- The disturbing serial pattern of underestimating job growth continued...

- ...and now tallies ~2 million missed jobs in 17 months

- Bears pointing to the rise in the UR have it all wrong

- The case for a June hike remains solid through careful interpretation of Fed-speak

- US nonfarm employment m/m 000s / UR %), wage growth m/m %, May, SA:

- Actual: 339 / 3.7 / 0.3

- Consensus: 195 / 3.5 / 0.3

- Scotia: 225 / 3.5 / 0.3

- Prior: 294 / 3.4 / 0.4 (revised from 253 /3.4 / 0.5)

- Two-month revisions: +93k

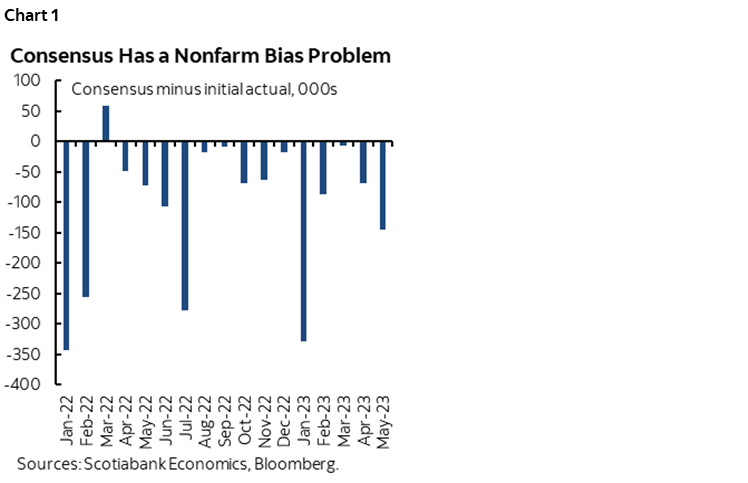

US job growth strongly beat consensus yet again (see table). As chart 1 shows, the pattern of serially underestimating job growth is rather unflattering to the community of economists and market participants that keeps wishing for weak reports but keeps getting routinely beaten on estimates of job growth. Consensus has underestimated payrolls in all but one month since the start of last year. The sum total of this underestimation bias amounts to missing about 1.9 million of the jobs that have been created over this time and so we’re dealing with a sizeable bias. That’s comparing consensus estimates to initial nonfarm payrolls estimates on release day. If instead we compare consensus estimates to current estimates of past job growth including revisions then the sum total forecast error has underestimated job growth by 1.6 million over this same period.

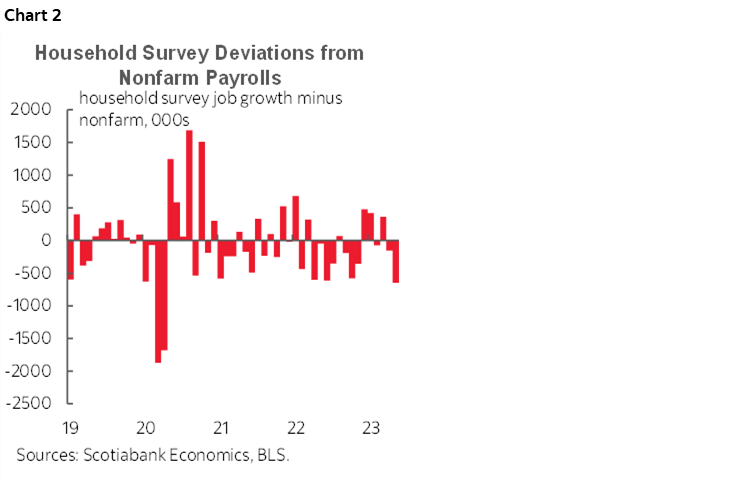

As a further sign of this bias, some of the commentary is playing on the fact that the unemployment rate edged up three-tenths to 3.7% in May and therefore somehow that’s what the Fed will focus upon. This is pure rubbish. The unemployment rate is derived from the companion household survey that showed a decline of 310k jobs and a 130k rise in the size of the labour force. Those numbers are pure statistical noise. Don’t take my word for it? Well then, listen to the Bureau of Labour Statistics (here) since they estimate that the 90% confidence interval for the household survey’s reported change in jobs is +/-600k versus +/-130k for nonfarm. Therefore we cannot conclude at this implied level of significance that the 310k drop in the household survey’s estimate of job growth is anything but pure noise whereas the 339k rise in nonfarm payrolls meets the bar for defining it as a statistically significant jump.

Chart 2 is another way of demonstrating this point. It shows that deviations like the 649k spread between this month’s nonfarm and household survey job growth estimates are not at all uncommon in both directions. Recall that earlier in the year the spread was in the opposite direction. The household survey beat nonfarm payrolls by +478k in December, 422k in January, and 360k in March and yet the bears were silent then. Imagine that, data not conforming to the narrative.... I'm sure some folks will spin the household survey in May as a darker signal than the payrolls report but there's simply no credibility to doing so.

In all, these are major reasons why the Fed pays much more attention to nonfarm payrolls rather than the household survey’s job growth estimates.

Across other details, revisions added 93k more jobs to the prior two months than previously estimated.

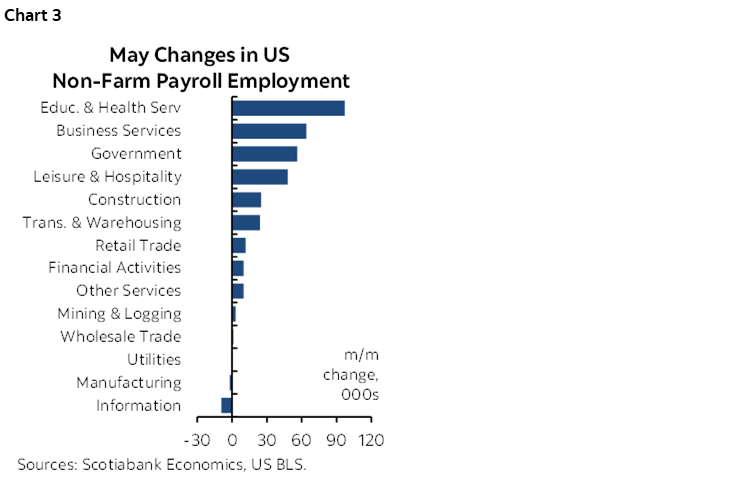

Private payrolls were up by 283k with government jobs up by 56k almost entirely at the state and local levels of government.

Goods producing sectors added 26k while services were up 257k in a continuation of the pattern that’s reflective of the modern day economy. There was decent breadth within services. Leisure/hospitality was up 48k, health care and social assistance added 75k, transportation/warehousing hired 24k folks, professional services were up 64k and not due to the temp employment category. Chart 3 provides the breakdown.

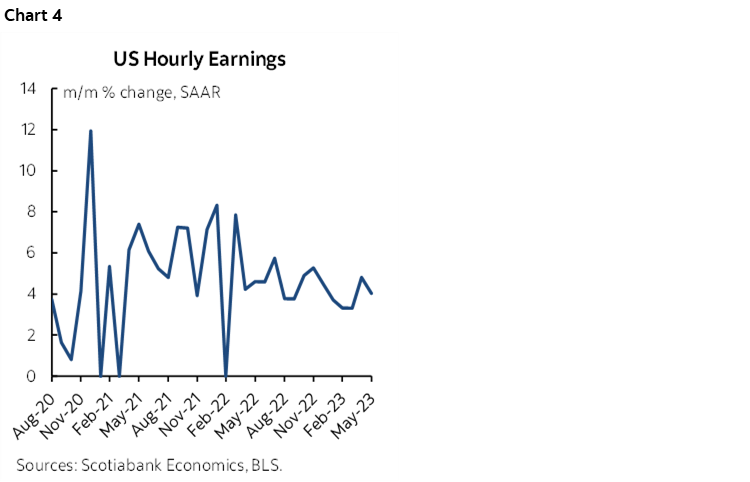

Wages were up by 0.3% m/m SA for a 4% m/m SAAR gain which is softer than the 4.8% distorted surge in the prior month but up from 3.3% before that. The three-month moving average for this measure is 4.1%. Chart 4.

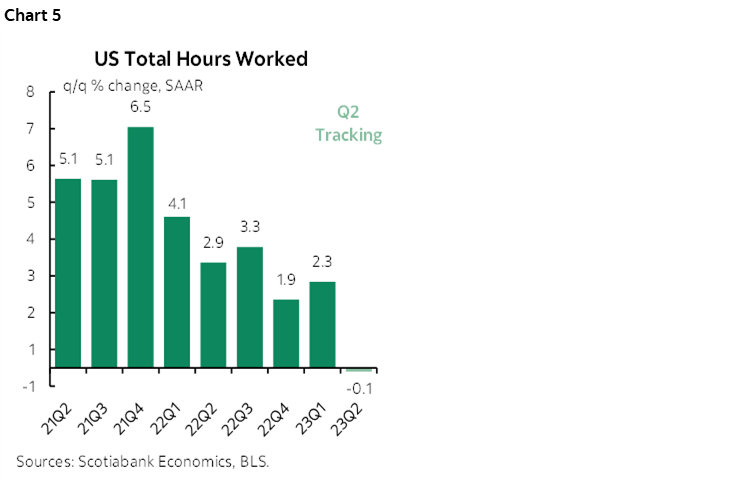

US hours worked are not a plus for Q2 GDP. After a 2.3% q/q SAAR gain in Q1, hours are tracking flat (-0.1% q/q SAAR) in Q2 (chart 5). Unless there is a strong productivity rebound from Q1 (and there may well be one) then Q2 GDP faces downside risk.

INTERPRETING FED-SPEAK

I think today’s set of numbers keeps open the door for additional Fed tightening. The camp that wants to believe that Fed rate hikes are over and done with is distorting impressions about what is contained in recent Fed-speak and in a way that may be destabilizing to markets. The only voting FOMC official that I’ve heard clearly spell out support for a June pause has been Philly’s Harker, and even he sounds a tad data dependent. What follows is a review of recent Fed-speak.

For starters, did Chair Powell’s comments on May 19th really set up a pause as some are suggesting? Recall that he said “Having come this far, we can afford to look at the data and the evolving outlook to make careful assessments.” When Powell said he’s going to “look at the data” I heard that he’s going to, well, “look at the data” and then decide what to do on a meeting-by-meeting basis rather than having hard set guidance in advance of future decisions. That’s not necessarily a pause signal. Recall that Powell also said in that same event that they haven’t made any decisions about future moves and emphasized they will follow the data at the margin from here forward. Powell’s point is that since they are in restrictive territory now and facing lagging effects of their decisions they can afford to step back from explicit hike guidance and take the decisions one at a time depending upon the evolution of data and events like the debt ceiling agreement’s passage.

Jefferson’s comments the other day are also being exaggerated by markets and are not necessarily representative of the full range of opinions as noted below in a recap of positions taken by FOMC officials who vote this year. On balance, I think it will come down to the debt ceiling vote’s passage, a strong nonfarm report and the next CPI on day 1 of the FOMC meeting.

- Governor Waller: depends on data.

- Governor Jefferson: He said “A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle.” Emphasize “at a coming meeting” and not necessarily June. That’s much more ambiguous on timing a potential pause than the coverage I’ve seen that read what some folks wanted to read as a clear June signal which it was not.

- Governor Bowman: Pointed to rebounding house prices as a challenge to their inflation goals. No comment on next decisions.

- Governor Barr: No recent comments.

- Governor Cook: No recent comments.

- Philly’s Harker: “I am definitely in the camp of thinking about skipping any increase at this meeting, barring what we see in the next few days.”

- Dallas’s Logan: Data dependent. “The data in coming weeks could yet show that it is appropriate to skip a meeting. As of today, though, we aren’t there yet.”

- Chicago’s Goolsbee: Said he doesn’t wish to pre-judge June decision and hasn’t made a decision.

- Minneapolis Prez Kashkari: “We may have to go higher from here, but we may not raise rates quite as aggressively and as quickly as we have over the course of the past year.” Ambiguous on timing and amounts if any. May pause, may not, rates may have to go higher.

As an add-on point, I don’t like the view that is creeping into markets that the Fed can halt and start and halt and start rate hikes in jerky fashion. First, I don’t have much trust for such guidance from a minority of Fed officials since it may just be about trying to manage markets by halting but holding out the threat of hikes they have no intention of delivering. Second, such an erratic path could damage market confidence and confidence in the economy through its effects upon the ability to plan. Third, I still think there is more merit to front-loading as long as the data supports it rather than a fits and starts path forward. If you’re going to pause, then signal a lengthy one as opposed to this nonsense of how well, maybe we don’t go in June, but July could be a live meeting. That’s just muddled thinking imo.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.