- Core CPI posted a modest gain...

- ...as core services CPI ex-housing flat lined...

- ...and core goods CPI slipped

- Markets continue to price a July Fed hike, slightly lower terminal rate

- There remains translation risk into core PCE

- US CPI / core CPI, m/m %, SA, June:

- Actual: 0.2 / 0.2

- Scotia: 0.3 / 0.3

- Consensus: 0.3 / 0.3

- Prior: 0.1 / 0.4

- US CPI / core CPI, y/y %, SA, June:

- Actual: 3.0 / 4.8

- Scotia: 3.1 / 5.0

- Consensus: 3.1 / 5.0

- Prior: 4.0 / 5.3

US core CPI inflation landed weaker than expected and continued an ebbing trend under the hood. There is translation risk into the core PCE measure that matters more to the Federal Reserve, but it still leans in the direction of at least a temporary pause in inflationary pressures. There is the added caution that markets have been fooled by soft patches before.

Markets reacted by driving the two-year Treasury yield another 8+bps lower to add to the modest pre-data decline. The dollar weakened a little further and S&P equity futures rallied a touch. Markets continue to price a 25bps hike on July 26th but lowered terminal rate pricing by 2–3bps to price only part of an extra 25bps hike before year-end.

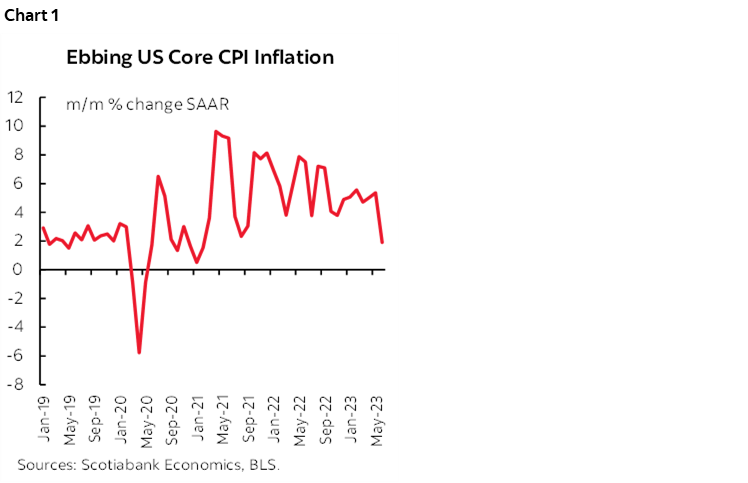

CPI ex-food and energy only tells a part of the story, but at 0.2% m/m SA it was on the weaker side of consensus and hence the year-over-year core measure pulled back to 4.8% (5% consensus, 5.3% prior). The annualized m/m core CPI was only 1.9% which is the weakest inflationary pressure at the margin since February 2021 and that demonstrates that the recent softening isn’t just a base-effect driven deceleration in the year-over-year rate (chart 1).

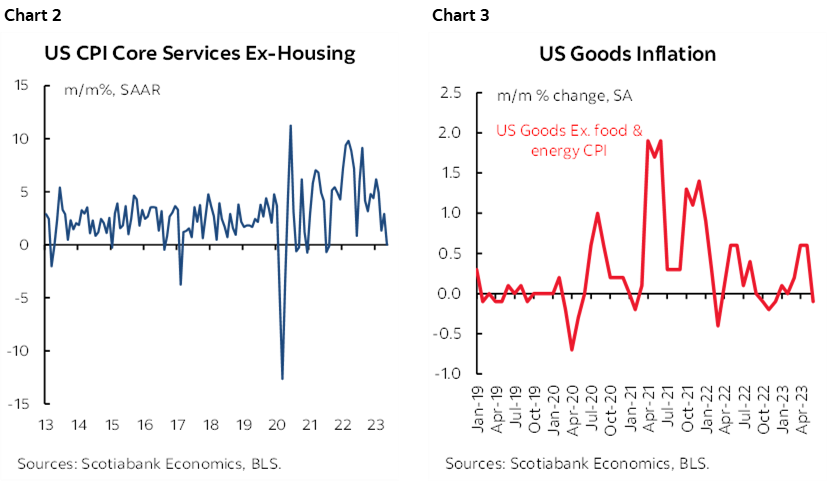

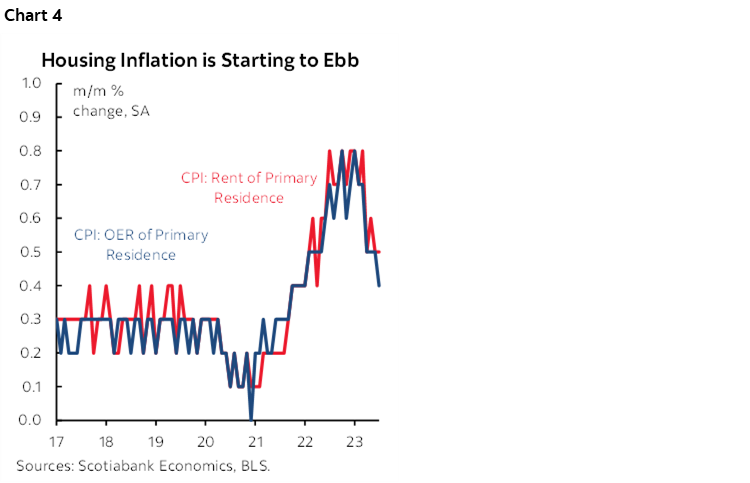

Key is that the twin trimmed-up core CPI gauges were soft again. Core services CPI ex-housing was flat and has been on an extended decelerating trend (chart 2). Goods CPI ex-food and energy fell by -0.1% m/m SA which indicates soft goods price changes (chart 3).

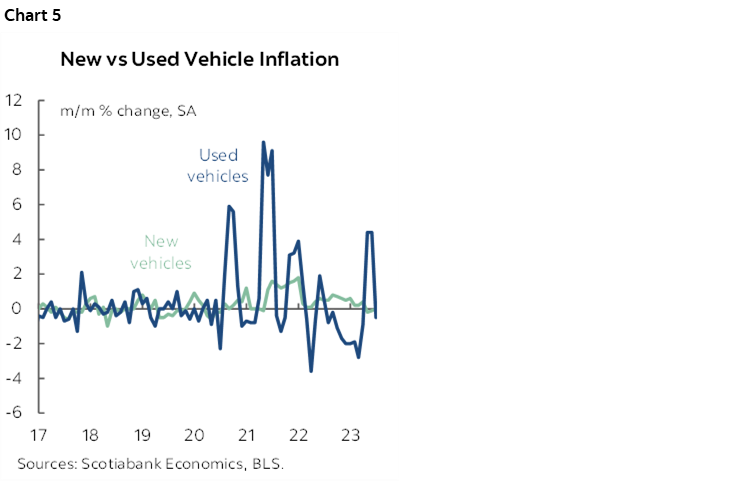

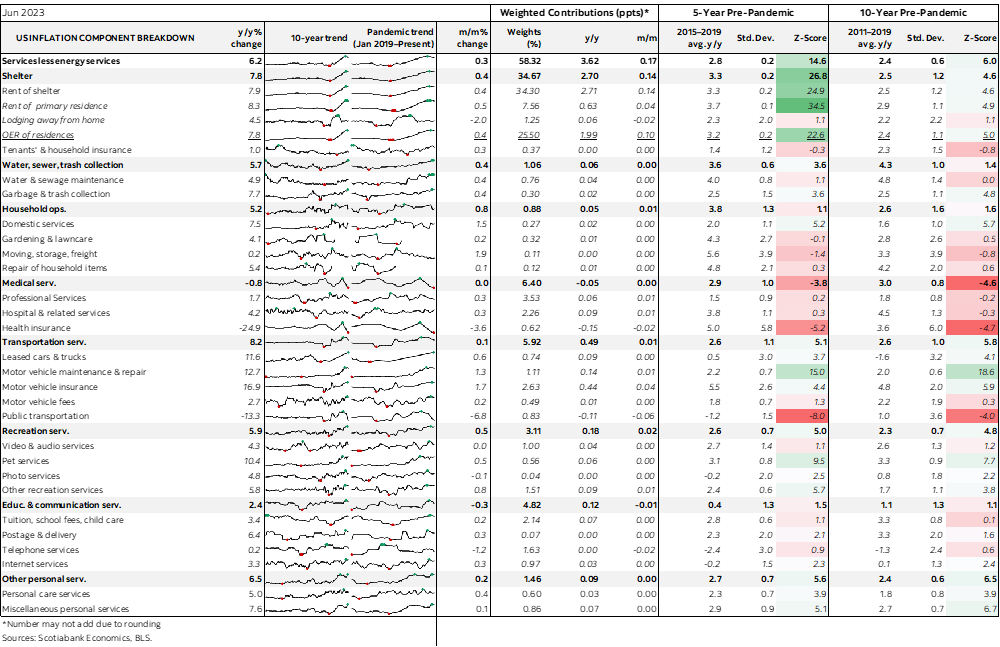

Shelter inflation eased to 0.4% m/m from 0.6% prior with OER up 0.4% from 0.5% prior. As chart 4 depicts, housing as captured in CPI is on an ebbing trend at the margin.

Used vehicle prices were well off industry guidance, down -0.5% m/m SA. New vehicles were in line with industry guidance for no change. Chart 5.

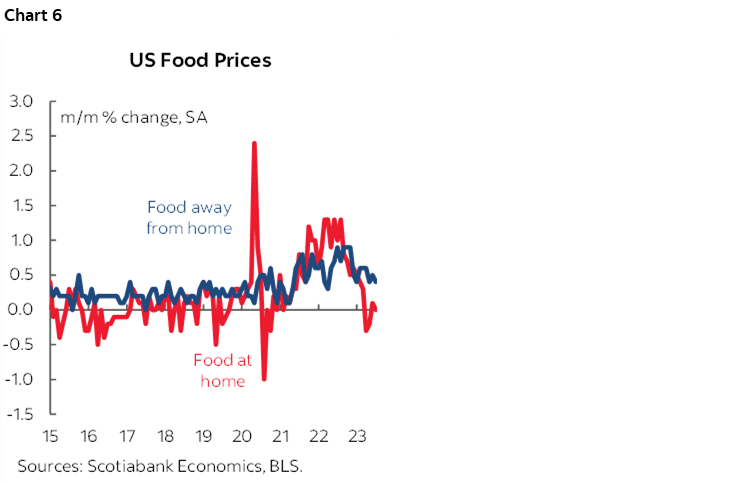

Food prices were little changed at +0.1% m/m with groceries flat and 'away from home' such as take out up 0.4%. Chart 6.

Energy prices were up 0.6% with gasoline up 1% m/m SA.

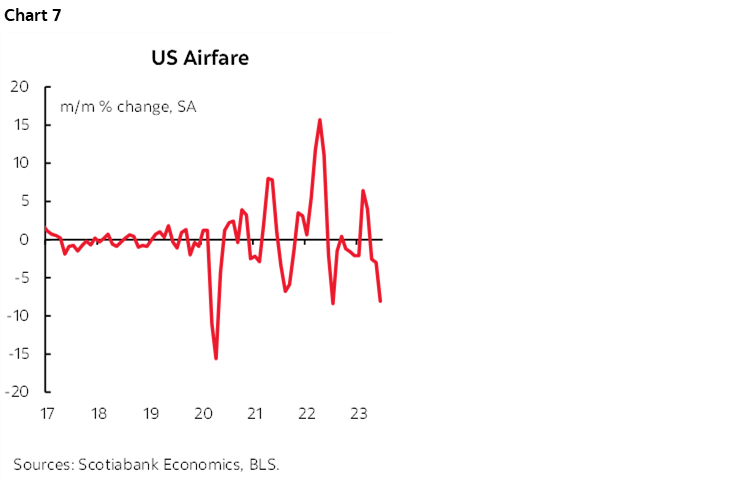

I’m not sure what’s going on with airfare despite all the industry talk, but it was down another 8.1% m/m from -3% prior and -2.6% the month before that for a significant and extended decline. Chart 7.

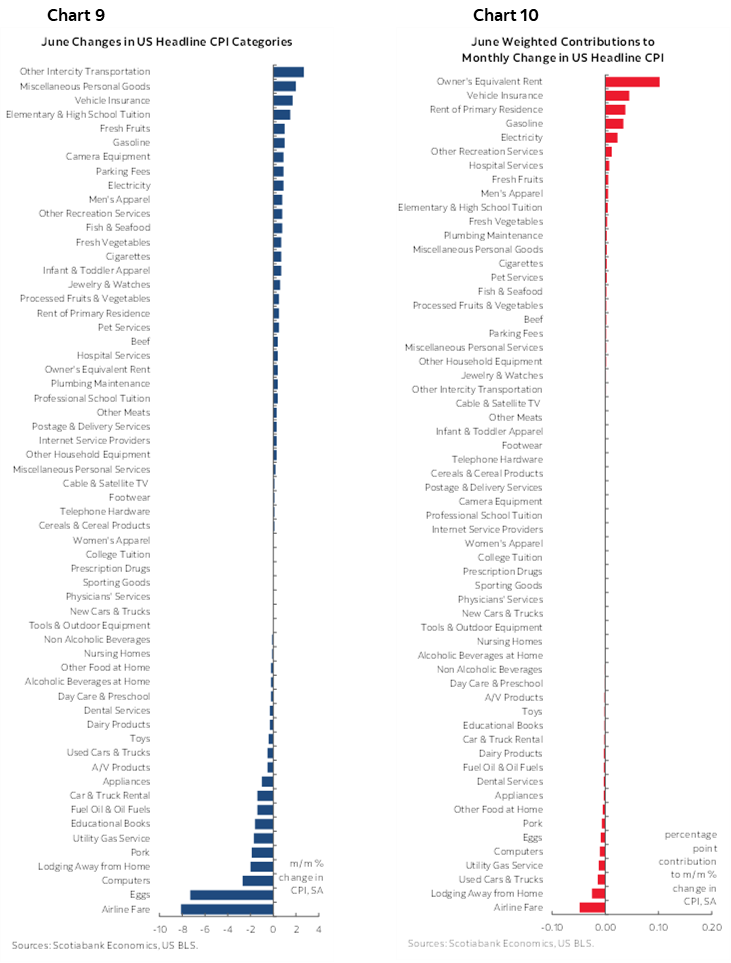

Charts 9 and 10 on the next page show the m/m % changes in CPI by components in unweighted terms and in terms of weighted contributions to the overall 0.2% m/m change in headline CPI.

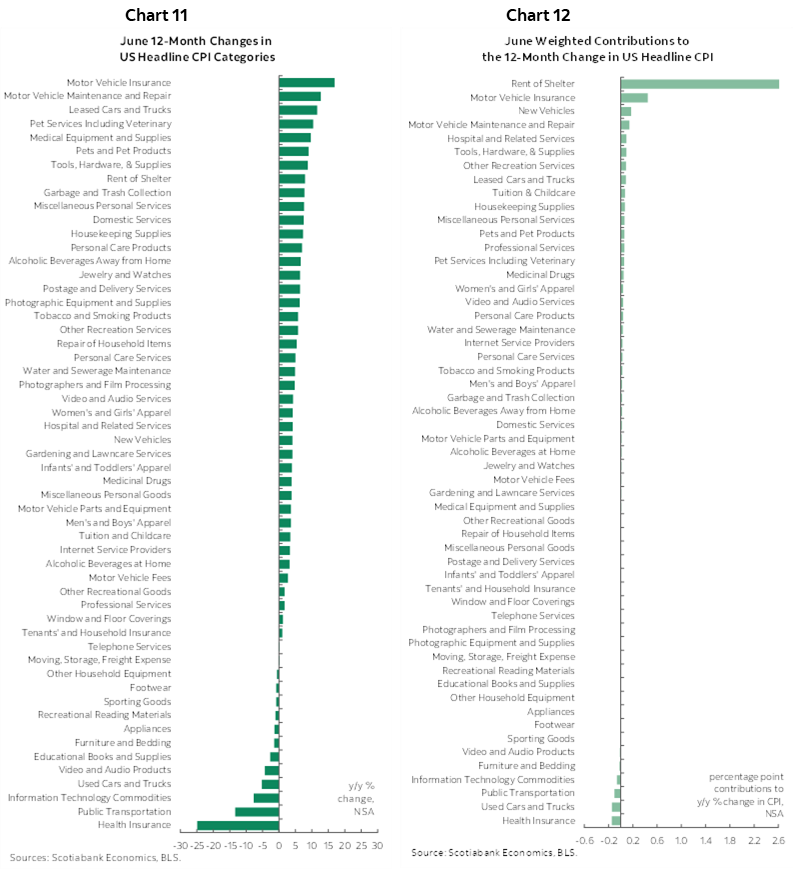

Charts 11 and 12 two pages ahead do likewise for the y/y changes.

A residual caution is that what happens to core CPI may not happen to core PCE, or at least not perfectly so. Core PCE has a much lower weight on shelter than core CPI, for instance, and so the deceleration in housing shouldn’t be as big of a contributor to the downside in core PCE.

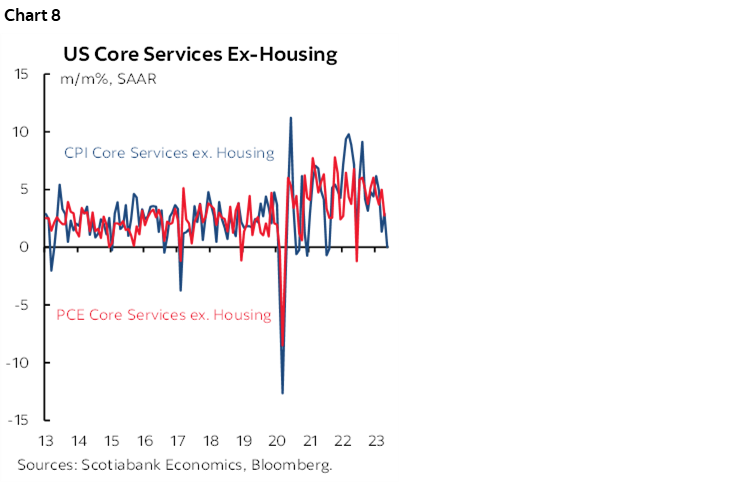

A way of demonstrating this point beyond just showing deviations in core PCE and core CPI over time is chart 8 below. Underlying core services CPI ex-housing can significantly deviate from core PCE services ex-housing with one reason being PCE’s lower much lower weight on housing than CPI.

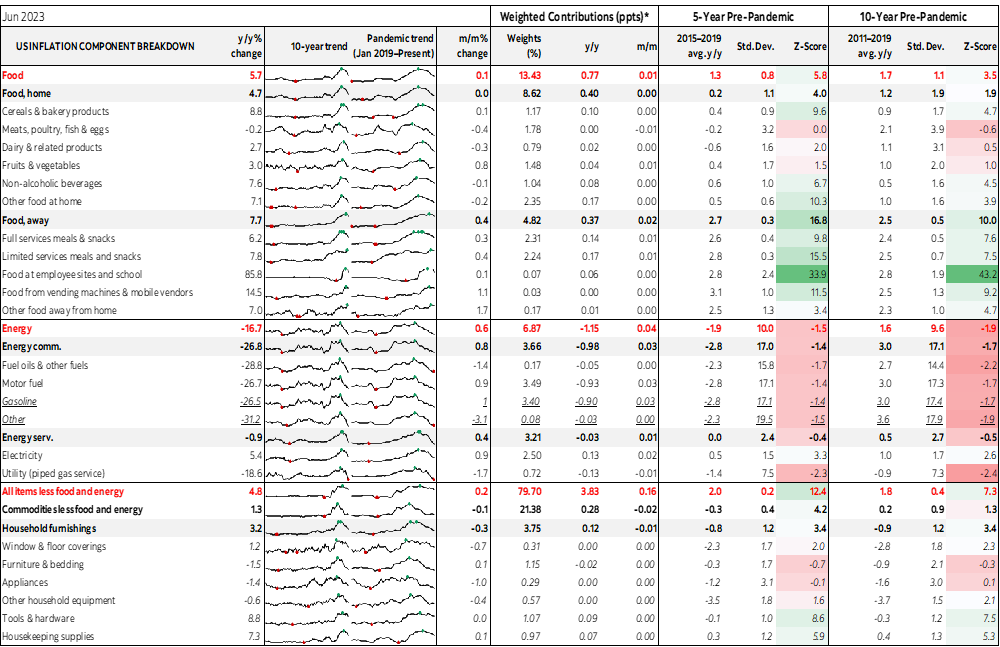

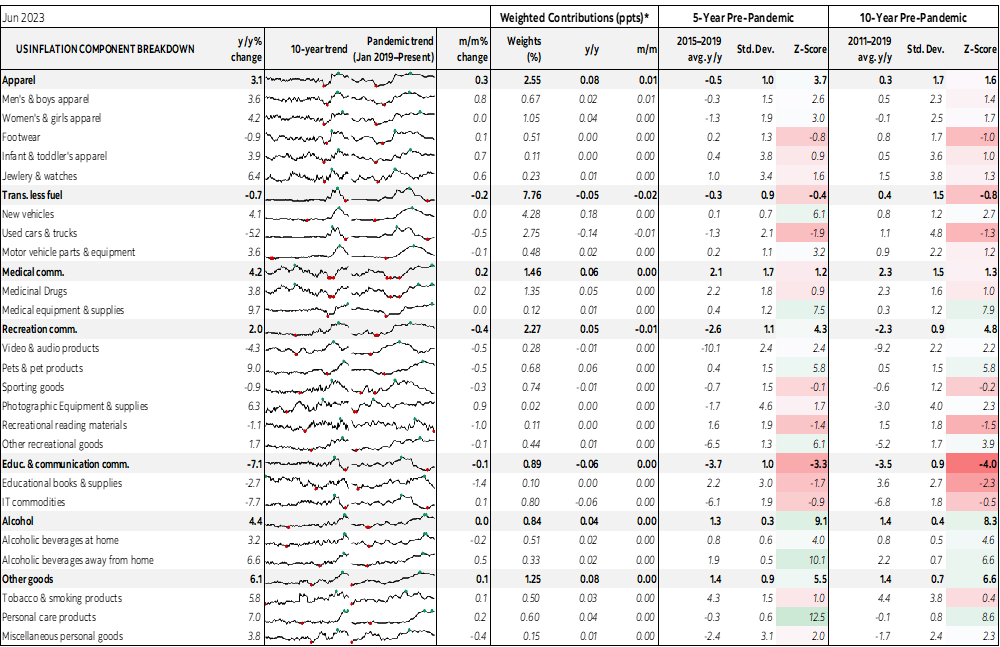

Please also see the accompanying table at the back of this note that shows more detail including micro charts and z-score measures of deviations from trend.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.