- The policy rate was left on hold as expected

- The BoC still warns that rates may go move higher if needed...

- ...but the rest of the statement indicates they don’t really believe it...

- ..and so financial conditions eased...

- ...and CAD remains a one way weakening bet

- Developments will come to challenge what the BoC did today

- BoC overnight rate, %:

- Actual: 4.5

- Scotia: 4.5

- Consensus: 4.5

- Prior: 4.5

The Bank of Canada left its policy rate unchanged at 4.5% as universally expected including by Scotiabank Economics.

The bias may prove to be a different matter altogether. As the Fed contemplates a potentially more hawkish data dependent turn, the Bank of Canada took a step in the opposite direction in this morning’s statement.

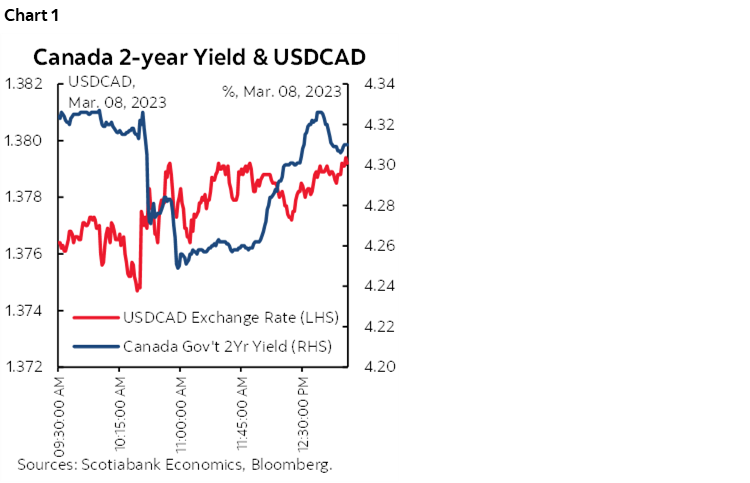

The result was a mild easing of financial conditions marked by a rally in shorter-term Canadian rates as the two-year Government of Canada bond yield moved lower while the two-year US yield is higher on the day. CAD depreciated as USDCAD marches toward 1.39 in the aftermath. That would match the level that triggered Macklem’s caution last October that rates would have to compensate. See chart 1 for intraday movements.

CAD depreciation would have been even greater had Chair Powell not reined in some of yesterday’s rally in the USD and the sell-off in shorter term US rates by emphasizing in his testimony before the House this morning that “no decisions have been made” as the Fed watches key upcoming reports like payrolls and CPI. That was clear in the conditionality he placed on forward guidance yesterday but I guess markets needed to hear it more clearly. Should those US reports land broadly in line with expectations, then CAD’s vulnerability could be higher as the figures roll in partly on the Fed bets and partly on the interpretation of the BoC’s statement today.

On balance, I think the BoC is vulnerable going forward and still position the risk to the policy rate moving higher. Explaining why requires parsing through the key changes in the statement starting with hawkish signals and then how the statement took them back.

OPEN TO FURTHER HIKES, BUT NOT REALLY

The BoC repeated guidance that it “is prepared to increase the policy rate further if needed to return to the 2% target. The problem is that the rest of the statement indicated they really don’t believe it but perhaps felt they had to throw it in to a further premature easing of financial conditions. The rest of the statement watered down this commitment.

ACKNOWLEDGED EXTERNAL STRENGTHS

The statement did say that they think developments for growth and inflation in the US and Europe “are both somewhat higher than expected” in the January MPR. They go on to note that “...labour markets remain tight, and elevated core inflation is persisting.” Other external references are unchanged and continue to note upside risk to commodity prices due to China’s rebound and the war in Ukraine.

LOOKING THROUGH Q4 GDP

The BoC did encouragingly acknowledge that Q4 GDP wasn’t as weak under the hood as the headline indicated which is encouraging since had they not done so then it would have signalled greater concern and dovishness. They did so by noting:

“In Canada, economic growth came in flat in the fourth quarter of 2022, lower than the Bank projected. With consumption, government spending and net exports all increasing, the weaker-than-expected GDP was largely because of a sizeable slowdown in inventory investment.”

That’s consistent with how I viewed the figures. They could have also gone one step further, however, and noted the list of temporary distortions to December GDP that made it a negative when absent a US oil spill that shut Canadian oil flows, two train derailments and harsher than usual weather effects the month would have been a solid plus, but they either chose not to or neglected to do so.

STRONG DOMESTIC LABOUR MARKETS

The statement noted that labour markets remain “very tight” and that job growth has been “surprisingly strong.” They reference wage growth at 4–5% using y/y figures, and how “productivity has declined in recent quarters.” That is also relatively hawkish.

EXCESS DEMAND IS GONE ALREADY?

As for the dovish take-back, first up is that they suddenly think that after one GDP report the Canadian economy has wiped out excess demand. We can see that through omission since gone are two references in the prior statement to how the economy remains in excess demand. If that’s an oversight, then it’s a pair of pretty big ones and not something that I believe in. Let’s see if they fudge potential GDP and update neutral rate estimates.

NOT WORD ON A LIKELY Q1 REBOUND

Second, the BoC may be leaving guidance on Q1 GDP to the April MPR, but what concerns me is the line about how they expect “weak economic growth for the next couple of quarters.” Eventually that’s possible, but if they include Q1 in “the next couple of quarters” then that might be inappropriate.

That’s because I think Q1 could rebound much more quickly than the 0.5% q/q SAAR growth forecast they had in the January MPR after the Q4 disappointment when it was flat versus their 1.3% forecast. They may have to punt some of the Q4 disappointment into a stronger Q1. This morning’s trade figures offer a strong net addition being tracked in terms of Q1 GDP. The reversal of temporary effects on December GDP may support this rebound. The biggest inventory drag effect on GDP growth in 40+ years could also stabilize or be a net addition to growth in Q1.

But meh, they didn’t even reference Q1 tracking. I think they may be vulnerable to an upside surprise. That could also mean that while it’s highly unlikely that the economy is no longer in a state of excess demand, a Q1 GDP rebound would make striking out such references all the more curious in nature.

PRICING POWER WILL EASE?

Third, they indicate that they expect pricing power to diminish. This comes in the following remark:

“With weak economic growth for the next couple of quarters, pressures in product and labour markets are expected to ease. This should moderate wage growth and also increase competitive pressures, making it more difficult for businesses to pass on higher costs to consumers.”

If Q1 GDP rebounds and given ongoing strength in the job market and awful productivity then the case for sustained evolution of core inflationary pressures toward the 2% headline target may be stated prematurely here.

NO SIGNS THEY ARE FUSSED BY CAD

A further case for this argument is that apparently, CAD isn’t enough of a concern to the BoC just yet. We’ll see what SDG Rogers says about it tomorrow if anything. The only reference was to strike out how the C$ “has been relatively stable against the US dollar” and replace it with “…the US dollar has strengthened.”

If the Fed is on the march to 6% and the BoC is turning dovish at the margin then CAD has 1.40 in its sights. That will challenge the BoC’s assertion that it will be more difficult to pass on cost pressures. I think they did a misstep here and are sitting ducks to currency traders.

STILL SUBSCRIBING TO THE BASE EFFECT HOAX

The BoC says that 3% inflation by mid-year lies ahead. They’ve learned nothing about putting too much stock in base effect distortions. That’s what misled them in 2021 when they dismissed inflation as driven by weakness the prior year and nothing more. Now they’re emphasizing how year-ago base effects will drag inflation lower.

“Both will need to come down further, as will short-term inflation expectations, to return inflation to the 2% target.”

CONCLUSION

In all likelihood the BoC probably continues to think that the key risks surround services inflation, productivity and wage growth as Governor Macklem emphasized in his recent speech in Quebec City. There were not many statement-codified indications of this, however, and there were enough curious twists that lead me to think this story isn’t over yet. Apparently markets continue to agree as they continue to price a full quarter point rate hike by summer. If the BoC comes back at all, then it won’t be for just a quarter point in my view, but putting down such a market placeholder remains prudent between binary options of no change and 50–75bps of further hikes.

Please also see the attached statement comparison.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.