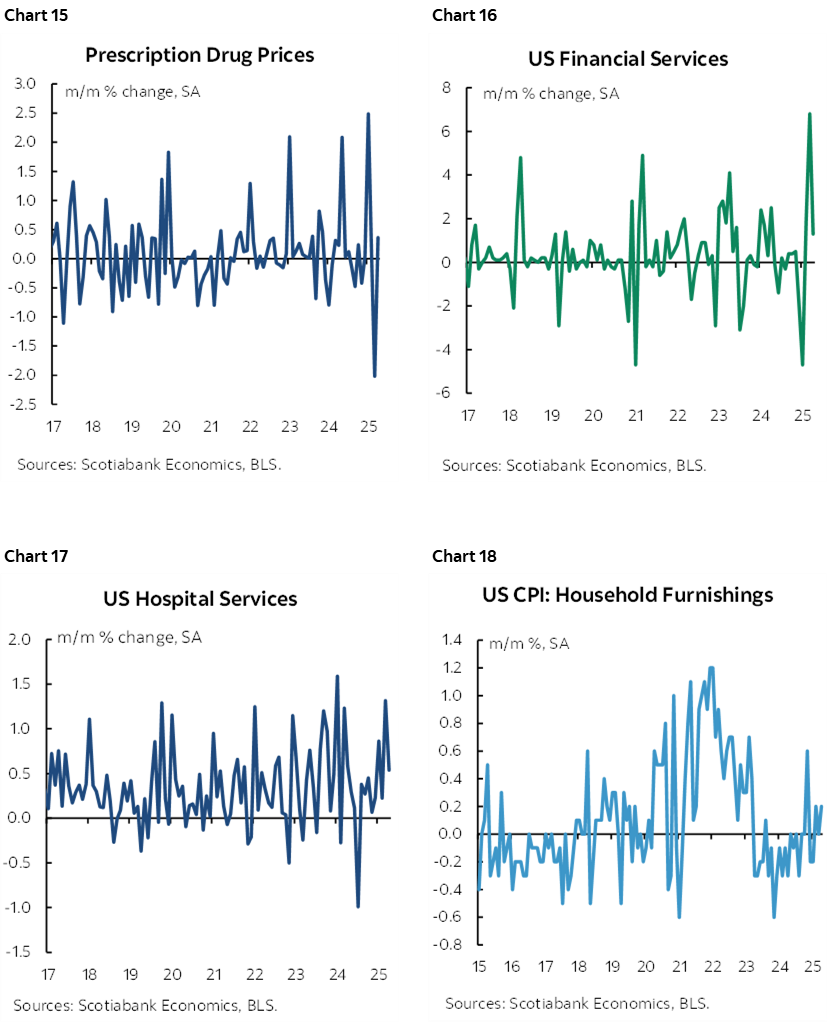

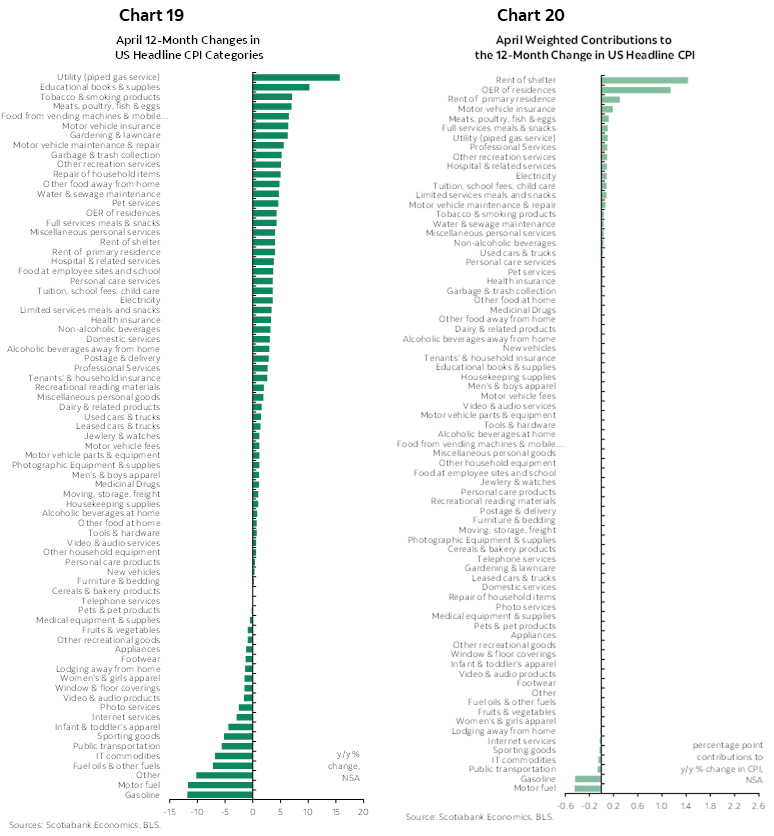

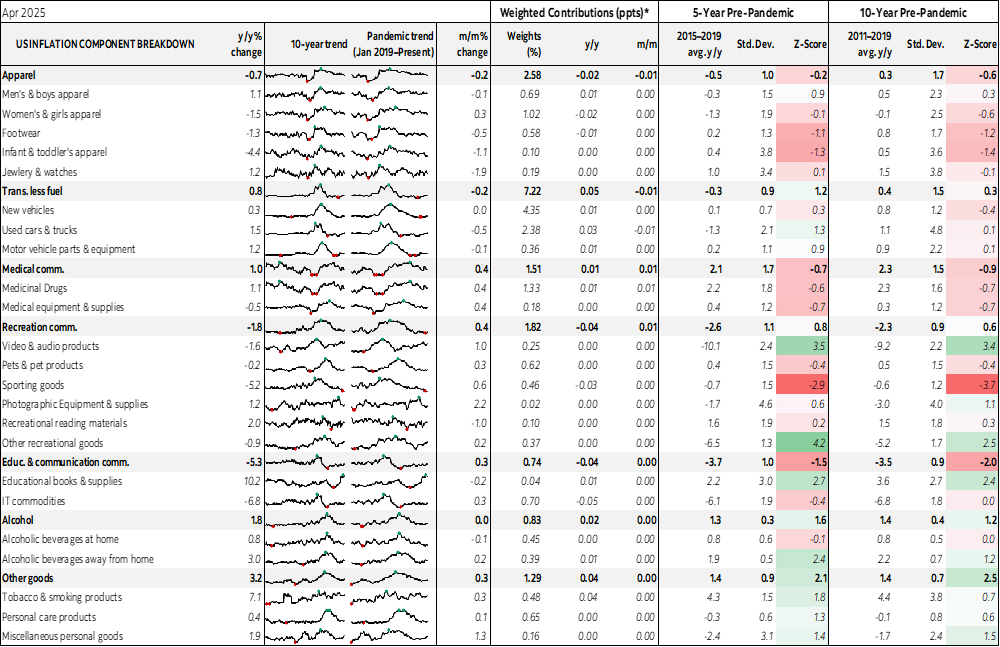

Please see charts 3–18 for individual component charts, charts 19–20 for y/y break downs of the basket and weighted contributions to total y/y CPI, charts 21–22 for the m/m equivalents, and finally the detailed table including micro-charts.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.