- Inflation continues to surprise BoC forecasts…

- ...and it’s high time they stopped fooling around with token measures…

- ...in favour of expedited tightening at the April meeting

- Coming changes to basket weights should cancel out effects on inflation…

- ...but the coming addition of used vehicles to the basket will add to inflation…

- …as Canadians could be staring at +/- 8% inflation by summer

Canadian CPI, m/m / y/y %, February:

Actual: 1.0 / 5.7

Scotia: 1.0 / 5.7

Consensus: 0.9 / 5.5

Prior: 0.9 / 5.1

Canadian core CPI, y/y % change, February:

Average: 3.5 (prior 3.3 revised up from 3.2)

Weighted median: 3.5 (prior 3.4 revised up from 3.3)

Common component: 2.6 (prior 2.4% revised up from 2.3%)

Trimmed mean: 4.3 (prior 4.0)

Canadian inflation continues to surpass the Bank of Canada’s expectations and that likely amplifies the risk of a 50bps or larger hike at the April meeting. Momentum and breadth are both very high with further pressure ahead as Canadian monetary policy is far behind the curve.

Headline inflation landed a little above consensus expectations and on my expectations for the month of February as shown in the tables above.

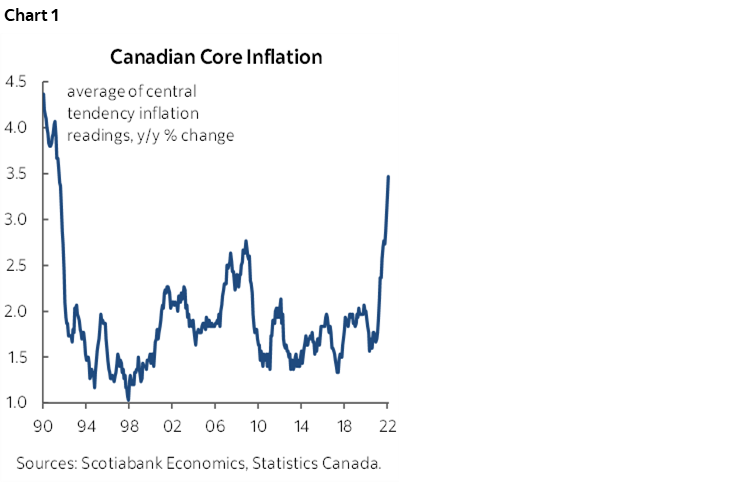

Average core inflation moved up three tenths from the prior month’s original estimate that itself was revised up by 0.1% for January and with February’s average core adding another two-tenths to land at 3.5% y/y.

That is the hottest average core measure since June 1991 (chart 1). We can safely say that inflation is not just being driven by a few price categories given that the central tendency measures that are being averaged here include trimmed mean, weighted median and common component CPI that are by nature designed to weed out narrowly driven price changes in the tails that are not representative of underlying price pressures. The hottest inflation in over three decades is being driven by widespread pressures.

Bolstering this last point is the fact that breadth remains very high with 75% of the CPI basket over 2% y/y.

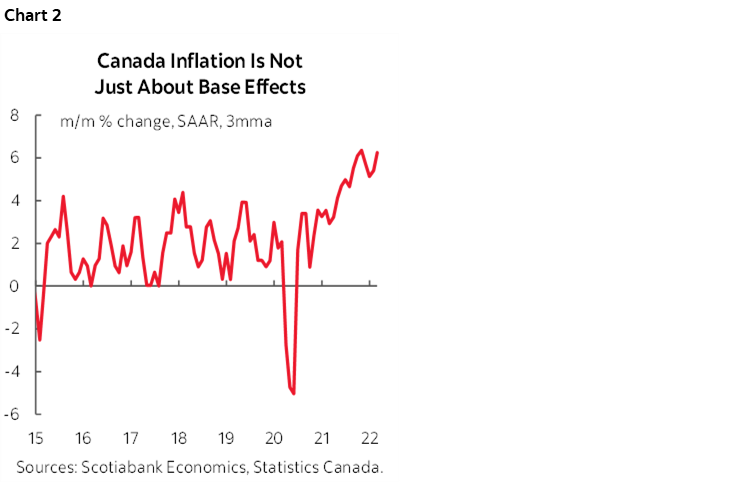

Further, in case we still have any inflation dinosaurs who still think that inflation is just being driven by year-ago base effects, well, it’s not. It hasn’t been for ages now. Month-over-month seasonally adjusted inflation at an annualized rate ran at 6.8% in February (chart 2). That says that inflationary pressures at the margin are still pointed above the year-over-year rate and still dragging it higher with no loss of momentum despite the fact that the BoC had long been promising we would see a loss of momentum by now or earlier. CPI ex-food-and-energy SA m/m inflation at an annualized rate was up 4.5%.

Seasonally adjusted m/m prices were up 0.6% non-annualized and therefore what is normally a seasonal up-month for Canadian prices—for reasons no one who has ever visited Canada at this time of year needs to have explained to them—was actually hotter than seasonally normal.

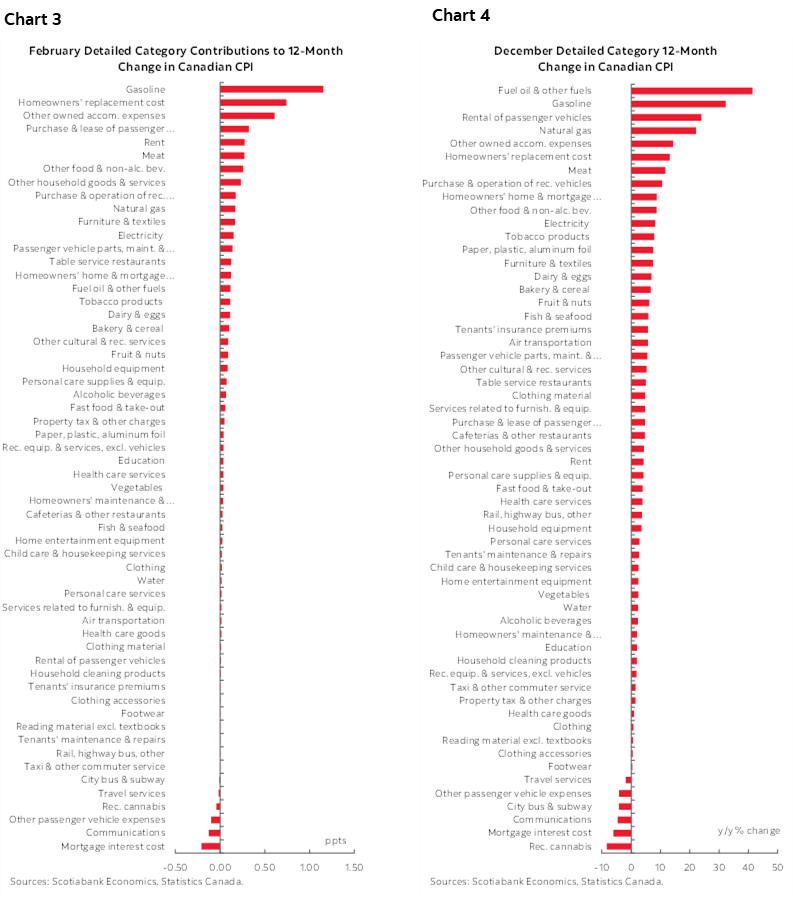

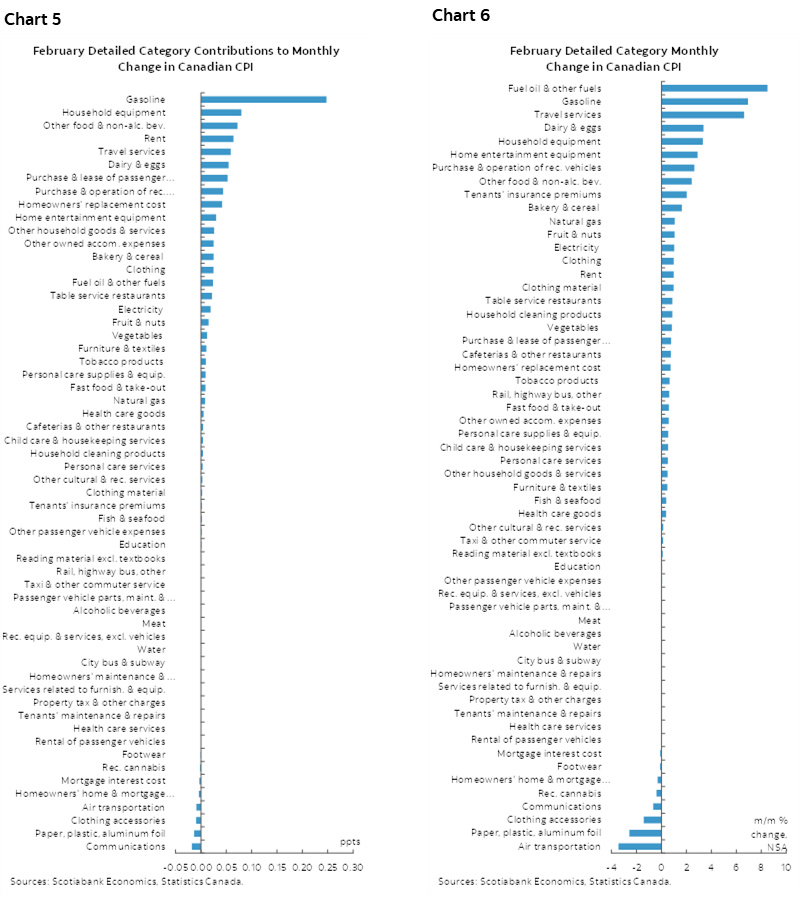

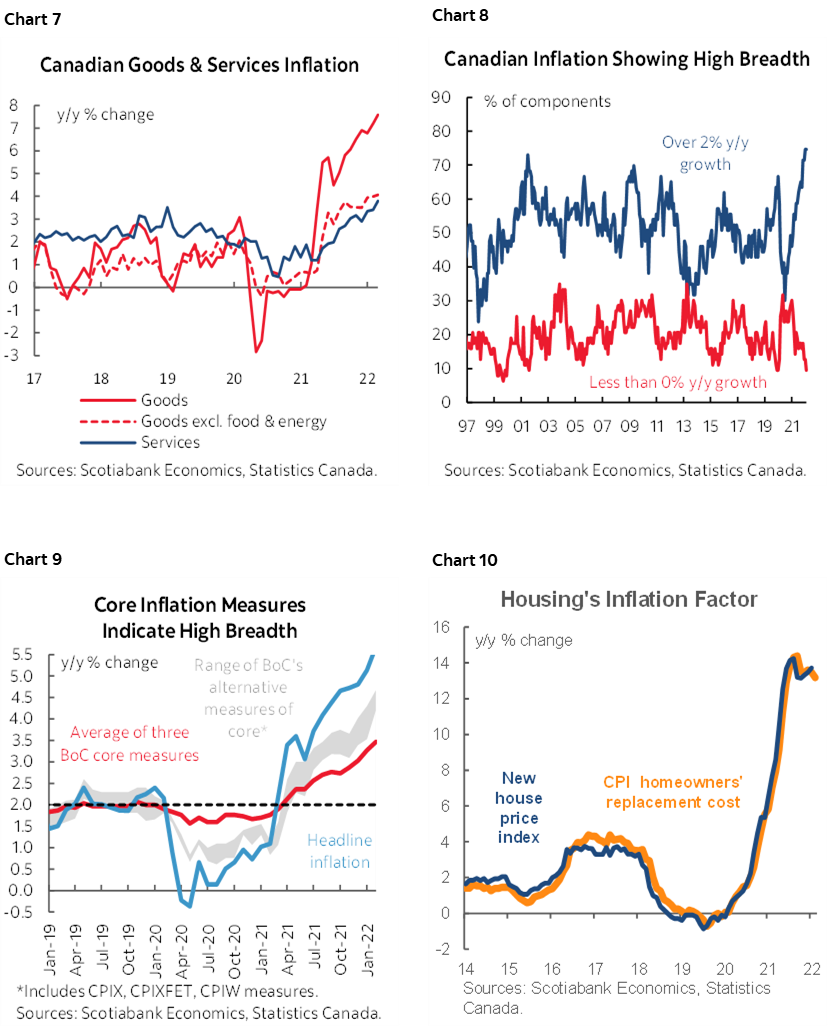

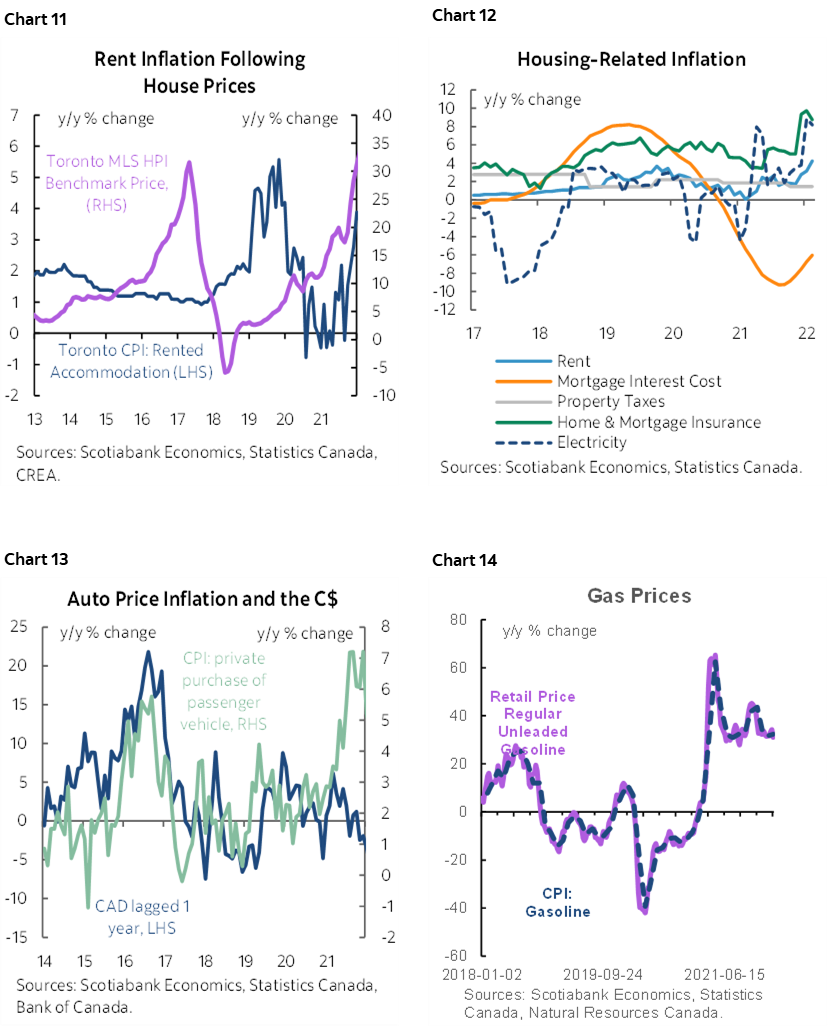

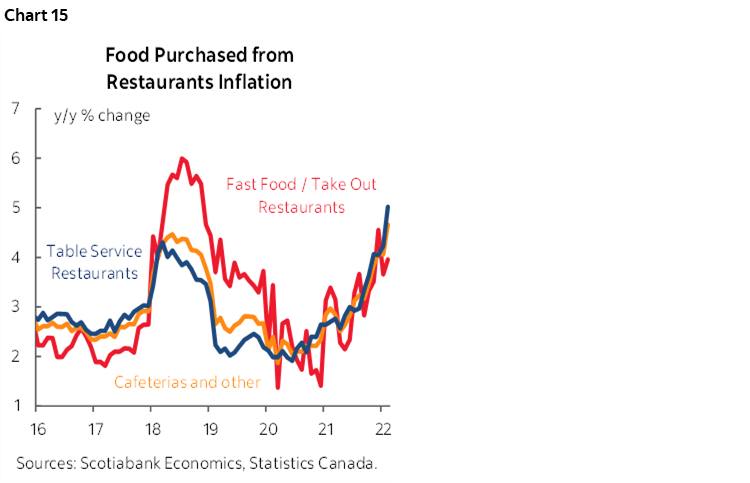

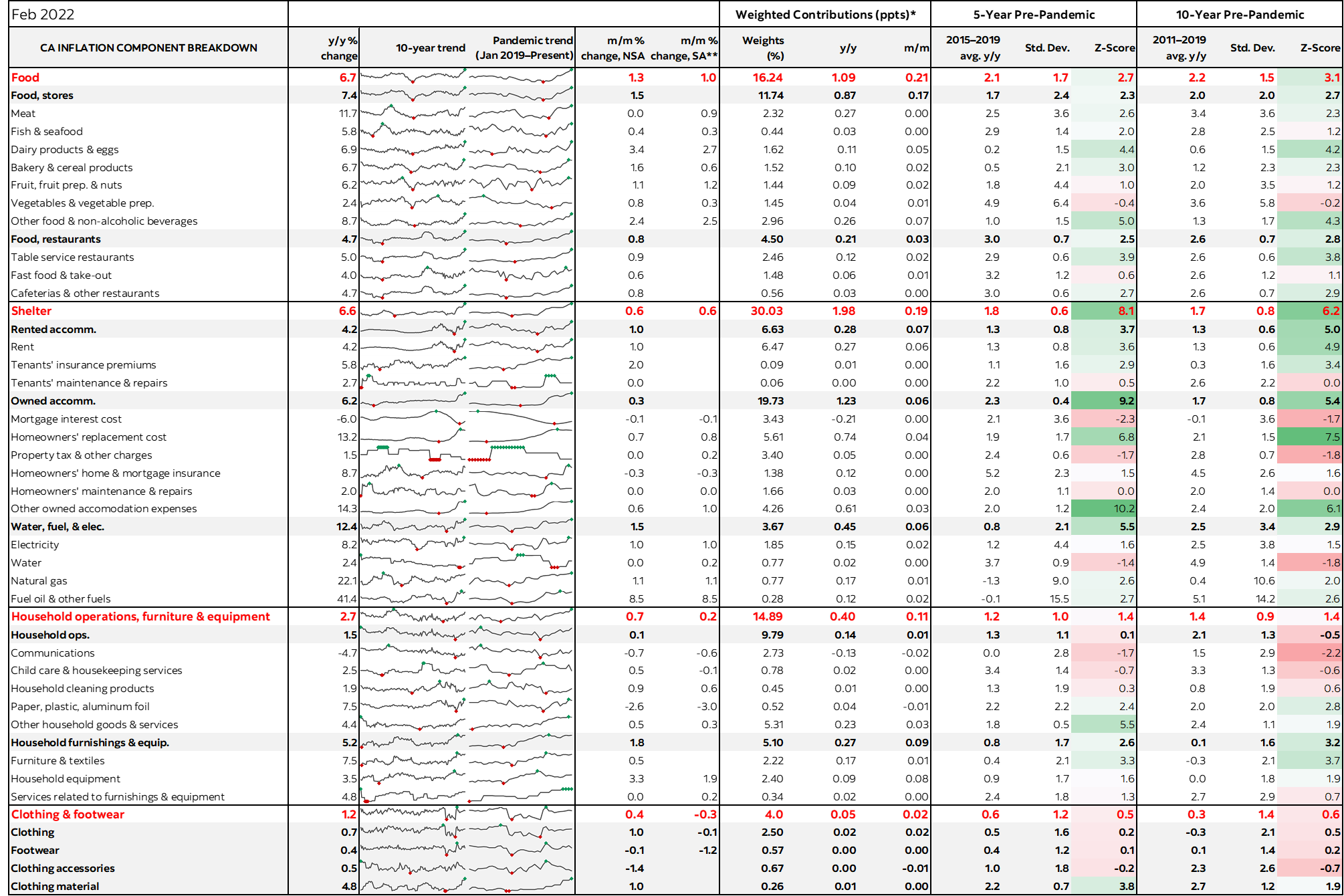

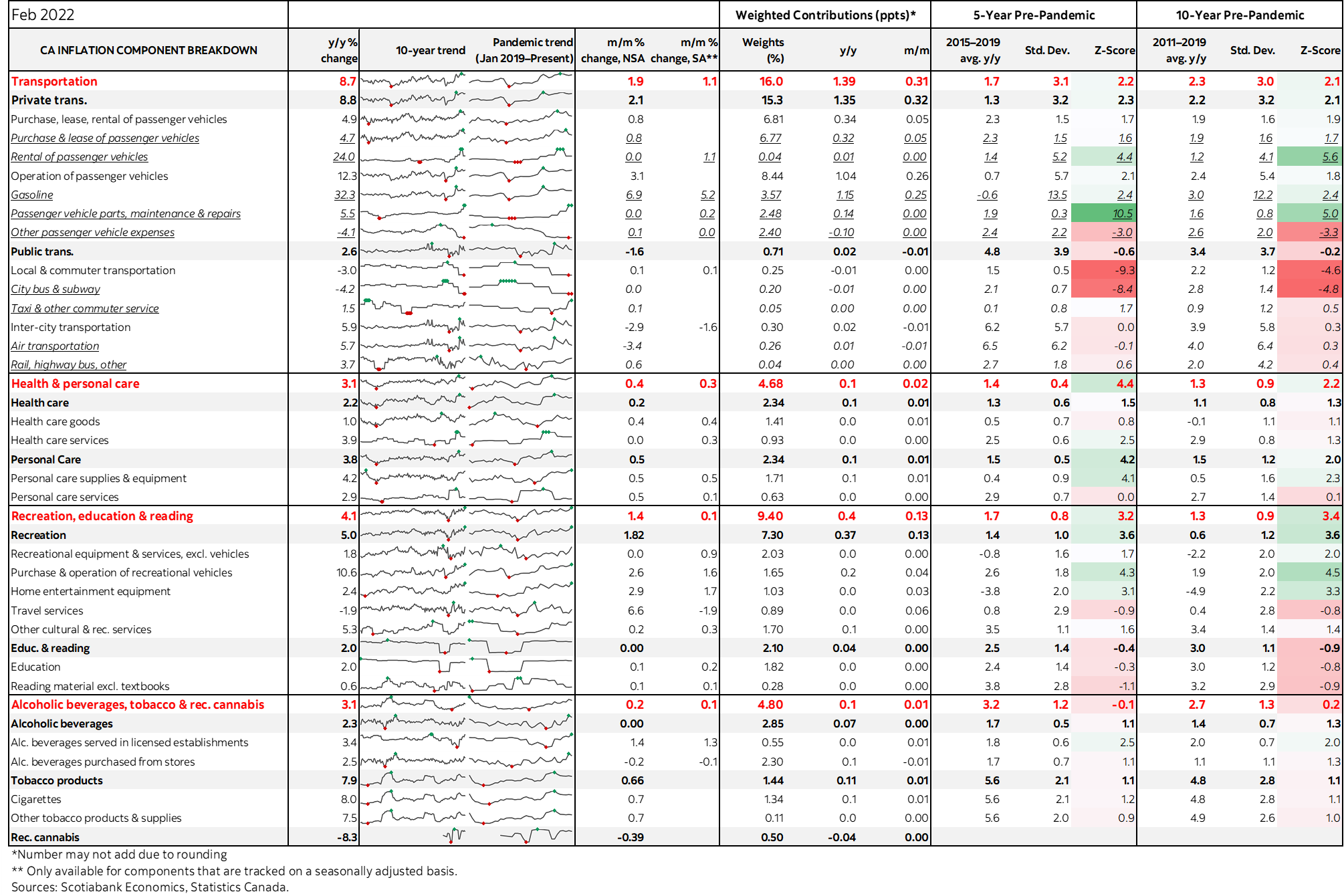

Charts 3–4 show the break down of the CPI basket in terms of year-over-year weighted contributions and unweighted changes. Charts 5–6 on the following page do the same thing for the monthly changes in prices. Yet again, the only way you wouldn’t see inflation here is if you don’t own a home, don’t rent, don’t drive and don’t buy any of what you eat. To avoid inflation in Canada, go build your own shack made out of locally sourced trees off in the boonies and I hope you are good at fishing and hunting. That sounds like a Farley Mowat character to me!

Charts 7–15 break down different items in CPI. A dominant theme is the role of housing that is becoming an accelerated source of inflation in Canada given the way it's measured. Shelter costs were up 6.6% y/y in February for the fastest increase since August 1983. Much of that is driven by homeowners' replacement cost that was up 13.2% y/y. Unlike the US that uses owners' equivalent rent, Canada captures housing primarily through the house-only part of builder prices (ex-land) as the main driver of replacement costs. That house-only component keeps pushing higher with a lag into CPI. Shelter will continue to add to inflation going forward.

BANK OF CANADA IMPLICATIONS

Recall that the BoC's January MPR forecast that Q1 inflation would be 5.1% y/y. Instead it is tracking 5.5–5.6% y/y. Never-ending serial upside surprises to BoC inflation forecasts won't sit well as the Bank of Canada’s inflation forecasters have been constantly playing catch-up.

What that says to me is that the BoC needs to expedite its tightening. As previously written, the BoC should not see shutting down its reinvestment program—which is likely to occur at the April meeting—as a substitute for hiking the policy rate in a rate equivalence sense. There is no rate equivalence as argued by their own staff’s research on the GBPP purchase program’s effects and based on the stylized facts that point to no meaningful change in Canada-US bond yield spreads during the period in which the BoC was gradually bringing net purchases down to zero while the Fed kept on buying Treasuries and MBS by the truckload. The BoC needs to show it is serious about inflation risk and adhering to its mandate with a larger move than just 25bps in April, like 50–75bps.

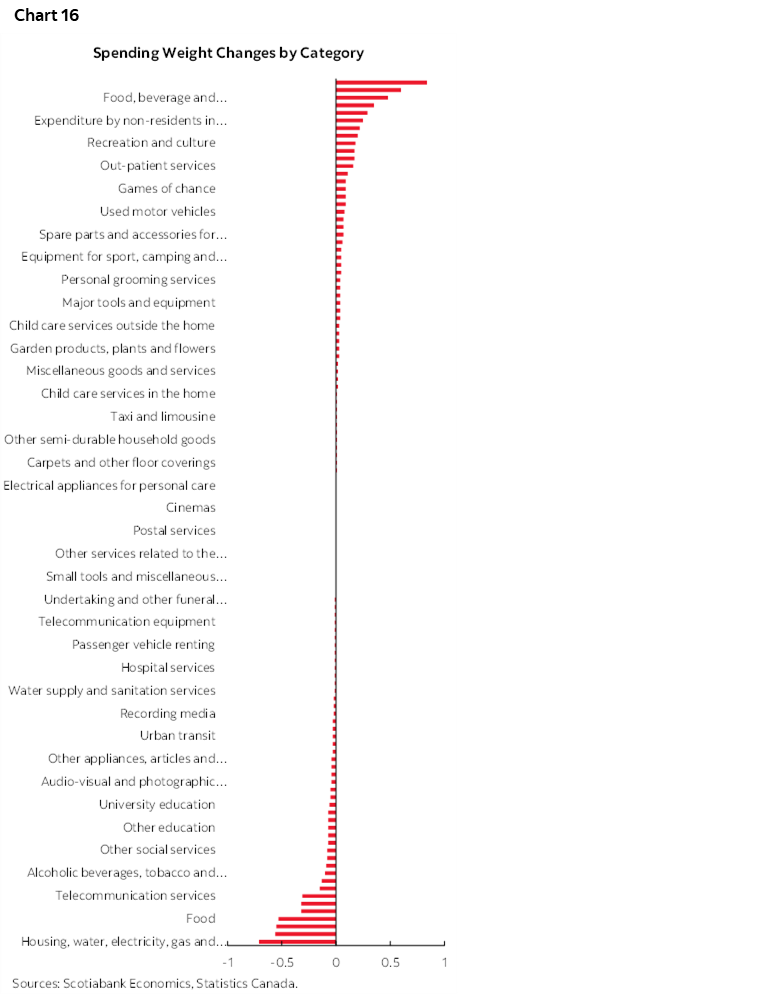

COMING CHANGES TO CPI WEIGHTS

StatsCan is advising that CPI basket weights will change again in June when May CPI estimates arrive. They will use household spending estimates from 2021 to refresh weights compared to the present use of 2020 weights. Chart 16 shows how the spending weights will change by category of spending. I roughly estimate that there should be a negligible impact on year-over-year CPI inflation when that happens relative to continued use of 2020 weights. That’s because the categories that will see higher weights in May CPI (clothing/footwear, furnishings/furniture, transport, rec/culture, food/accomm) will be offsetting lower weights on groceries, housing utilities, rent, comms, education. When these weight changes are applied to current price changes for those categories it results in no meaningful change in CPI inflation. StatsCan will be adjusting these weights annually going forward which will make CPI a little more reflective of current spending patterns as they evolve.

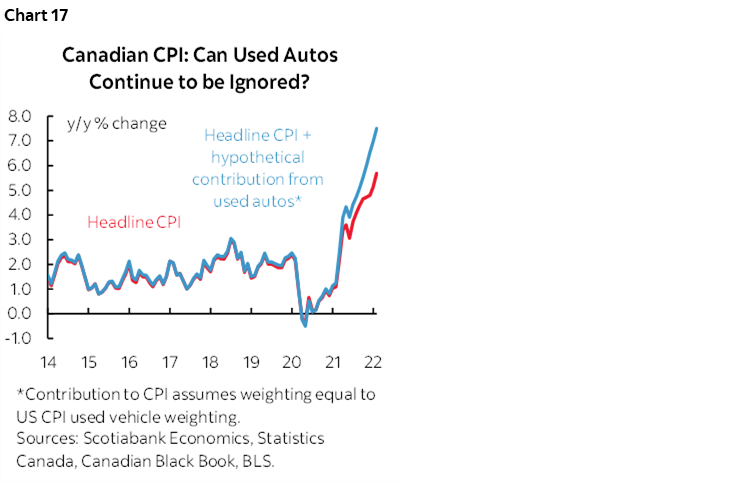

STILL WAITING FOR USED VEHICLES TO BE ADDED TO CPI

The bigger issue to coming changes to Canadian CPI stems from the fact that StatsCan is continuing to work on adding used vehicle prices to Canadian CPI compared to the useless practice of using new vehicle prices to proxy used vehicles that have been rising at much faster rates of increase than. They had advised as much in the February CPI report for January. It would make logical sense to do this at the same time as the basket weights get changed as noted in the prior section, but the logic of adjusting the basket in one fell swoop might not carry the day.

The existing practice drastically understates CPI inflation. Chart 17 shows a proxy estimate for how much but the agency has been silent on what approach it may take while guiding that they are finally working on a paper on the matter. In essence, whereas Canadian policymakers sometimes imply that Canada is better at managing CPI inflation than, say, the US by pointing to lower official Canadian CPI inflation relative to US CPI inflation, the reality is that this is just because of mismeasurement issues. If Canada measured CPI properly then it would have an almost identical rate of inflation and without even getting into issues like whether housing is being adequately captured in Canada’s methodology that relies upon builder prices.

All of which is to say that if we continue to get upward momentum as we forecast and if StatsCan adds used vehicle prices to the basket hopefully soon, then perhaps by summer Canadians will be fretting over an annual inflation rate crossing 8% y/y.

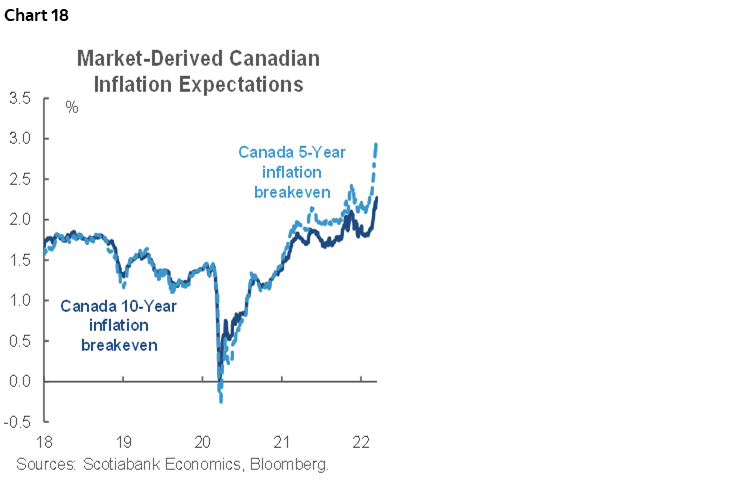

That would be inflation at a rate Canadians have not seen since 1982 into early 1983. We’re long past caring about exactly what’s driving inflation in what I think is a combination of supply– and demand-side drivers. The far more disconcerting development is that inflation expectations are becoming unmoored as shown in chart 18 and previously written in reference to other measures. We’re into the dangerous territory of adaptive and extrapolative expectations that have lost confidence that monetary policy can control inflation at this stage. The next round of consumers’ and businesses’ inflation expectations in the coming pre-MPR surveys will probably build upon those measures as well. The Bank of Canada’s credibility is very much on the line both in terms of the seriousness of addressing inflation and the stability issues associated with having overheated housing markets.

Please also see the back page table that provides more granularity on the inflation figures.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.