- Powell said a March cut is “not the most likely case.”

- The Fed’s perfectly understandable confidence problem

- Powell wisely rejects a rules-based approach

- A QT discussion was held and a fuller discussion was promised for March...

- ...which probably sets up a likely announcement to reduce Quantitative Tightening

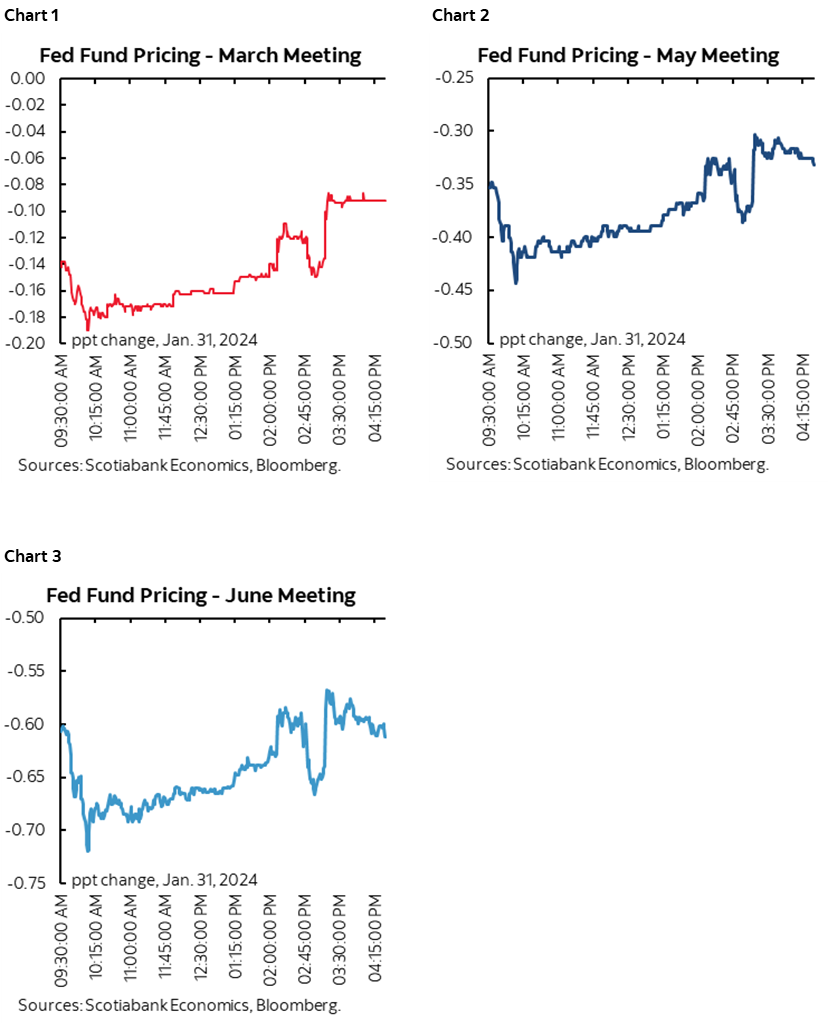

- All nearer-term FOMC meeting dates trimmed cut pricing

It took sixty minutes to get there and after premature headlines and comments about what was delivered, but eventually Chair Powell’s prime message was to explicitly rule out a cut by March and to set up a potential announcement on adjusting Quantitative Tightening at the next meeting. No policy changes were delivered. In all, the communications met my expectations.

Everything else about the statement and the rest of the press conference is of relatively little consequence. The biggest unanswered question is why it took so long to deliver the punchline today! That begs the question whether Powell was giving his own opinions after the statement and first sixty minutes of the press conference and going off-script.

What follows is a full account that summarizes my instant real-time views provided to our markets clients.

MARCH CUT? FUHGGEDDABOUDIT!

Chair Powell delivered his strongest rejection to date of market pricing for a rate cut at the March meeting. When asked whether it is premature to think that rate cuts are right around the corner, he said:

“We said in the statement we will move carefully. I don't think it's likely that the Committee will reach a level of confidence to begin easing by the March meeting. That’s probably not the most likely case.”

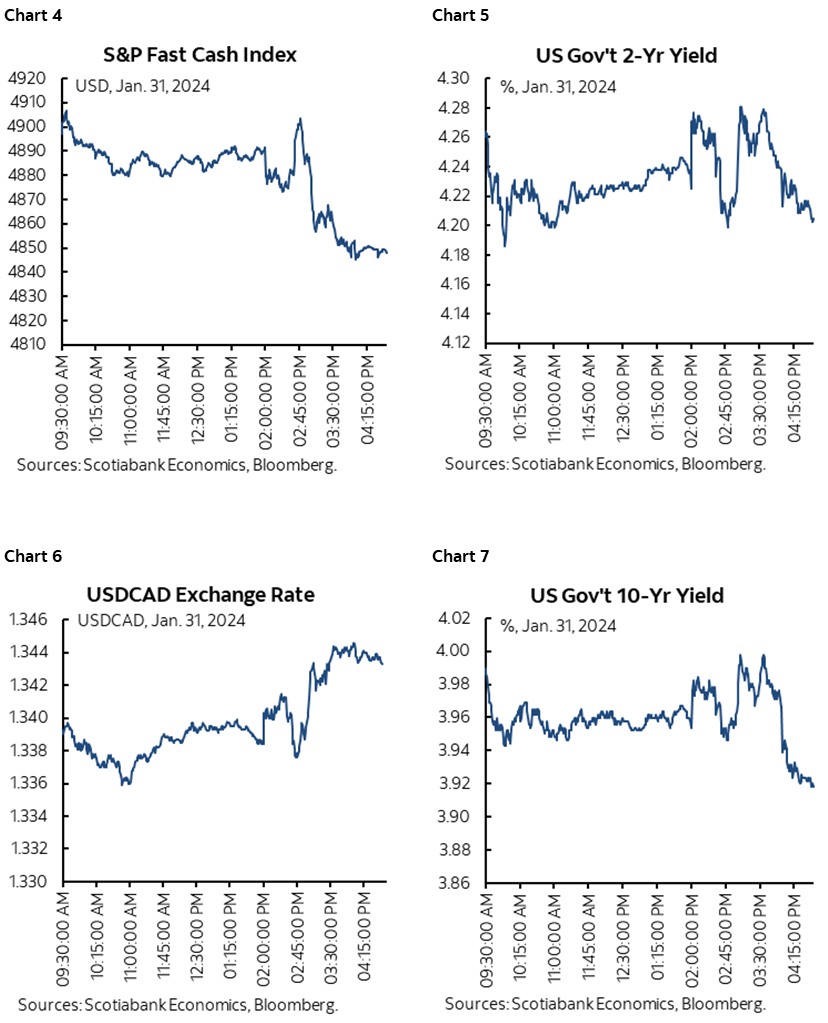

That trimmed market pricing for easing over coming meetings (charts 1, 2 and 3). Charts 4–7 show the intraday moves across other market measures.

Powell has the data line-up to back him up on that comment. The Committee will only get one more PCE print by March and two more payrolls/wages reports. It's doubtful that one or two more data points on each would give them the required confidence to take this to the next level and begin easing.

When asked whether a first cut would start a cycle of cuts or be a one-off, he sloped off the question by saying “It’s going to depend on the data.” Good answer.

When asked whether there was variation among FOMC members on the confidence to cut rates and how quickly to get there, Powell flat out said

“There was no discussion on cutting rates. We’re not at that stage. We’re not at a place of working out those details because we were not actively considering moving the funds rate down.”

NO DATE STAMPS

When asked how many months he thinks he might need to see lower inflation to have more confidence to ease, Powell said: “I'm not going to put a number on it.”

Good for you, we all know the perils to trying to outguess developments in this environment. Powell knows full well that projections have a nano-second shelf life.

QUANTITATIVE TIGHTENING CHANGES AFOOT

Toward the end of the press conference, Chair Powell was asked whether the Committee discussed slowing the pace of balance sheet run-off in the months ahead. He said that balance sheet run-off has gone well so far, and that:

“We did have some discussion on the balance sheet. We’re planning to have more in-depth discussion in March.”

That translates into a need to watch the FOMC meeting minutes three weeks from now for more about the range of the discussion at this meeting.

It also potentially tees up an announcement on changing QT parameters at that meeting.

When asked whether they would want to cut and moderate balance sheet run-off in tandem, Powell said “We see those as separate tools. It's not something we're planning but it could happen.”

When asked what he needs to see when considering whether to taper Quantitative Tightening and whether that includes seeing the overnight repo facility go to zero, Powell said:

“That's what we'll be talking about at the March meeting. I wouldn't say that's what we're targeting. We'll be looking at a variety of things over the next year or so.”

That 'over the next year or so" may be reference to the kind of timeline they have in mind for ending QT. It might imply rejection of a sudden ending of QT or a more compressed timeline.

STATEMENT CHANGES

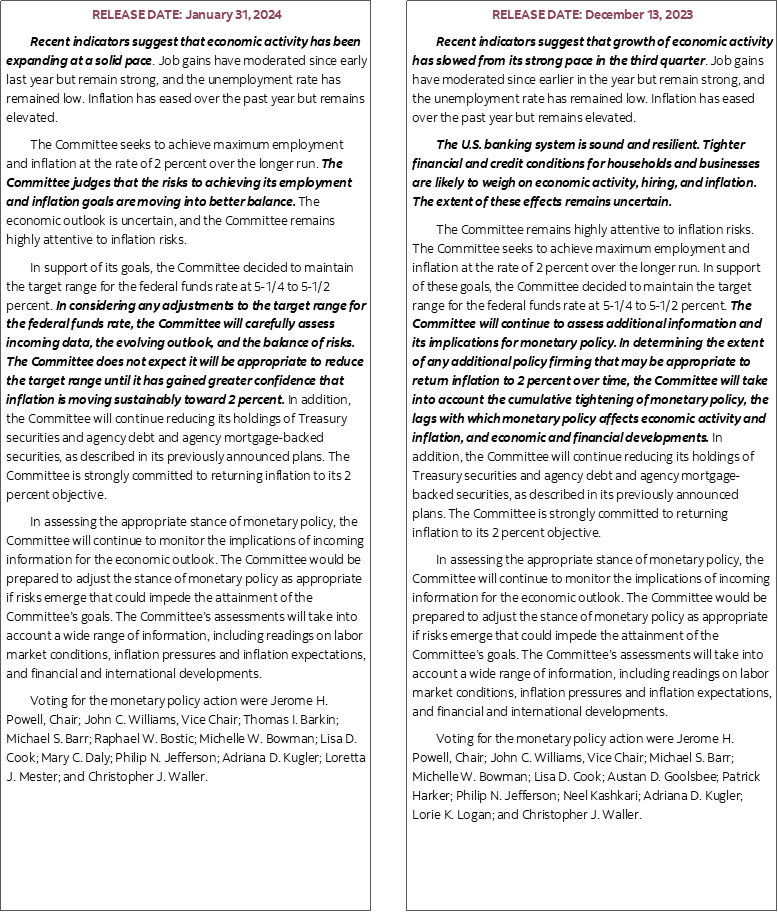

Please see the accompanying statement comparison at the back of this note for changes that were made to this statement relative to the prior one on December 13th. There were more changes than anticipated.

The growth reference in the opening sentence was upgraded from 'slowed' to 'a solid pace' which is roughly what was expected.

The second paragraph was a total re-write. It eliminated reference to the banking system, how tighter financial and credit conditions would weigh on economic activity, hiring and inflation with uncertain effects.

In place of that prior wording, they now reference how dual mandate risks are “moving into better balance.”

Key, however, were the changes to the third paragraph. They struck out reference to ‘any additional policy firming that may be appropriate’ and replaced it with “in considering any adjustments” while pushing back against nearer term easing by saying:

“The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.”

The decision was unanimous.

On balance, the statement made it fairly clear that it doesn't sound like they're in a rush to ease.

THE FED’S CONFIDENCE PROBLEM

The statement-codified need to have greater confidence is the key here. When asked point blank what it would take to give the Fed confidence to ease, Powell said this:

“We have confidence. We're looking for greater confidence. Implicitly our confidence has been gaining. We want to see more data, a continuation of the good inflation data. Is the 6 months of good inflation data a signal we're on a sustainable path toward achieving 2% sustainably? The data is low enough. But can we take it as sustainable, that's what we're talking about. We're looking for inflation to continue coming down as it has for the past six month.”

When probed further with the question being “Is there anything that makes you doubt that it will be sustainable?” Powell said:

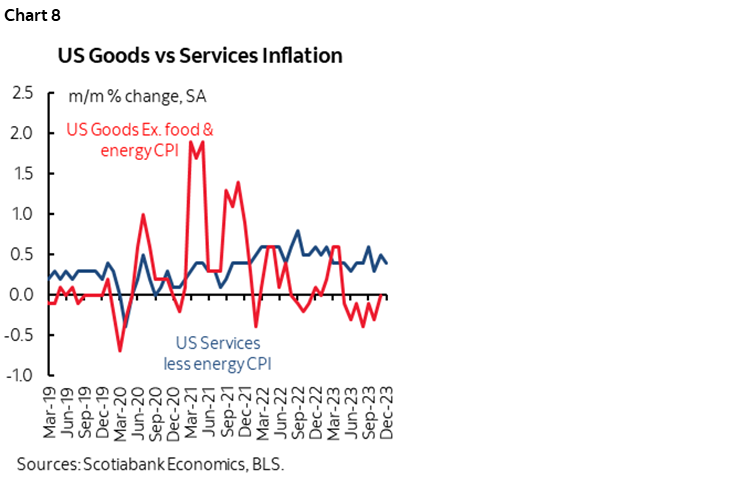

“It's a good story but we need more confidence. Over time, goods inflation will flatten out and so disinflation will require services inflation to contribute more.”

This last point is key. Powell returned to it more than once as a key uncertainty. Goods disinflation has been dragging down inflation while services inflation remains hot (chart 8). There are multiple scenarios going forward, but Powell is implicitly asking what if goods disinflation stalls and services inflation does not?

Powell also noted that "Ongoing progress in bringing it down is not assured" in reference to inflation.

Powell further responded with “No I wouldn’t say that” when asked if the goldilocks soft landing has been achieved. He said “Core inflation is still too high. We’re not declaring victory at this point. We still have a ways to go.”

The Chair also noted that this key quote:

“The greater risk is that inflation stabilizes at a level above 2% rather than accelerates. We would have to respond if inflation moves back up again and both of those scenarios are risks. You've had 6 very good months for inflation but are the last six months durable?”

On the other hand, Powell sounded worried that ultimately the picture could rapidly shift toward exposing greater vulnerabilities. He said this in the context of dismissing worries about rapid economic growth challenging achievement of the dual mandate:

“A lot of this disinflation has come through healing of supply chains. Relative to the neutral rate we can't identify with precision how tight policy is. The supply side has been recovering in the middle of this. A lot of the growth we are seeing is driven by easing supply chains and labour markets and when that wanes, we'll see more of the tightening effects.”

The Fed’s confidence problem also extends to the other part of its dual mandate. When asked whether the labour market is back to normal, Powell said:

“The labour market by many measures is at or nearing normal but not totally back to normal. Job openings and wage increases are not totally back to where they were. The economy is broadly normalizing. Wage setting will take a couple of years to get all of the way back [to pre-pandemic].”

Powell also responded affirmatively in response to whether the FOMC will be watching CPI revisions on February 9th and duly noted that “Last year was a surprise” and not a good one.

NO MECHANICAL RULES PLEASE!

Powell was asked why they wouldn’t be easing as a Taylor Rule would indicate given expectations for falling inflation. Powell responded by saying:

“We consult a number of Taylor rules but we've never been in a place where we've made policy on the basis of the Taylor rule. If real rates go up as inflation comes down we cannot mechanically adjust the policy rate because we look at more than just the fed funds rate and we don't know where the neutral rate of interest is at any given time but we also can't wait until the economy turns down. We're in a risk management framework trading off the risk of too early and too late but the timing requires confidence toward sustainable 2% inflation.”

Powell might have also said that easing in anticipation of falling future inflation is a tad farcical given how poorly models and central banks forecast inflation throughout the whole pandemic era (and before...). If you ease because you expect durably cooler inflation but you know everyone sucks at forecasting inflation, then why would you ease on this basis? Powell’s been around long enough to know the answer.

RISK TO THE OTHER HALF OF THE DUAL MANDATE

When asked whether a weaker employment picture would motivate easing, Powell basically said yes:

“We're not looking for that. If we saw an unexpected weakening in the labour market that would certainly weigh in favour of cutting sooner. If inflation is stickier that would support cutting later. In the base case, the SEP shows we think we can and should be careful about when to begin to dial back.”

Onto Friday payrolls next!

UNANSWERED QUESTIONS

I’m a bit surprised that no one in the press conference asked why the FOMC removed the comments in the statement about how the banking system is sound and resilient and the reference to tighter financial and credit conditions that are likely to weigh on economic activity, hiring and inflation and how the effects are uncertain. Are they less concerned about these factors?

The statement referenced “any adjustments to the target range”' instead of “any additional policy firming” in the prior statement. That sounds ambiguous in a way that leaves tightening and easing on the table, yet Powell said during his presser that "We believe that the policy rate is at its peak" and that "dialing back" will become appropriate at some point this year. That’s not new; in fact the dot plot has shown 2024 easing for years now and Powell said it again at the December press conference.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.