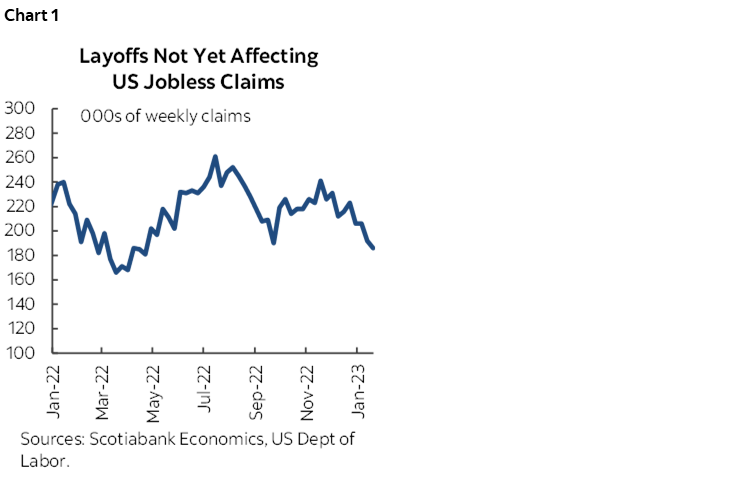

- Jobless claims remain very low…

- ..as perhaps layoffs are being offset by reabsorption, job growth elsewhere

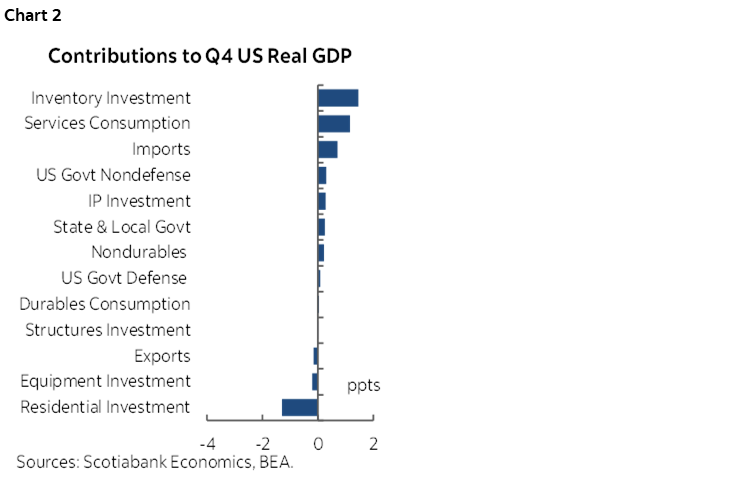

- US GDP growth beat estimates on mixed details

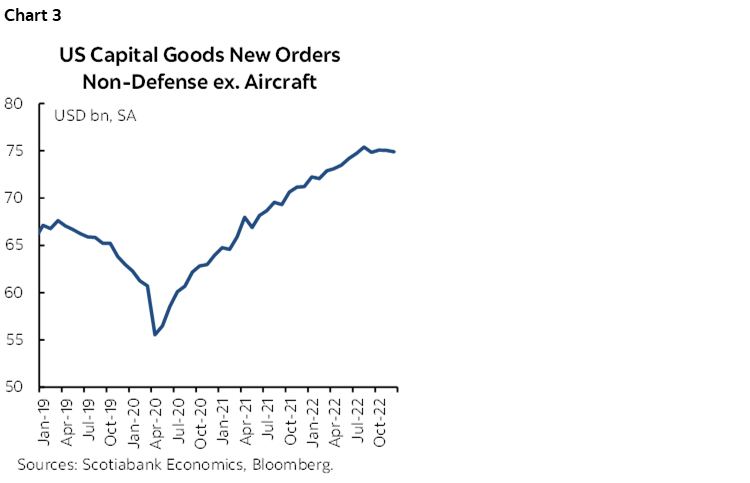

- US core cap-ex has plateaued…

- ...as this supply side measure has stopped expanding

Pick what you wish out of a grab bag of US macro reports this morning. Shorter-term US Treasuries slightly cheapened in the aftermath probably on the ongoing signs of strength in the job market.

Weekly initial jobless claims continue to run at very low levels despite layoff headlines (chart 1). At 186k last week they are at the lowest since last April and averaging just under 200k on a 4-week moving average basis. No states estimated their numbers this time (not even California) and so we can't really dent the quality of the low number on that basis now.

So what’s going on? Either there are lagging effects for when pink slips start showing up in jobless claims and/or layoffs are being offset by strength elsewhere. That could either be due to layoffs being reabsorbed into job vacancies and/or due to enough job creation elsewhere. This is a bullish signal into next week’s nonfarm payrolls but bad for folks who would prefer Powell to get weak knees.

US GDP growth surpassed consensus expectations (2.9% q/q SAAR, consensus 2.6%, Scotia 2.8%) following 3.2% growth in Q3. Yet again consensus was too bearish for too long in a repeat of what happened into Q3 GDP but I’m sure some folks will find a way to dump on the numbers regardless.

GDP details were mixed. Chart 2 shows the weighted contributions to GDP growth in Q4. Be careful toward the inventories contribution as perhaps stocks were depleted too rapidly when inventories dragged on Q2 and Q3 GDP growth. Consumption was up 2.1% q/q SAAR and added 1.4 ppts to GDP growth in weighted terms which was a little lighter than expected and may indicate a soft December reading tomorrow. Trade added 0.6 ppts to GDP growth entirely due to less of an import leakage effect as exports were a small drag. Fixed investment subtracted 1.2 ppts from growth due to residential (-1.3 ppts weighted drag) with nonres investment flat (+0.1 ppts weighted). Government spending added 0.6 ppts due to all levels contributing.

Durable goods orders soared by 5.6% m/m SA primarily due to a surge in plane orders. Core cap-ex (excluding planes and defence) slipped by 0.2% m/m. Chart 3 shows that the trend in cap-ex has flattened out. The debate on that involves whether it is sensible because the economy may fare much worse than expected and for longer, or whether the supply side has stopped growing and we'll pay the price for that through inflation risk into a potential demand rebound at some point.

And I don't see anything in the core PCE figures that is surprising into tomorrow's December readings. 3.9% q/q on the screws. Cooler, but so not cool.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.