- The US economy continues to crank out jobs at a rapid pace

- Markets were not impressed...

- ..as they are mainly focused upon SVB’s failure...

- ...by relying more upon emotives than substance...

- ...and may be overreacting to wages and labour force expansion

- Fed watchers monitoring systemic risk as they move onto CPI

- Nonfarm payrolls, m/m 000s // UR (%), SA, December:

- Actual: 311 / 3.6

- Scotia: 240 / 3.4

- Consensus: 225 / 3.4

- Prior: 504 / 3.4 (revised from 517 / 3.4)

The US economy continues to crank out jobs at a fairly rapid pace. You wouldn’t be able to tell that from looking at markets today. The USD is softer but may now be regaining strength. US Treasuries are rallying with yields down by double digits across the whole curve (18–20bps across 2s through 10s in fact) which is spilling across into other global bond markets through carry. Equity indices are slightly lower in the US.

Markets reacted the way they did for three reasons.

- Trading in Silicon Valley Bank shares was halted shortly after US payrolls were released and we’ve since learned that the bank has failed. The share price was tumbling this morning as reports surfaced that the FDIC and Federal Reserve were examining the bank’s finances. Bonds, stocks and pricing for future Fed policy rate hikes are reacting more than measures of credit risk.

- US wage growth ebbed (see below).

- The US labour force continues to expand which indicates more workers can still be pulled into the job market and keep wage pressures somewhat at bay (see below).

US SYSTEMIC RISK REMAINS LOW

Unhelpful emotives are being flung around like cheap candy this morning. I think that’s getting ahead of things through headlines and reports written for the minute without necessarily thinking things through as we continue to monitor developments.

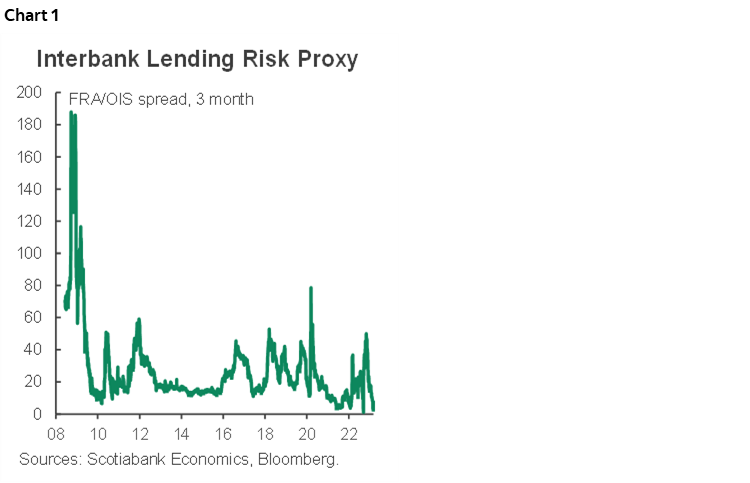

The spread between the three-month forward rate agreement and the comparable maturity overnight index swap rate has moved up a few basis points today but remains very low (chart 1). To this point there is low probability of material systemic risk in a contained situation although it plays to market sensitivities toward sudden developments.

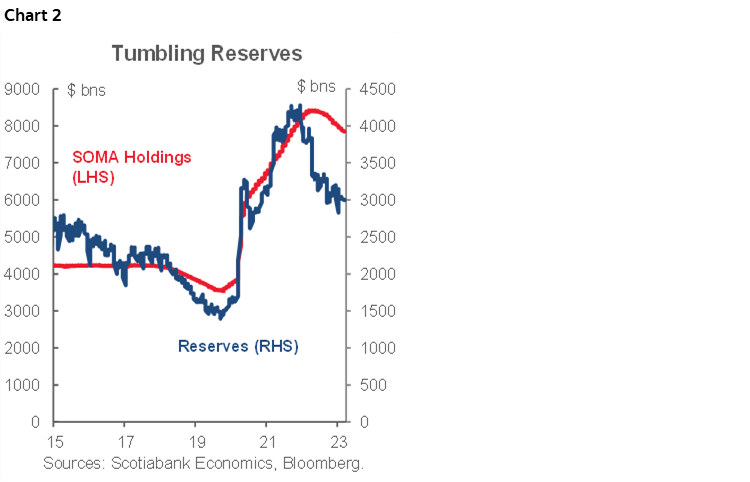

Further, reserves in the US banking system remain high at about US$3 trillion (chart 2). This probably still keeps them in the realm of ample reserves where Chair Powell wishes to keep them. I don’t think that the SOMA portfolio’s rollback has been large enough to date to spark material systemic risk to funding markets.

Still, there will be price discovery around the optimal level of reserves in the system and the funding frailties that are being exposed. If those frailties become larger, then the Fed has tools including greater repo market infrastructure and QT flexibility.

WAGE GROWTH EBBED

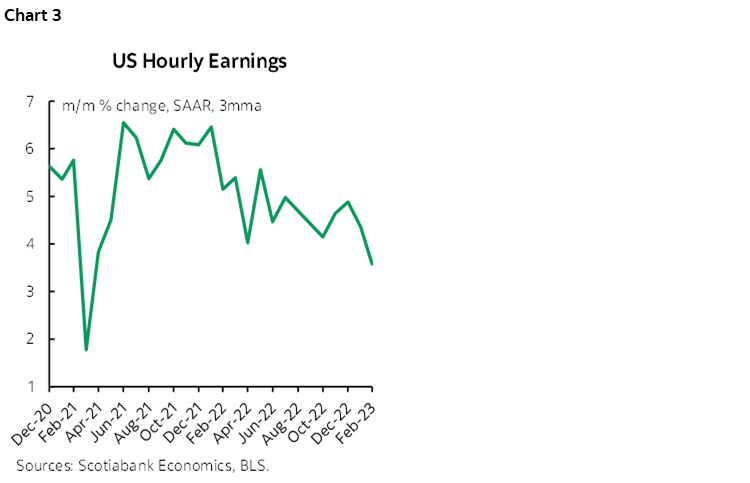

US wage growth ebbed to 0.2% m/m SA in February. That’s the slowest pace since February of last year and it was a tick beneath consensus expectations. The 3-month moving average of annualized wage gains is trending lower (chart 3).

One month shouldn’t cause such whippy reactions but it may have been a part of the market reaction this morning after a string of wage gains in the 0.3–0.5% range.

THE US LABOUR FORCE INCREASED

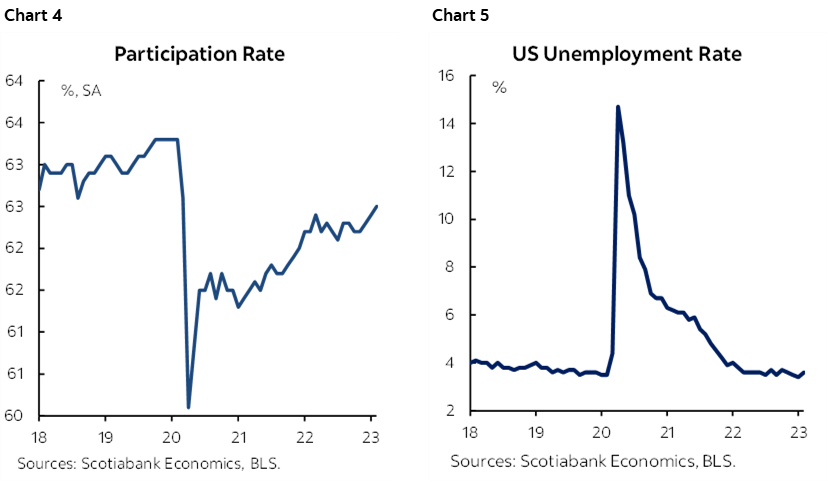

The US labour force increased by 419k in February. This is derived from the household survey that showed employment growth of just 177k. The net effect was to raise the participation rate (chart 4) and put mild upward pressure on the unemployment rate that climbed two-tenths to 3.6% (chart 5).

A big caution is that the 90% confidence interval around changes in US unemployment is +/-300k. There is even more noise within this household survey than in nonfarm payrolls. Markets never fuss over this and simply take the 419k gain in the labour force at face value when it could be a lot less or a lot more. The 90% confidence interval around estimates of the unemployment rate is +/-0.2% and so a 0.2% rise in the unemployment rate falls within the bands of noise. Again, markets don’t consider this.

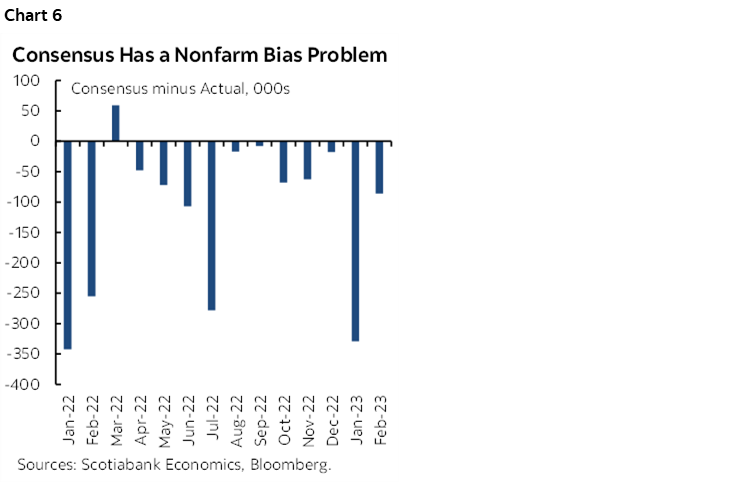

Nevertheless, this marks yet another in a long line of monthly job gains that consensus has wildly underestimated (chart 6).

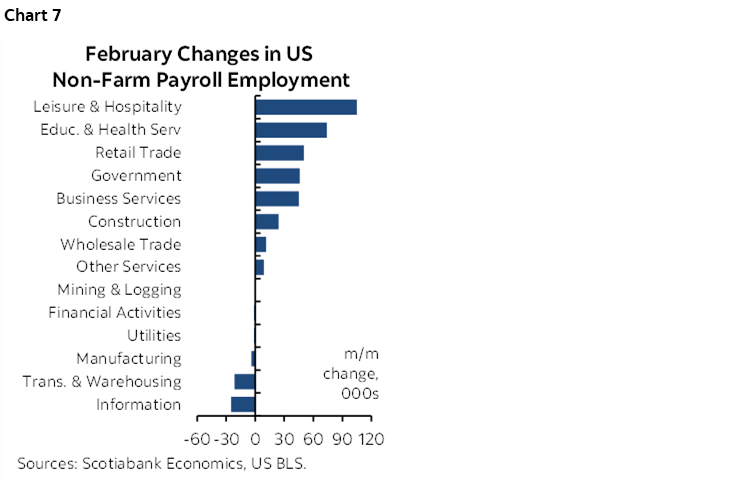

Chart 7 shows which sectors drove the gain in nonfarm payrolls.

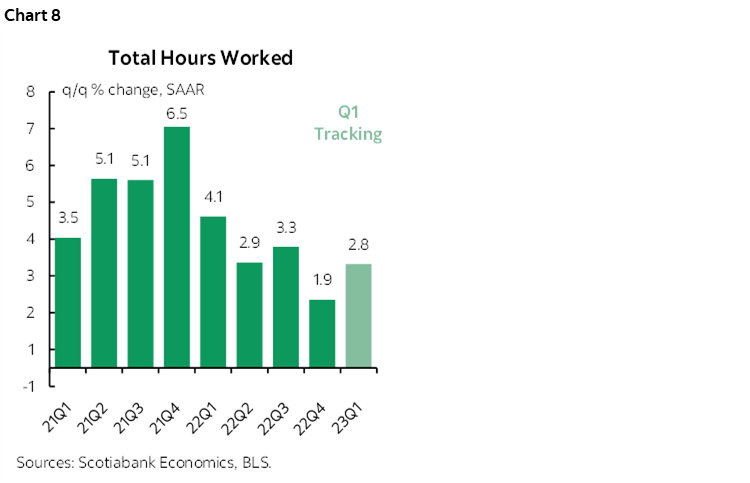

Also note that hours worked are tracking a nearly 3% rise in Q1 (chart 8). This is a positive sign for Q1 GDP growth since GDP is hours worked times labour productivity.

Next up for Fed watchers are further market developments and US CPI on Tuesday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.