- With jobs and wages pending, the BoC has a case to hike in July

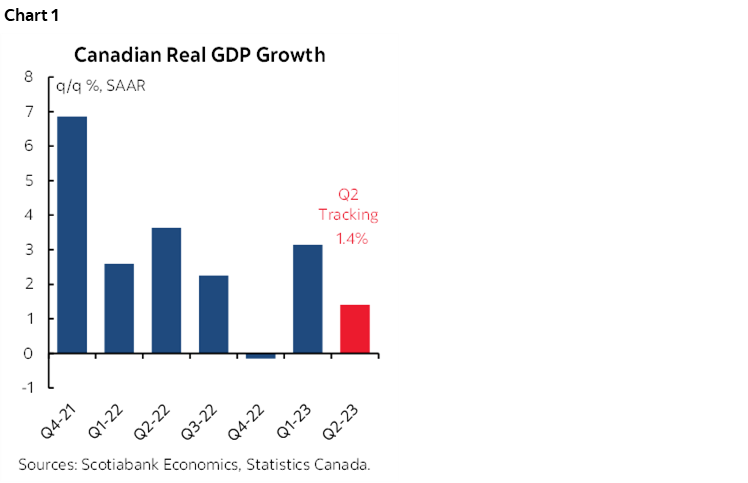

- The economy is tracking 1½% GDP growth in Q2...

- ...which may be slightly exceeding BoC forecasts even with distortions...

- ...on a mish mash of monthly revisions, misses and beats

- BoC surveys continue to indicate unmoored inflation expectations...

- ...and rising house price expectations

- US data spilled over into Canadian market effects

- Canadian GDP m/m % change, April:

- Actual: 0.0

- Scotia: 0.3

- Consensus: 0.2

- Prior: 0.1 revised up from 0.0

- May GDP ‘flash’ estimate: 0.4%

BANK OF CANADA IMPLICATIONS

A suite of readings indicates that GDP growth is modestly exceeding the Bank of Canada’s Q2 forecast while its surveys of businesses and consumers point to unmoored inflation expectations and rising expectations for gains in house prices in a case of here-we-go-again. On net, these developments bolster—not cement—the case for a BoC hike on July 12th and probably carry the day over the recent CPI figures. An economy that is not yet making strides toward opening up disinflationary slack approaching two years after bond market tightening began and with no one believing they’ll hit their 2% inflation target requires another disciplinary jolt of monetary tightening in a race against the clock to contain inflation risk. The narrative for how inflation risk has pivoted higher remains intact. The last piece of information may be next Friday’s jobs and wages that I think will set a constructive tone.

The case against a hike in July is nevertheless not to be fully discounted even if not a base case by a slim margin. The BoC has skipped making rate changes along trend tightening or easing paths in past fine-tuning stages as it assesses a sweep of data and the recently softer than expected inflation print could provide some cover to take the summer to evaluate and come back recharged in September. Some, like me, might be left wondering what was the point if the only incremental tightening turns out to be a quarter-point and question the BoC’s resolve to crush inflation risk in slow footed fashion.

GDP DETAILS

March GDP was revised up a tick from flat to a 0.1% gain. April GDP landed flat compared to initial flash guidance that the economy grew by 0.2% with some of that miss explained by the upward revision to the prior month which was the only month that got revised. The truly new information came through May GDP with the initial estimate pointing toward a strong 0.4% m/m gain, until that possibly gets revised either up or down.

This combination of a positive revision, a miss, and then a strong flash reading combined to net out to tracking growth that is still in the 1 ½% q/q annualized range for Q2 using the monthly GDP accounts (chart 1).

There are three reasons not to get too fussed by a slowdown in growth:

- Growth in Q2 may be slightly exceeding the BoC’s forecast for 1% q/q SAAR growth. Whether using the monthly production-side GDP accounts or our ‘nowcast’ for quarterly GDP growth using expenditure accounts, we think that growth is tracking around a half percentage point faster than the BoC anticipated. That’s not a big deal, but it means that instead of mildly lower than potential GDP growth we have growth roughly matching potential GDP growth and hence the economy is still not opening up disinflationary slack.

- A significant caveat around the data is the uncertain net effect of transitory shocks such as ongoing wildfires that have disrupted some activity relative to what might have occurred while boosting spending to fight the fires. It’s also unclear whether the full indirect effects of the Federal civil service strike were shaken off even in the May GDP estimate.

- Some growth may have been pulled forward into Q1 from Q2 and so we need to look at the combination through the whole first half. Some growth in Q2 may be punted into Q3.

- After the economy expanded by 3.1% in Q1 and then shifted to rising at around the supply side’s ability to expand, the economy is still not making material traction toward opening up disinflationary slack.

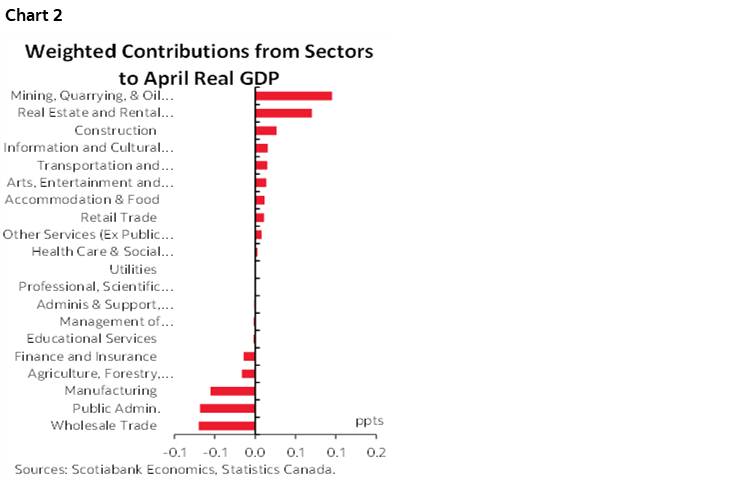

- Chart 2 shows the weighted contributions to April’s flat GDP print by sector. Bright spots were in resources, real estate services and construction, and travel/tourism activities. Downsides came through wholesale trade, manufacturing and public administration.

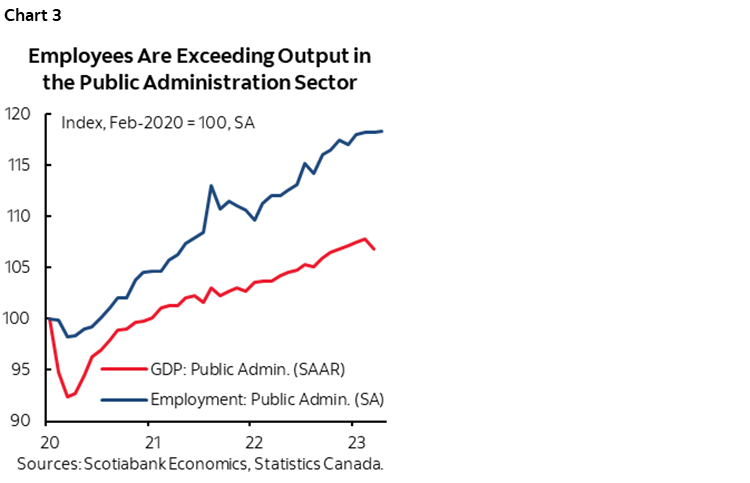

April was stronger than it appeared and May was weaker than it appeared because of the direct effects of the Federal civil servants’ strike. The federal civil servants’ strike shaved about 0.1% m/m off of April GDP in terms of direct effects and while we only have verbal guidance for May’s rebound in public administration, it’s likely that a similar weighted positive contribution to May GDP took place. What we cannot tell is the multiplier effect of the strike on other sectors such as agriculture but a ballpark guesstimate could reasonably mean another 0.1% or so of growth was robbed in April through the strike’s indirect effects. As an aside, the public administration sector offers a case of many more employed bodies producing less person employed (chart 3).

We don’t get numbers behind the flash estimate for May GDP and instead get this loose verbal guidance from Statcan:

"Advance information indicates that real GDP increased 0.4% in May. Growth was led by the manufacturing and wholesale trade sectors, as well as by offices of real estate agents and brokers. There was also a rebound in federal government public administration (except defence). These increases were partially offset by decreases in the mining, quarrying, and oil and gas extraction sector, as well as the utilities sector."

BANK OF CANADA SURVEYS — UNMOORED EXPECTATIONS

The release of the Bank of Canada’s twin consumer (here and here) and business surveys (here and here) is likely going to concern the central bank. Signs of progress toward lower inflation included fewer reported labour shortages that are still high, and weaker expected growth that is likely necessary to achieve lower inflation.

What dominates, however, is ongoing evidence that inflation is expected to remain well above the BoC’s target for an extended period of time. Unmoored expectations are a challenge to the BoC’s 2% target because when higher inflation becomes expected in demands and contracts it can become a self-fulfilling prophecy that is difficult to control.

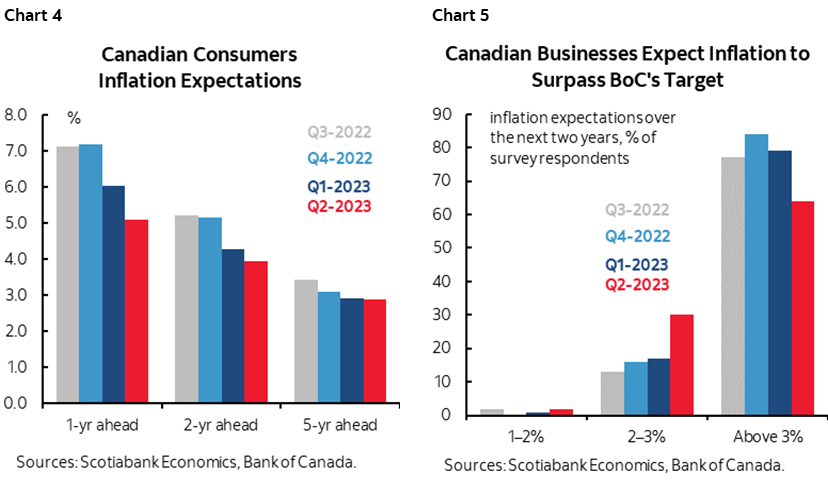

There were some improvements such as in consumers’ 1-year and 2-year ahead inflation expectations but they are still high, and consumers still expect above 2% inflation 5-years out from now (chart 4). Businesses’ inflation expectations shifted a little from the above-3% to the 2-3% category, but basically businesses think inflation will be above the 2% target throughout the 2023-24 period (chart 5).

What may also concern the BoC is evidence that households are raising their house price growth expectations as shown in their chart 2 in the second link provided for the consumer survey.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.