- Inflation exceeds consensus expectations…

- ...lighting up yields and the dollar while hitting equities

- Momentum and breadth of price pressures remain very high

- 1% Fed funds is grossly misaligned toward 8.6% inflation…

- ...which probably leans more toward a faster pace and bigger moves from July onward…

- ...as Fed guidance may have tied their hands into next week’s meeting

- The case for 75+ from the BoC is July has also gone up

US CPI, m/m SA // y/y % change, May:

Actual: 1.0 / 8.6

Scotia: 0.9 / 8.5

Consensus: 0.7 / 8.3

Prior: 0.3 / 8.3

US core CPI, m/m SA // y/y % change, May:

Actual: 0.6 / 6.0

Scotia: 0.5 / 6.0

Consensus: 0.5 / 5.9

Prior: 0.6 / 6.2

The latest inflation reading lit up the bond market and with it the odds that the Fed accelerates the pace and size of rate hikes. A higher than consensus print drove the 2-year Treasury yield about 18 bps higher and the 10-year yield about 9bps higher in a bear flattener move. The dollar took flight and the S&P is down almost 3% on the day so far.

Fed funds futures are pricing a few basis points more than a half-point rate hike next week and material odds of a 75bps at the July meeting. The Fed has made it clear it will be considering a 50bps move next week and so given its emphasis upon avoiding surprises and holding hands along the way it may be highly reticent to deviate from this guidance. The costs to turning its meeting-by-meeting forward guidance into a dumpster fire may be deemed to be too high and they can use forward guidance to support market tightening that is greater than the immediate pace at which the target range is hiked. There may, however, a hawkish dissenter or more.

Instead, the committee could be kept onside with more hawkish plans after the June meeting. The bigger key may be signals toward a bigger move in July that could include a specific press conference reference next Wednesday to a 75+ move at the next meeting. Forecasts are submitted today ahead of the Tuesday–Wednesday FOMC meeting and individual participants can change their forecasts up to Tuesday night which means they will take into account today’s inflation reading. I think there are very high odds of a 75bps move in July, higher odds they will signal a continuation of big moves into the September meeting and that our forecast for a terminal rate of 3% faces significant upside risk into year-end.

Headline CPI prices were up 1.0% m/m in seasonally adjusted terms which is quite a bit faster than consensus (0.7%) and close to my 0.9% estimate at the very top end of consensus. Core inflation ex-food-and-energy was up 0.6% m/m and a touch faster than consensus and my estimate that were both 0.5%, but the year-over-year rate of 6% was a tick higher than consensus and on my estimate.

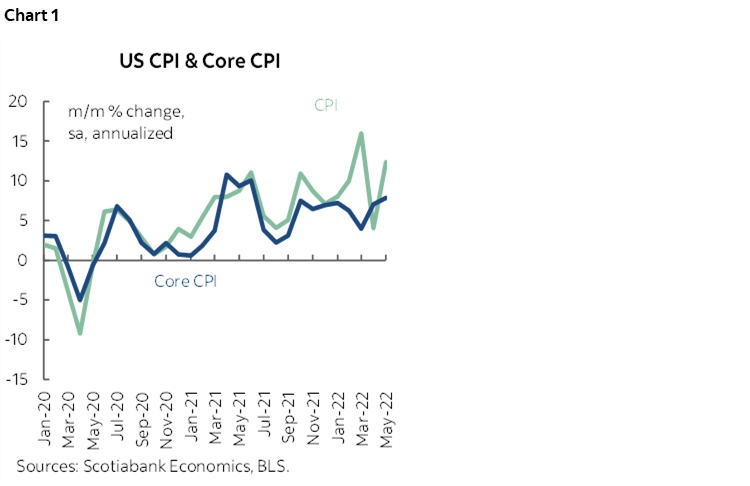

Momentum remains very high with no signs that inflationary pressures are easing up which counsels hitting the policy rate harder. Annualized month-over-month core CPI inflation picked up to 7.8% from 7.0% the prior month for the hottest reading since June of last year. Chart 1 shows how sustained the price pressures have been using this measure which remains the preferred gauge for assessing inflationary pressures at the margin as opposed to year-over-year measures.

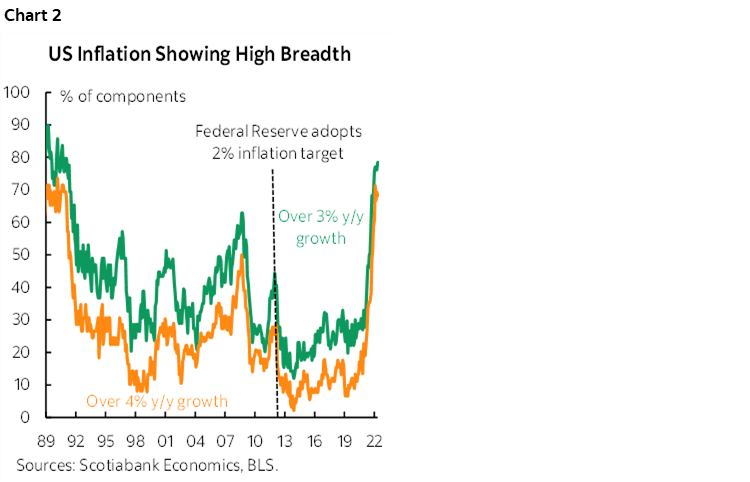

High breadth was the added killer (chart 2). Very high breadth. 86% of the CPI basket is up by more than the Fed’s 2% inflation target. 78% of the basket is up by more than 3% and 68% is up by more than 4% or double the Fed’s target. It takes until we get to about 5.7% y/y for over half of the basket to be rising by less than this figure. All told, this is astronomical breadth.

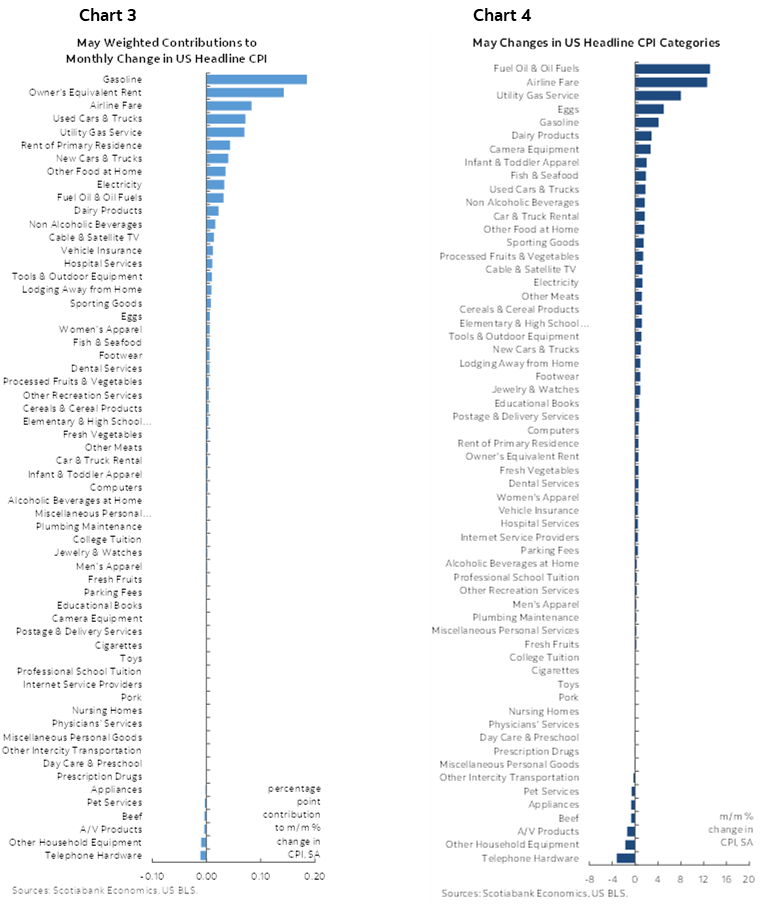

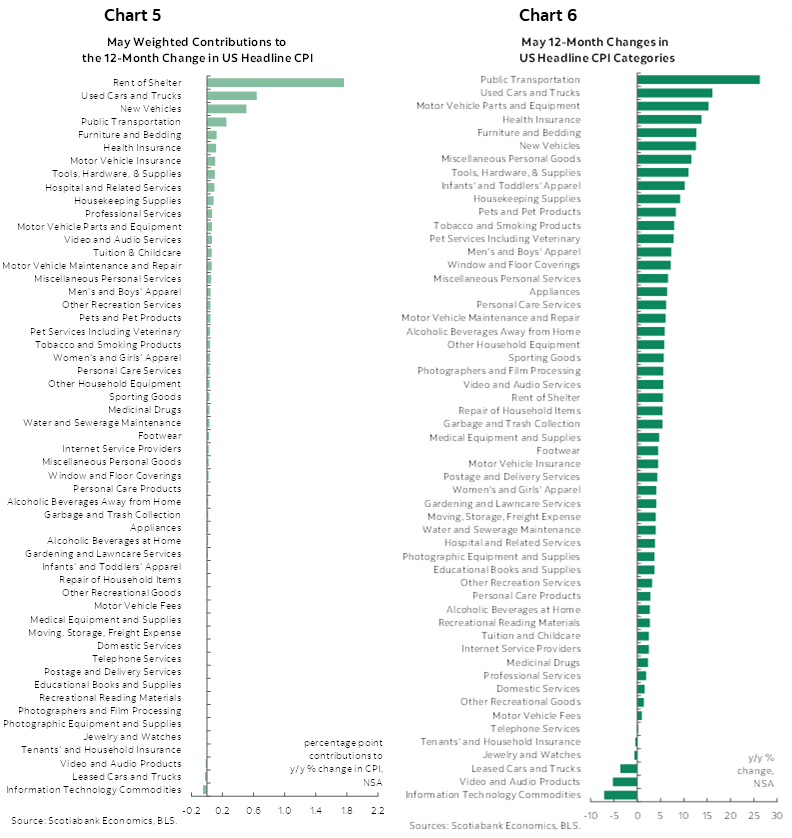

Chart 3 shows the weighted contributions to the 1% m/m rise in total CPI by individual component. Gasoline prices were the highest contributor followed by the way the US captures housing inflation and then followed by airfare, used vehicles, home heating, rents, new vehicles and onward. These are major components of the household budget and they are all lit up. Chart 4 shows the changes in m/m prices by category without applying weights to the respective categories. Charts 5 and 6 do the same thing to the year-over-year rates by category.

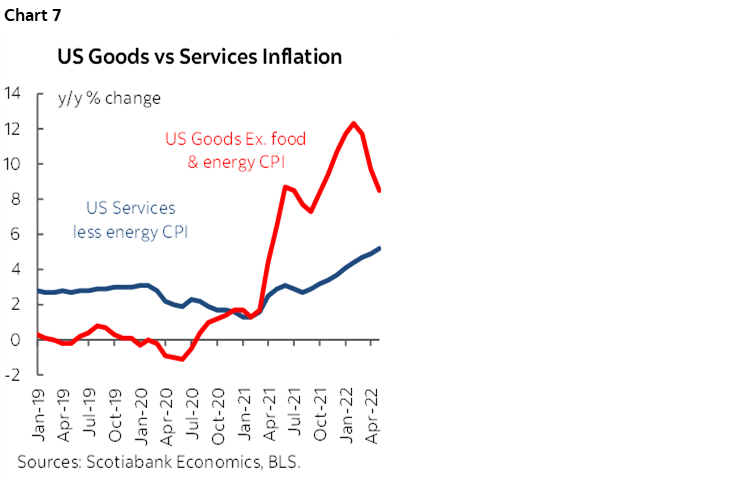

Core goods price inflation is ebbing in year-over-year terms but the warnings about the need to discount this as pandemic effects dissipate in favour of expecting accelerating reopening effects on services are coming true (chart 7). Service price inflation continues to accelerate.

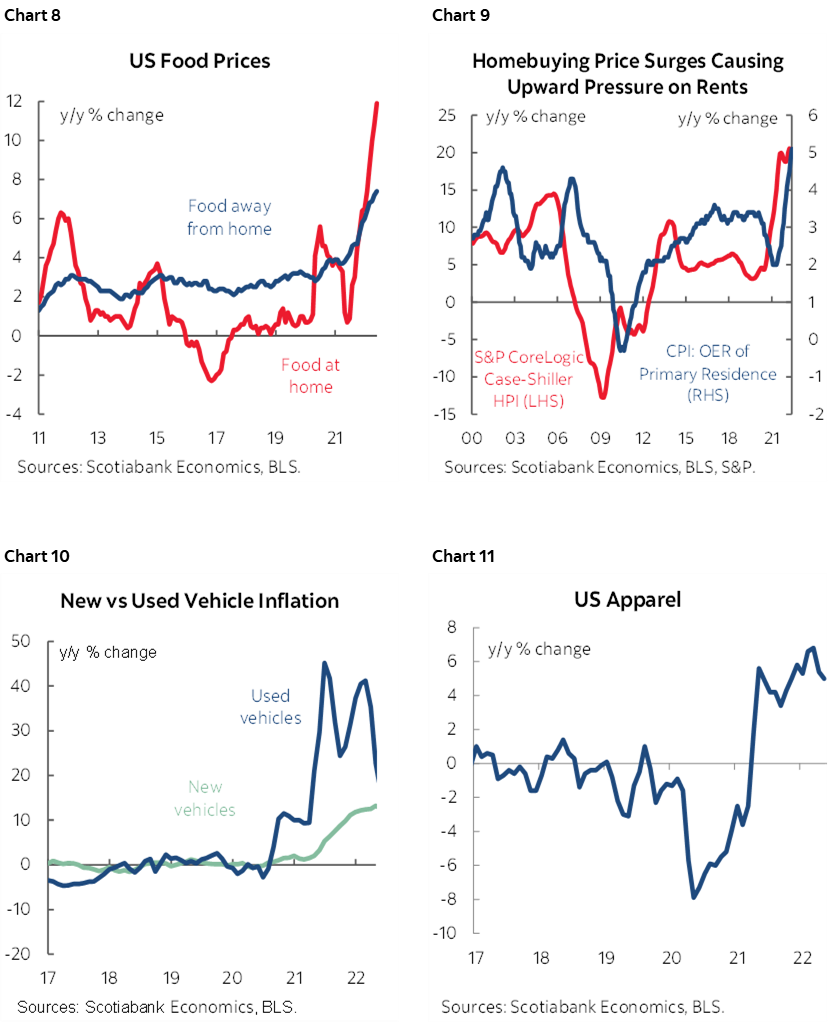

Food prices were up 1.2% m/m with food at home up 1.4% and away from home up 0.7% (chart 8). Energy prices were up 3.9% m/m led by gas at 4.1% that matched the estimate, but also piped gas prices were up 8% which was softer than market price increases. Housing inflation is shown in chart 9. I'm surprised that both new and used vehicle prices were up 1% m/m and 1.8% m/m respectively given other sources that were indicating they'd be little changed and cancel out, but the year-over-year rates have cooled (chart 10). Still, the weights imply little contribution from either.

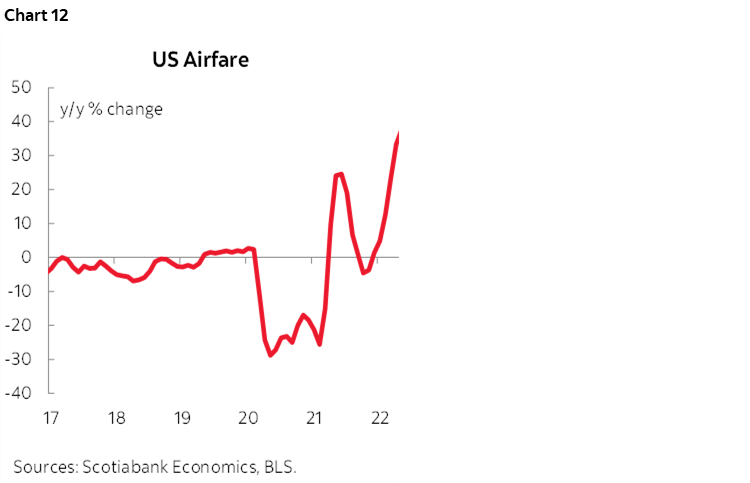

High contact prices gained again as expected. Airfare was up 12.6% m/m, vehicle rentals up 1.7% m/m since if you can't get one then rent one, lodging was up 0.9% and note previously mentioned take-out prices etc etc

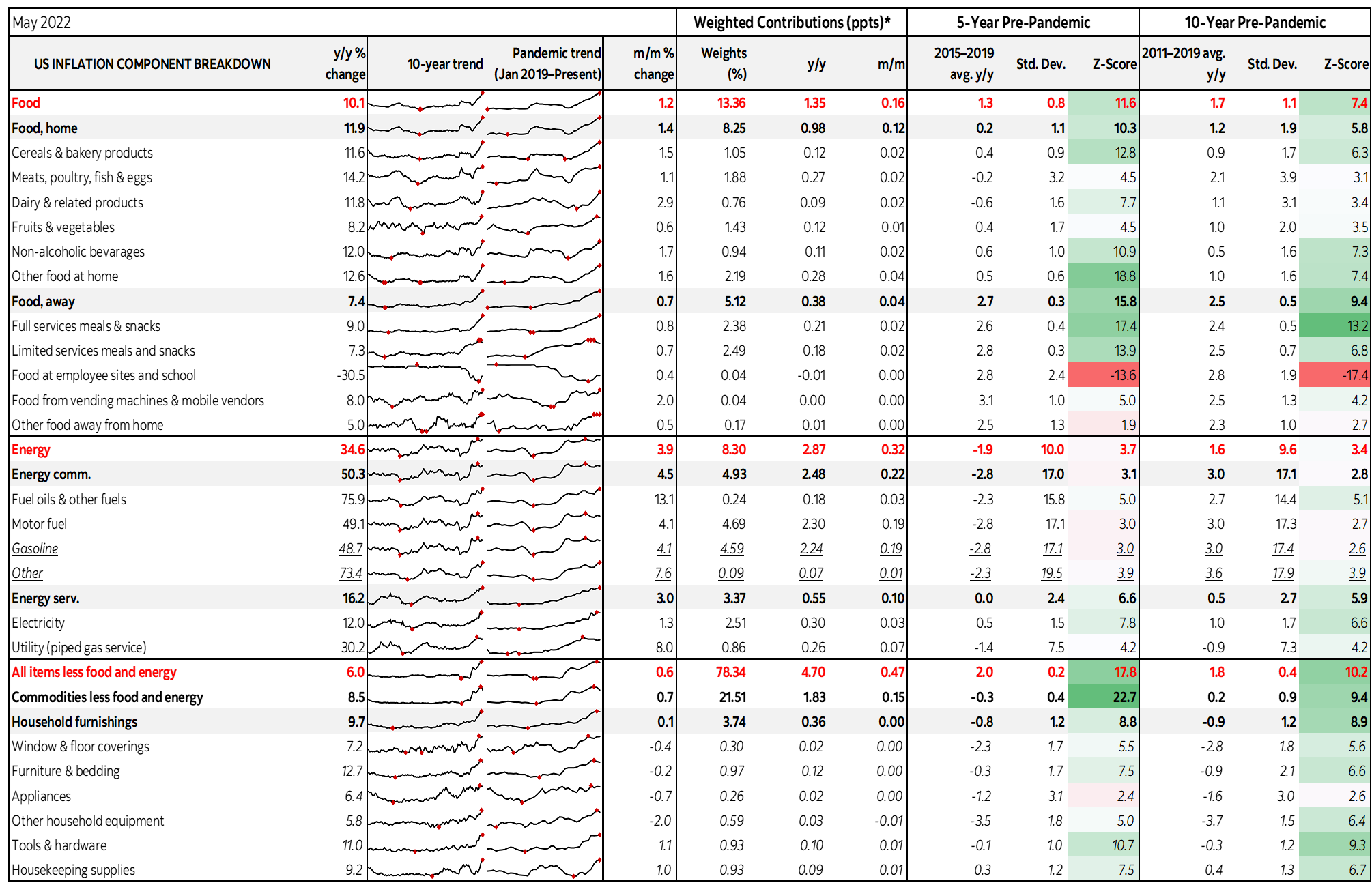

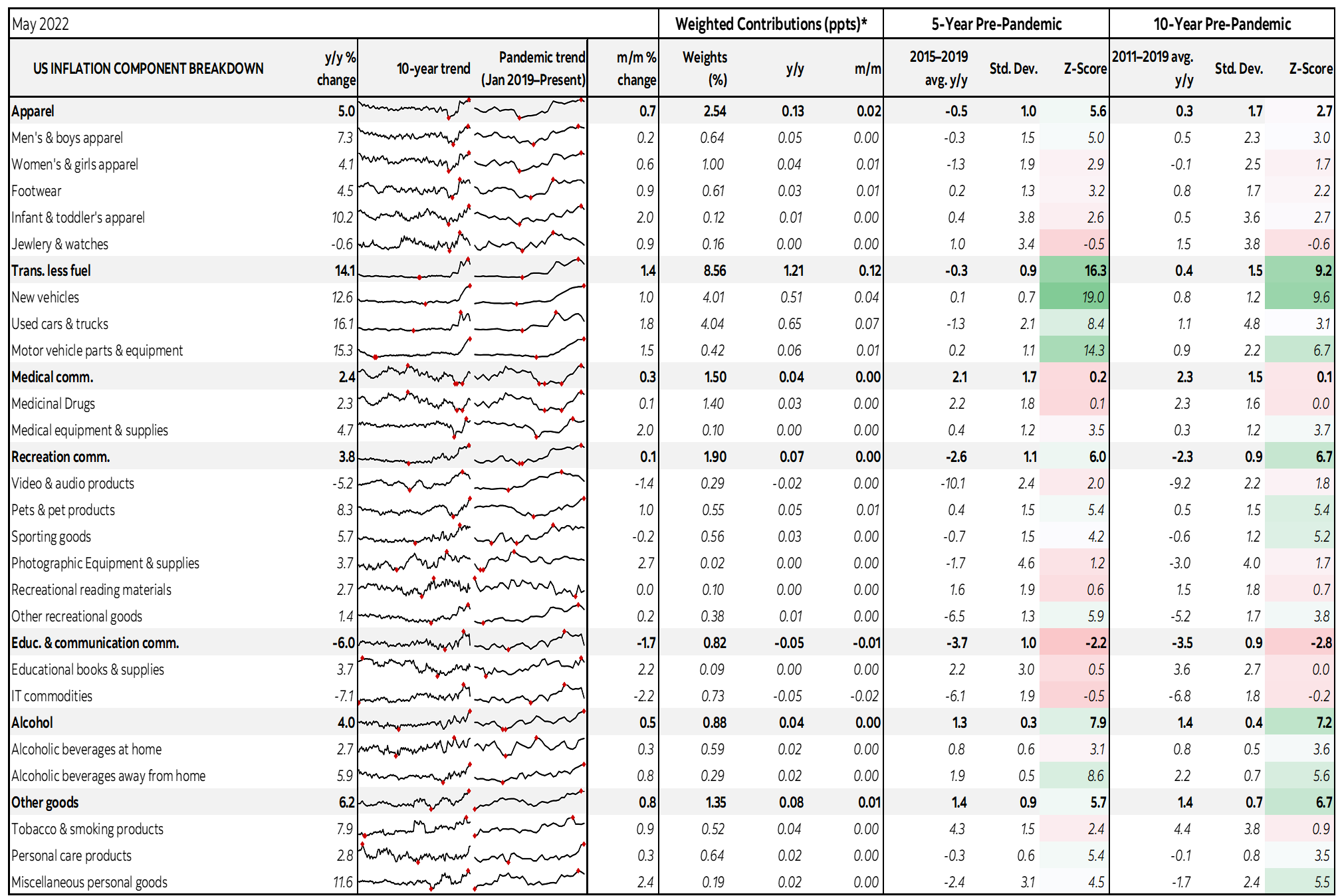

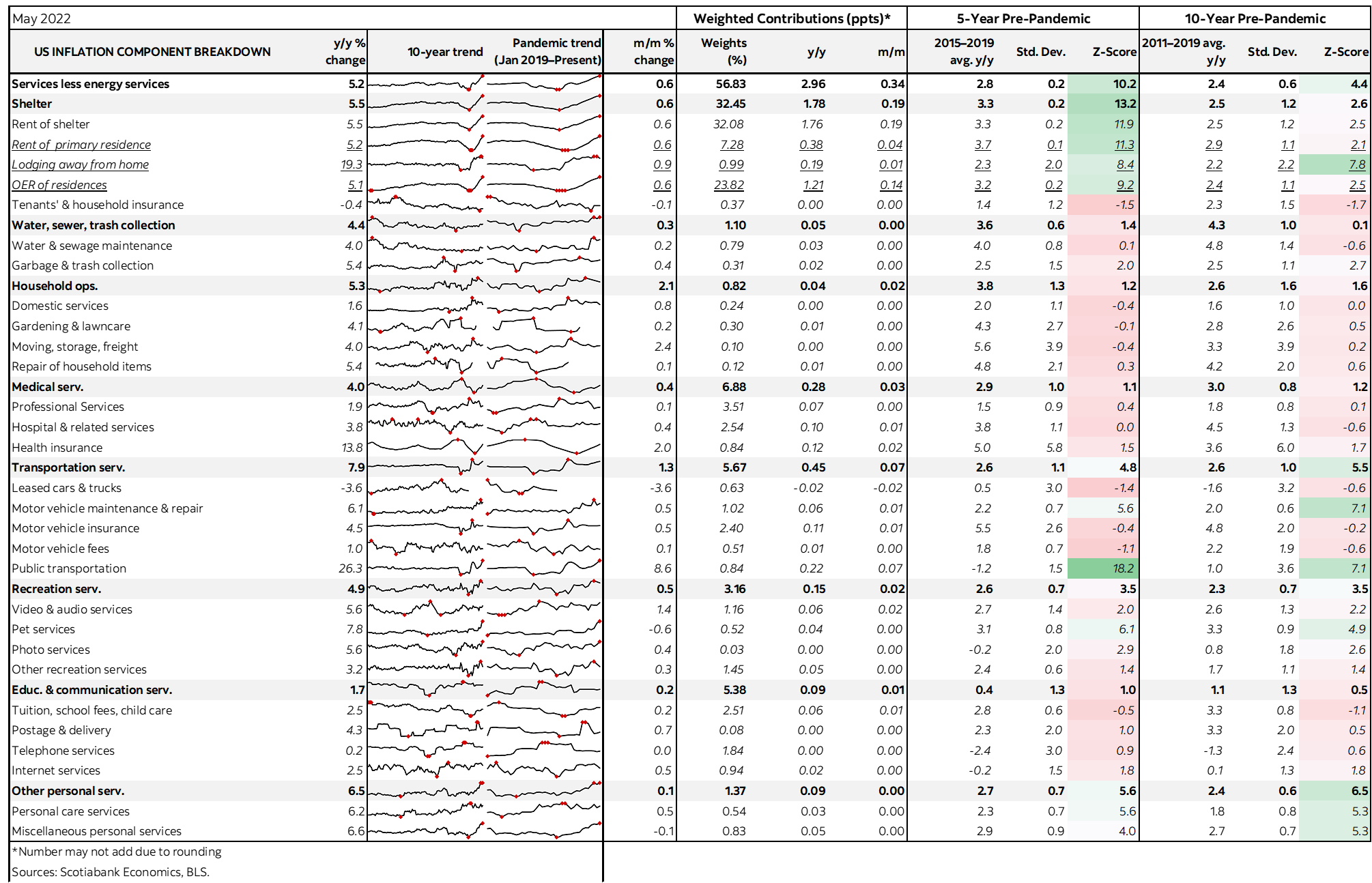

Please also see the detailed table on the back page that breaks down all components of the basket with micro charts, weights, standard deviations and z-scores as a measure of how abnormal the price changes by category are relative to multi-year periods.

As a final observation, given the higher odds that the Fed will pick up the size of hikes likely in July with June risk, this makes is significantly more likely that the Bank of Canada will hike by a bigger amount than 50bps at its July meeting and probably 75bps. Both central banks are absurdly behind where they should be. Similar domino effects are occurring across gilts and EGBs as a faster pace of Fed tightening is implying spillover effects into other central bank decisions.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.