- The BoC held its overnight rate at 2.75% as widely expected

- Forecast uncertainty intensified with the addition of a third projection scenario

- The BoC still does not see progress on its core four issues

- Friday’s tariff deadline could trigger the BoC’s escalatory stagflationary scenario

- Fiscal policy was ignored for now, but fiscal easing will be incorporated later

- The BoC saying the choice is to hold or cut is meaningless and not new info...

- ….without any signalled confidence about what could happen

- BoC missed the upswing in core inflation, sounds too confident about a downswing

The BoC held its overnight policy rate unchanged at 2.75% as universally expected and priced. Its lack of any useful forward guidance and continued avoidance of a base case forecast in favour of three scenarios now versus two back in the prior MPR in April basically said they haven’t a clue what to do next. I don't find we learned anything new whatsoever about the policy bias from this set of communications.

The (long) statement is here and compared to the prior one in the appendix. The MPR is here, Governor Macklem’s opening remarks to his press conference are here, and I’ve included an attempt at a press conference transcript in this note.

MARKETS SHOOK IT OFF

If you were trading it, this was barely worth getting up out of bed for. The Bank of Canada came and went with the same confused stares and minimal impact upon markets. US data mattered more to the C$ that depreciated after US GDP and core PCE hit (recap here) and then moved sideways.

Canada’s short-term yields barely flinched; the two-year yield was rising by 2–3bps into the announcements and then position covering temporarily drove it about 3bps lower to and the yield is now flat on the day.

The OIS market still has basically no move priced for the September 17th meeting beyond a handful of basis points. The October meeting’s pricing is on the fence between a cut and a hold. The December meeting is about 60% priced for one rate cut. None of those contracts were materially affected by today’s communications.

As should be the case. The BoC continues to stand in the middle of the road and blinded by the coming headlights. I honestly can’t fault them.

WHY THEY HELD TODAY

Macklem's opening remarks point to 3 main reasons for the hold today:

"First, uncertainty about US tariffs on Canada is still high. Discussions between Canada and the United States are ongoing, and US policy remains unpredictable.

Second, while US tariffs are disrupting trade, Canada’s economy is showing some resilience so far.

Third, inflation is close to our 2% target, but we see evidence of underlying inflation pressures."

THE SAME FOUR ISSUES

The statement retained the key paragraph that outlined the core four issues the BoC is focused upon settling before it may have any comfort in deciding upon next policy steps.

"Governing Council is proceeding carefully, with particular attention to the risks and uncertainties facing the Canadian economy. These include: the extent to which higher US tariffs reduce demand for Canadian exports; how much this spills over into business investment, employment and household spending; how much and how quickly cost increases from tariffs and trade disruptions are passed on to consumer prices; and how inflation expectations evolve. "

Please see my morning note (here) for an elaboration on the lack of progress toward answering these four key issues.

THREE SCENARIOS—ONE MORE THAN BEFORE—AND ANYTHING COULD HAPPEN

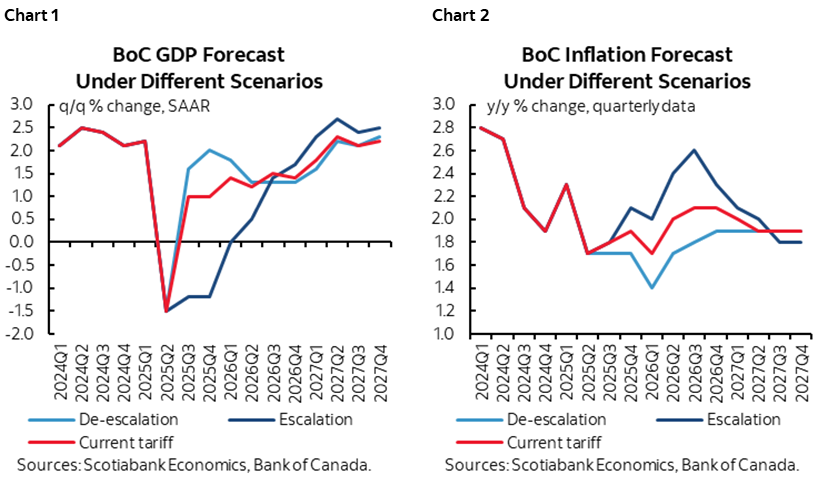

The BoC’s MPR presented three outlook scenarios this time, up from two back in the prior MPR in April. Back then, the BoC presented one scenario that negotiated away tariffs along an unpredictable process but uncertainty about trade policy remains, and another scenario added to that scenario’s assumption the other US tariffs since then and the assumption of a more damaging and long-lasting global trade war.

Today, they presented three scenarios. Do I hear a bid for four in October’s MPR? The current tariff scenario takes all tariffs in place of agreed upon to date. One alternative scenario emphasizes a reduction of tariffs and another scenario assumes tariffs are increased further—the so-called de-escalation and escalation scenarios.

Charts 1 and 2 show the GDP and inflation forecasts under each of these assumed three scenarios.

It is important to note that their ‘current’ tariff scenario is indeed current as of today and does not include Trump’s current threat of a 35% rate on Friday August 1st that he said this morning is a deadline that stands, or copper or pharma or any other tariffs. It takes tariffs to this day including 50% on steel and aluminum, 25% on non-US content of imported vehicles, 25% on motor vehicle parts not in compliance with the CUSMA agreement, a 25% tariff on imported goods not CUSMA-compliant except energy, electricity and potash at 10%. The current scenario also takes Canadians pledged retaliatory measures to date, not ones that may escalate.

If the August 1st tariff threat becomes reality, then the most likely scenario could be the escalatory one that they offered that deepens the US tariff shock and Canada’s response. That one points toward rising inflation and sagging growth in a stagflationary shock that would be highly complicating for the BoC.

Three scenarios instead of two now signals greater uncertainty overhanging the BoC’s decision making process in my books.

The implications for inflation that stem from each scenario were clearly laid out by the BoC without leaning toward which one they think is more probable:

"In the current tariff scenario, total inflation stays close to 2% over the scenario horizon as the upward and downward pressures on inflation roughly offset." That 'current tariff' scenario doesn't say cut.

"As the alternative scenarios illustrate, lower tariffs would reduce the direct upward pressure on inflation and higher tariffs would increase it. In addition, many businesses are reporting costs related to sourcing new suppliers and developing new markets. These costs could add upward pressure to consumer prices."

Chart 2 shows the impact.

STATEMENT SAID HOLD OR CUT—WHAT ELSE DID YOU EXPECT?

And yet some headlines chose to ignore all of this and made a bigger deal out of the following sentence in the statement than had merit:

“We will continue to assess the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs related to tariffs and the reconfiguration of trade. If a weakening economy puts further downward pressure on inflation and the upward price pressures from the trade disruptions are contained, there may be a need for a reduction in the policy interest rate.”

Of course! But those are big ‘ifs’ that leave us no better off in terms of evaluating their likelihood than the statement of the obvious. And again, the clear signal from the BoC is that they haven’t a clue what to expect. The usual rate bullish shops had a very selective interpretation of the BoC’s communications today.

CORE INFLATION DRIVERS

Backing up the openness toward possible easing, while not saying anything new, seems predicated upon the BoC’s thinking that core inflation pressures could subside:

“There are reasons to think that the recent increase in underlying inflation will gradually unwind. The Canadian dollar has appreciated, which reduces import costs. Growth in unit labour costs has moderated, and the economy is in excess supply. At the same time, tariffs impose new direct costs, which will be gradually passed through to consumers. In the current tariff scenario, upside and downside pressures roughly balance out, so inflation remains close to 2%.”

What happened to Governor Macklem’s prior speeches about how trade turmoil and global fragmentation raise costs through inventory and supply chain and other adjustments that may be persistently passed onto higher prices? That’s absent in this reference when it’s arguably among the reasons why they missed the surge of core inflation to date to begin with. And output gaps? Oh please, they’re overrated. Canada has been in excess supply according to the BoC’s two output gap measures for 8–10 quarters and yet core inflation has remained highly persistent on the properly defined m/m SAAR basis across all three main measures and the breadth of price increases has been trending higher.

WHAT WAS GLARINGLY MISSING

There was no mention of the potential implications of a Fall budget or fiscal policy effects other than sector-specific supports. That may just be the BoC playing safe politics but is not addressing the clear risk that significantly expansionary fiscal policy is waiting in the wings on top of modest measures introduce through ways and means actions this summer. Fiscal easing could easily substitute for monetary easing if required, or pivot the monetary policy dialogue in the other direction pending what happens to the rest of the picture.

IS THE TARIFF THREAT EXAGGERATED?

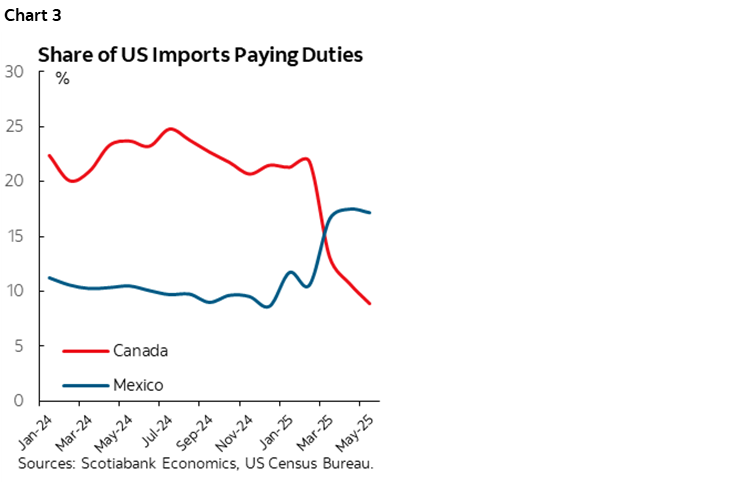

The BoC’s estimate of the ultimate amount of Canadian exports that could be CUSMA/USMCA compliant is a bit higher than what we observe and expect. They think it could be 95% of all non-energy exports and 100% on energy exports. We’ve tended to argue it could be around 90%. Chart 3 shows that using US customs data it may already be 90% based on duties actually being collected. SDG Rogers addressed this issue in the press conference (see below).

One point I've been making with clients is that if escalation is avoided and the blueprint of deals with other countries applies, then the tariff threat to Canada is at risk of being exaggerated especially in relation to other developments. It is and could be a big deal for select individual sectors, like metals.

But if, say, we get a 15–20% tariff like on the US imposed on Japan, the EU, and the UK’s slightly lower rate among others, and the administration officials continue to indicate that it's likely to apply only to non-CUSMA/USMCA compliant trade, then 15–20% on 5–10% of our trade is frankly peanuts. That’s probably one reason why USDCAD has moved off earlier peaks as CAD appreciated alongside the market’s diminishing fears about tariffs since ‘Liberation Day’ on April 2nd. If the tariff threat intensifies further, then CAD can adjust again which is a cautionary note for core inflation.

I think what matters more to Canada than the price elasticity of exports to tariffs is the income elasticity of US demand for Canadian exports stemming from growth south of the border. In plain english, if the US economy remains resilient, then it will keep on pulling in more imports from Canada at low effective tariff rates if that scenario turns out to be correct. What matters far more to Canada is whether US growth remains decent.

On that note, we do indeed have cooling US growth as the bigger concern. There are multiple studies on the impact of Trump's immigration policies on cooling US growth. The uncertainty factor is costing US growth and may be why private domestic sales were weak in this morning's US GDP figures. The bond market is stepping in against fiscal policy. So is the Fed. And tariffs will likely cost the US growth by souring world trade which benefits no one, and crimping domestic purchasing power of US consumers and businesses. The US economy has defied expectations for quite some time, but a very reasonable narrative can still point toward downside risks to US growth eventually emerging if they are not already.

In short, keep an open mind toward all scenarios including the possibility of a lessened effective tariff hit combined with easier fiscal policy and a real policy rate that is already around 0%. That’s not a particularly dovish scenario.

PRESS CONFERENCE TRANSCRIPT

What follows is an attempt at providing an account of the Q&A with journalists during the press conference. Any errors or omissions are to be blamed on my tpyingg skills absent a formal transcript.

Q1. Even if there is some sort of agreement between Canada and the US, won't the pending review of CUSMA/USMCA keep uncertainty elevated?

A1. Let's hope there is an agreement and it is a good agreement, but yes, there is a sense that US policy may well remain unpredictable, that it is going to be hard to restore trust, so yes some uncertainty will continue. We do have a fair amount of uncertainty in our current tariff scenario for some time that eventually falls off. In our deescalation scenario it diminishes but uncertainty remains.

Q2. The central projection has core inflation at 3% for the rest of this year. How significant is that to being a barrier to providing relief to Canadians?

A2. One of the reasons we held is that we are seeing pressures on core inflation. They've all moved up. That has got our attention. Going forward, we are going to be watching closely those developments. Some of the factors could unwind like CAD depreciation, like unit labour costs and wage growth decelerating, and excess supply. With tariffs, we're just starting to see the effects including the counter measures and that's going to be putting some upward pressure.

[ed. in the past, Macklem has said labour markets and wages are not playing a role in driving inflation which indicates a very asymmetric bias toward the influence of productivity adjusted employment costs on inflation].

Q3. Can the Bank live with 2 1/2% inflation or is that still too high?

A3. If inflation is currently 2 1/2% but pressures suggest it will unwind and head back to 2% then we're comfortable. If we think inflation remains there or rises then we're not comfortable. It depends upon the path forward and we need to think more about the risks. We're not thinking about a single forecast but a range of scenarios. Hopefully things will become clearer.

Q4. You note the effective tariff rate rising by five percentage points but what is your starting point? How do you arrive at your 95% USMCA compliant estimate?

A4. Rogers answering. The baseline was close to zero. We get to 5% using the weighted composition of trade and current tariffs. The 95% compliance rate is a forecast assuming more motivation to complete the paperwork to become compliant.

A4 cont'd: Macklem expanding. The situation is fluid. These scenarios are based on a lot of assumptions. We'll see where they land. There is more than one outcome here.

Q5. Will there still be a need for a rate cut this year if your current tariff scenario holds?

A5. We're going to take our decisions one at a time. I can say three things. The situation hasn't changed that much since our last decision. Given the uncertainty, we're continuing to put more emphasis on the risks and are ready to respond. We repeated the same four things we are focused upon outlined in the statement. And we've said looking ahead if the weakness in the economy creates further downward pressure on inflation and those upward cost pressures on inflation are contained then there could be a need for a further cut. I think that gives you a sense of the current situation. What will we be doing? We'll be following things like everyone else. We've given detail about the various indicators and readings we're looking at and that we'll continue to ensure inflation is well controlled.

Q6. You are not expecting a recession this year and bounceback later. What are the reasons for the bounceback?

A6. The quarterly profile for GDP is being affected by these swings in tariffs. There is a very sharp deceleration of exports in Q2 that weakens growth. Having declined sharply in Q2 they shouldn't contract as much in Q3. On the consumption side, it is still growing, being restrained by uncertainty, but still growing and expected to continue through the third and fourth quarters. In that scenario growth picks up in 2026–27

Q7. Back in May you said you expect permanent scarring from tariffs. What's your thinking now, have there been substantial effects?

A7. Growth stays below 2% and is permanently lower. Tariffs mean the economy works less efficiently. The economy will resume growing but remain on a permanently lower path unless the tariffs are removed. [ed. presumably so does potential growth]

Q8. Premier Ford is calling on the BoC to cut interest rates now. What do you say?

A8. We make decisions independent of the political process in a way that will fulfill our mandate. The experience of the past few years underlines how much Canadians don't like inflation. We will support the economy while also ensuring a tariff problem does not become an inflation problem.

Q9. Does the BoC see settlement balances moving to a level that would require the BoC to bring forward purchases of treasury bills?

A9. Our plan hasn't changed, we still think we'll settle around $50–70B in settlements balances with no change to our plans right now.

Q10. How does the BoC make sure that sectoral weakness due to tariffs doesn't spread to other industries?

A10. Steel and aluminum tariffs of 50% are having a very severe and direct effect. But when we look beyond the directly affected sectors it is continuing to grow. Employment in the rest of the economy has continued to expand. Consumption is continuing to grow. The economy is showing some resilience so far. We will be watching closely what happens with tariff themselves as part of that. Hopefully we can continue to move toward the deescalation scenario but that's not the only possible outcome. Clearly monetary policy is not a tool you can use to target specific sectors which is a role for fiscal policy which has been doing this. We need to look at the overall economy and spillover effects.

Q11. Voters have turned more right wing in more economies and reversing more open trade and immigration policies globally. Just wondering if any uncertainty over trade rules is clearing up. Does not having political pressure from the PM like the President in the US make your job easier?

A11. I think I need a speech to answer the question. Even before Trump was elected trade has been shifting. The world is fragmenting and that is going to have an impact.

Q12. What are the BoC's thoughts about massive increases in defence spending and the impact on productivity?

A12. Rogers answering. In the long-run it probably will help productivity. They generate some economic activity in Canada. Those things take a long time to work through the economy. [ed. personally I think that’s highly doubtful as significant defence spending leaks out of the economy and the end product plays no direct role in producing anything].

Q13. How much could Fed cuts indirectly impact Canada making easier less possible here?

A13. We have a flexible exchange rate and can gear monetary policy to the needs of the Canadian economy.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.