- Q4 GDP of 1.7% offers a soft transition to 2023Q1

- It’s a baby step toward evaluating 2023 with the BoC on pause

- Canadian GDP, m/m % change, November, SA:

- Actual: 0.1

- Scotia: 0.2

- Consensus: 0.1

- Prior: 0.1

- December guidance: “essentially unchanged” (ie: likely –0.1% to +0.1% m/m SA)

Canada’s economy remains in a deep state of excess demand that may be very tentatively shifting toward opening up some slack. Having said that, we need to treat this possibility with a high degree of care. Consensus has felt this way toward Canada over prior quarters and thus far Canada’s economy has consistently outperformed such expectations.

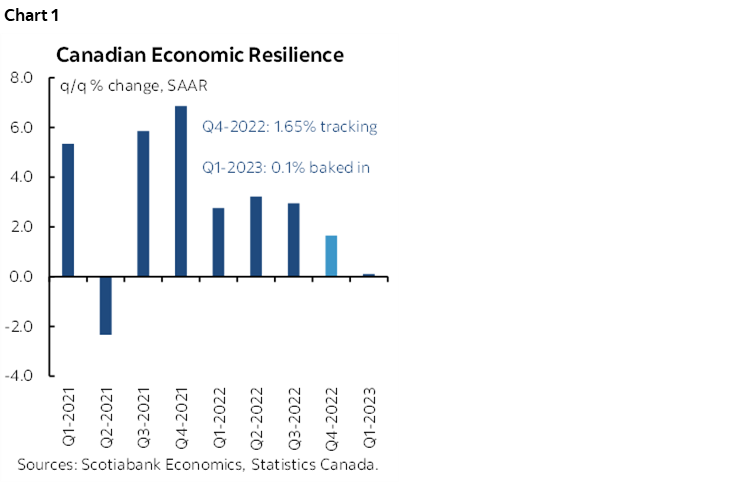

The economy remains in excess demand because Q4 GDP growth landed at 1.65% q/q at a seasonally adjusted and annualized rate using the monthly production-based GDP accounts. That kind of growth is broadly in line with guesstimates of the ability of the supply side to grow around a comparable rate and continues to illustrate trend resilience (chart 1). As production grows in line with the supply side’s ability to feed it and neither more nor less than that the result is that Canada’s economy has moved sideways in terms of capacity constraints on the Canadian economy. Canada needs to have a protracted period of economic growth undershooting potential GDP growth in order to open up slack in the economy and exert sustained downward pressure upon inflation. To date, we cannot say that is happening.

Will it into 2023? Probably, but this will only be informed by what actually data and we have nothing to go by thus far. All we can say to this point is that the way in which 2022 ended bakes in neither upside or downside momentum into the first quarter. There is no growth ‘baked in’ to Q1 GDP which means tracking Q1 GDP is now fully a matter of tracking evolving data to determine whether it will be an up or down quarter for overall activity in the economy.

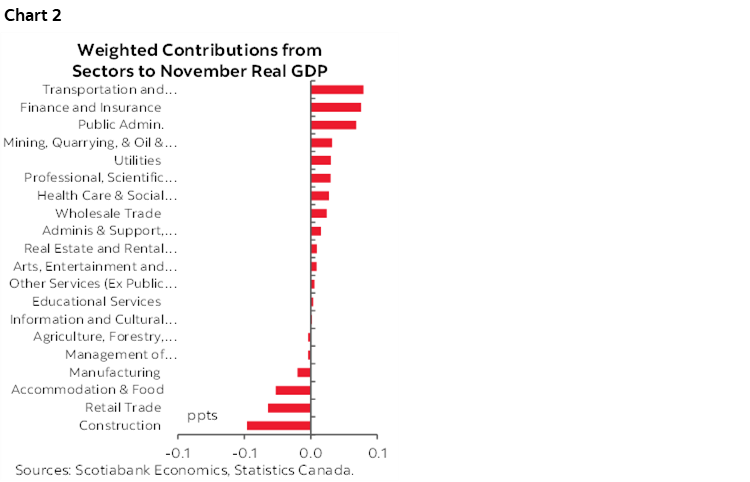

This tracking is informed by the fact that November GDP was up by 0.1% m/m and December was reported as “essentially unchanged” by Statcan. That’s their code language for basically anything from -0.1% m/m to +0.1% in December. Weighted contributions by sector are shown in chart 2. So if Q4 averaged growth of 1.65% and ended as guided then the math points toward a loss of momentum. We’ll inform the up or down risks to this loose guidance as December goods sector data arrives and as Statcan more fully incorporates service sector performance.

The Bank of Canada would not view this batch of estimates as offering any new information to their refreshed forecasts from last week (MPR here). In it they had forecast Q4 growth of 1.3% q/q SAAR using expenditure-based GDP. Expenditure-based GDP growth can deviate from this morning’s production-based GDP accounts. Production-based GDP does not take into account how higher output was achieved (e.g. more or less use of imported content) and where it went (ie: higher or lower inventories). Expenditure-based GDP does take account of such factors and so next week’s trade figures will help to inform tracking of the BoC’s forecasts and so will more complete inventory data.

For now, we’ve only taken a small baby step on the path toward evaluating the economy’s performance with the central bank on pause as it does so.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.