- The fed funds policy rate was left unchanged at 4½% as widely expected

- Markets didn’t like Powell’s continued patience…

- ...that avoided teeing up a cut in September…

- ...in favour of watching “months” of data and developments

- Trump photobombed the Fed with tariff announcements on copper, commercial de minimis exemptions and Brazil

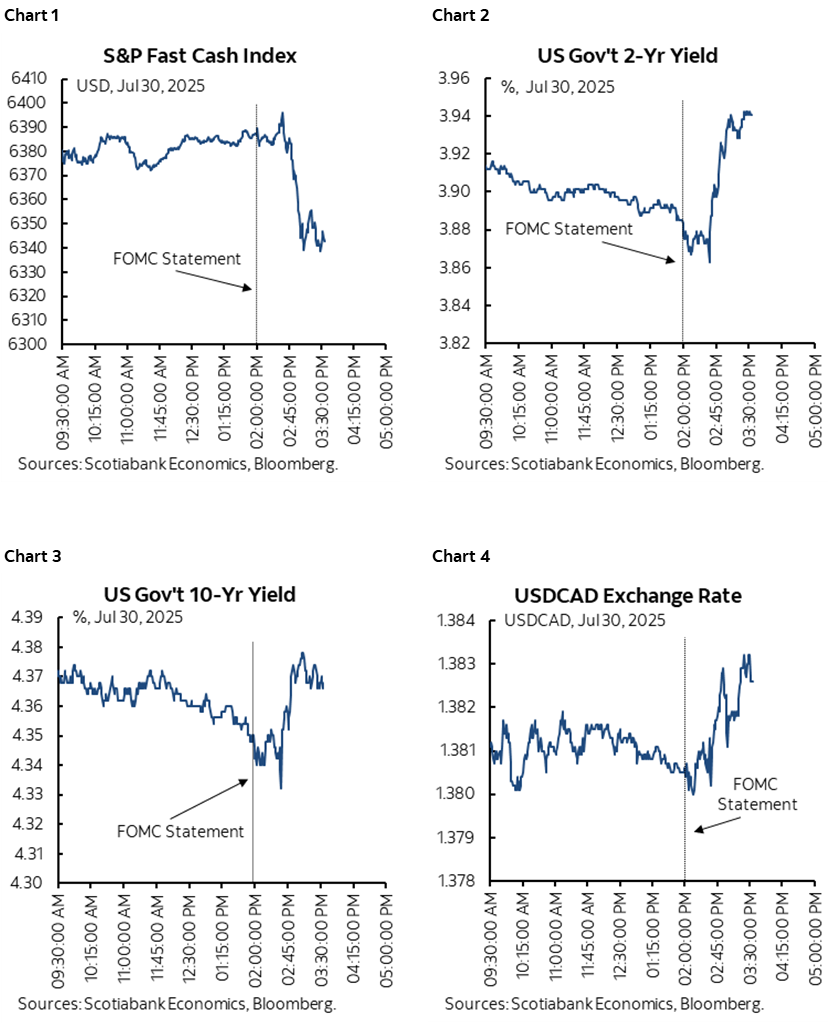

The FOMC left the fed funds target range unchanged at 4.25–4.5% as universally expected. There were small statement changes and two dovish dissenters that were not surprising, but Chair Powell remained noncommittal in terms of if—and—when the Committee may ease monetary policy. President Trump photobombed the communications with a series of tariff announcements at the 2pmET drop of the FOMC statement.

Markets responded by pushing the S&P500 down about ¾% mostly during the press conference as they hoped for a clearer sign that easing could begin by the September meeting and did not get one. The two-year Treasury yield moved up by about 6–7 bps also mostly during the press conference. The ten-year Treasury yield backed up and the USD appreciated. See the intraday moves in charts 1–4. Fed funds futures pricing for the September meeting was pared by about 4bps toward a 50–50 bet and cumulative pricing for the rest of this year was pared by about 7–8bps to less than 40bps.

Overall, the communications largely met my expectations for a neutral-hawkish stance.

STATEMENT CHANGES

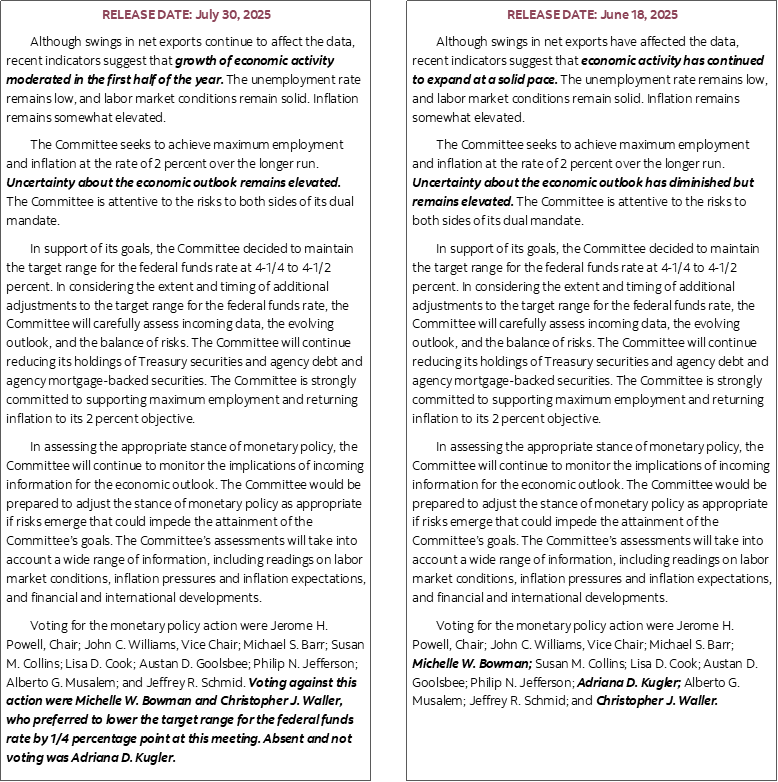

There were only three statement changes and only one that mattered. Please see the accompanying statement comparison.

The one that mattered was on the voters. Two dissented in favour of cutting at this meeting. They were Governors Waller and Bowman. Governor Kugler was absent.

Secondly, the statement now says “growth of economic activity moderated in the first half of the year.” That’s largely just a truism. Q3/Q4 growth last year was 3.1% and 2.4%. Q1/Q2 growth this year was -0.5% / 3.0%.

Third is the changed reference to uncertainty that struck out diminished and just says it remains elevated. Theoretically that could just be flagging that it hasn't continued to diminish since the June meeting, or that it has increased since then. Powell clarified what was meant in his press conference by saying that at the time of the last meeting, uncertainty had moved down a bit, but this time it had not so they struck that out.

MORE TARIFFS

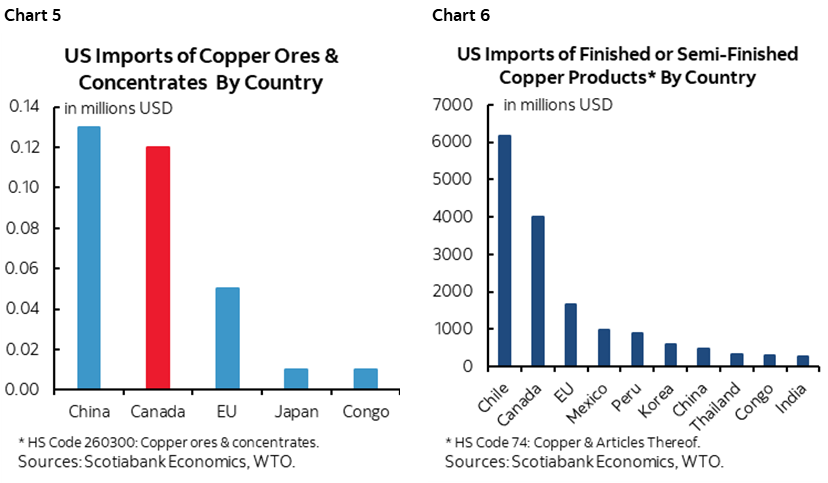

The White House issue a series of ‘fact sheets’ on tariffs at the same time as the FOMC statement landed. Either they were trying to bury any reaction behind the Fed or goading the Fed, you pick. Rarely are such thinks merely coincidental. The copper is here and see charts 5–6 that show where the US gets the affected products, the De Minimis commercial exemption announcement is here, and the Brazil one is here.

PRESS CONFERENCE HIGHLIGHTS—PATIENCE OVER “COMING MONTHS” AND NO SEPTEMBER TEE-UP

Chair Powell came out swinging at the start of his press conference by saying growth is solid, labour markets are largely in equilibrium at full employment with inflation a bit above target. His opening line was therefore communicating no urgency to ease.

He then noted that increased tariffs are pushing up prices in some categories of goods and that nearer term inflation expectations have also edged up and are probably driven by tariffs while longer-term measures remain reasonably anchored.

Powell extended his tariff focus by noting that higher tariffs are beginning to come through but the overall effects on inflation are uncertain. He said that the view that it is a temporary one-off price level adjustment is reasonable. He said it is also reasonable that they could feed more persistent price pressures. Time will tell.

What I thought leaned against September 17th in terms of possible easing was Powell’s remark that "In coming months we will receive a good amount of data" that will inform their stance. Key here is the "coming months" reference that doesn't sound like September by way of wishing to see a fair amount of data and developments.

When asked directly about a cut in September, Powell said “We have made no decisions about September. We will take all information as we make our decision at the September meeting.” He went on to cite evidence that the policy rate is modestly restrictive, the labour market is solid, financial conditions are accommodative, and that the economy is not performing as if the policy rate is holding it back. Powell described policy as modestly restrictive and that this seems appropriate.

When asked what the Committee has learned over the past few months about the price pass through process including the June report that showed some tariff effects and whether two months is a long enough horizon to evaluate how tariffs are affecting inflation, Powell said:

“The evidence shows companies upstream from the consumer are paying most of the tariff effects for now. We expect to see more pass through to consumers. Little is being paid by foreign companies. We are just going to have to watch and learn empirically. I think we've learned that the process is going to be slower than expected at the beginning. We never expected it to be fast.”

Powell then said you could argue they are looking through tariff pass through effects so far by not raising rates and that in the end they will make sure this does not move from being a one-time price increase to being inflationary.

When asked what if the One Big Bill will add stimulus in 2026 and cut back on potential rate cuts next year, Powell said “The biggest part of the bill was making permanent existing law on taxes so we don't see it as significantly stimulative. It should be somewhat stimulative but not a lot.” True, though the MAGA camp thinks it’s highly stimulative.

CONCLUSION

The clear message continued to be one of patience. Bring on this Friday’s nonfarm payrolls and one more thereafter, two more PCE gauges and two more CPI prints, Q2 GDP revisions, a bevy of other data releases, and who knows what further policy changes by the US administration. If, however, tariffs continue to pass through into inflation with reasonably resilient payrolls at a lower breakeven rate in light of more restrictive immigration policy, then the Committee’s willingness to cut in September is likely to remain low.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.