- The BoC held its policy rate unchanged while guiding future tightening

- We lost today’s battle, but BoC guidance suggests were on the right side of the war

- The BoC’s forward rate guidance tool is unreliable

- BoC will fall further behind inflation and amplify housing imbalances

The Bank of Canada passed on a rate hike today against our expectations that we had pegged at better than even odds and with congratulations to the shops that got the battle right even if not the reasons. If the BoC nevertheless follows through and translates the material shift in policy guidance that they provided today into concrete action, then our more hawkish than consensus forecast may yet win the battle as consensus might have misjudged the path from here.

That nevertheless remains to be seen not only given the course of developments to come, but also significantly because of the apparent unreliability of BoC forward rate guidance. It also remains apparent that the central bank has retained an ongoing run-hot bias toward inflation and house prices as it is far behind the appropriate stance of monetary policy for this point in the cycle.

Please see the accompanying statement comparison, the Monetary Policy Report (here) and Governor Macklem’s opening remarks to his press conference (here).

As a consequence to today’s rate hold and because a hike was mostly priced, financial conditions eased through lowering market-driven borrowing costs and a mild depreciation in the C$ that pared half of its post-statement weakening as the press conference unfolded. With inflation ripping and housing demand soaring the BoC actually eased financial conditions today and into the Spring mortgage pipeline. The BoC describes conditions as having tightened by referencing the rise in nominal bond yields but did not acknowledge that the more relevant real borrowing rates have plunged.

WHAT THEY DID

There were seven main developments:

1. First, the policy rate was unchanged at 0.25%.

2. Second, forward rate guidance was hawkish toward future steps and the pace of adjustments especially during the press conference during which Macklem said the following:

“Everybody should expect interest rates to be on a rising path.”

“We've been very clear that we are announcing a significant shift in policy and to expect a rising rate path and the time for emergency policy is gone. “

“We all agreed it was paramount to take action today to take steps to avoid higher inflation expectations in the nearer term from migrating into the longer-term.”

“When we say 'a path' it does not mean one move, it means a number of steps. “

“There needs to be a series of steps. As we get further down that path the decisions will become more finely balanced and more data dependent.”

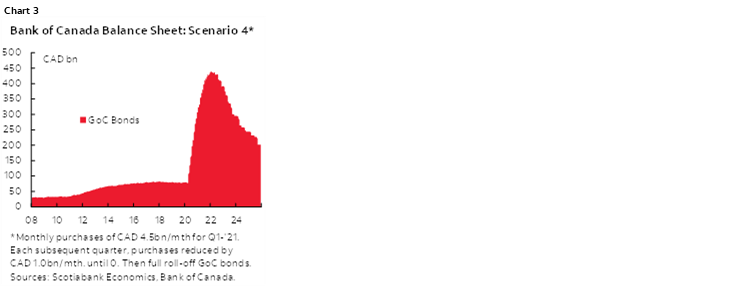

3. Third, On balance sheet guidance, Governor Macklem said that the BoC will hold GoC bond holdings constant “at least until it begins to raise the policy interest rate” at which point they will consider allowing roll-off. That is unchanged. The Governor’s remark on reinvestment plans during the press conference seemed to intimate they would lean more toward gradually reducing reinvestment flows rather than going cold turkey which matches the scenario outlined in chart 3. Macklem guided that the BoC is not considering asset sales with the qualifier being “at this point.”

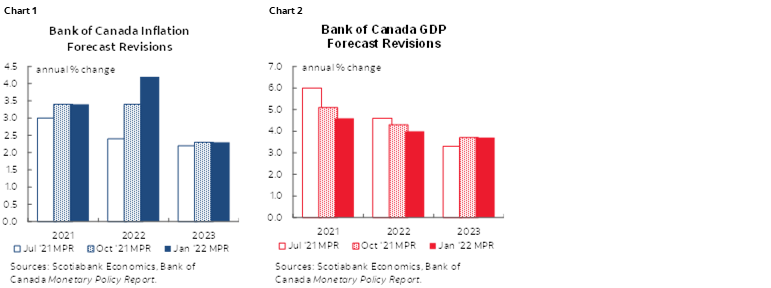

4. Fourth, the BoC upgraded its forecasts for growth and inflation. At 4% GDP growth this year and 3.5% next year they even have a slightly stronger growth profile than we do (3.7%, 3.3%).

5. At the same time, the BoC upgraded its inflation forecast to 4.2% this year and 2.3% in 2023 to show a sustained overshoot of its 2% inflation target throughout the projection horizon. The BoC is hedging its bets between the verbiage that says inflation is transitory versus the numbers that say not so much relative to the 2% target. Then again, its inflation forecasts have performed poorly to date.

6. The BoC even finally acknowledged that “wage gains are picking up.”

7. Potential GDP growth assumptions were left unchanged at “about 1.6%” per year over 2021–23. As a consequence to the combined forecasts for potential and actual GDP growth and where it judges the starting point for the supply side of the economy, the BoC now says that “Governing Council judges that overall slack in the economy is absorbed.”

So far we’re pretty happy. Strong growth? Check. Hot sustained inflation? Check. Wages accelerating? Check. Slack gone? Check.

So they hiked, right? Nope.

THE BoC’S FORWARD GUIDANCE PROBLEM

The rub here lies in the fact that everything in today’s BoC narrative said hike and the ducks lined up very well relative to our assessments and expectations for the drivers of the decision, but they still passed on the opportunity to do so.

The prime reason? Governor Macklem strongly violated his own longstanding prior forward guidance that said they would hike when spare capacity shuts. Today the BoC said it is shut right now, but they held the policy rate unchanged anyway and guided that a rate hike will now lag this development.

Had they said spare capacity won’t shut until, say, Q2 or repeated the guidance it will happen in the “middle quarters” of 2022 then we could have debated that, but it would have been more consistent with holding the rate unchanged today. I must have missed the speech when it was said that the policy rate would rise after the closure of spare capacity because the last speech I read from the Governor dropped all reference to its former forward rate guidance which if unintended was a huge oversight. The BoC had been following a fairly methodical approach to exiting its GBPP program, but slipped up today in terms of actioning its prior forward rate guidance.

What further complicates things is the guidance that the BoC will be very data dependent into each decision. That makes a March hike less than automatic. In fact, will they hike if January jobs tank as seems likely and even if it’s transitory? The messaging around doing so as temporarily weak data is likely to be rolling in may be more awkward than had they just hiked today.

So why did the BoC do that? It’s possible the BoC wanted to send a message that it won’t be pushed by markets, but I’d hope that wasn’t the case... Governor Macklem emphasized that they “are mindful” toward the effects of omicron which seemed to figure prominently in the decision to pass today, despite the fact he said they are looking through it as a transitory shock. Despite the fact that housing is ripping. Despite the fact that properly measured inflation is tripling the BoC’s 2% target. Despite the fact that slack is gone.

IMPLICATIONS

What I think the main implication is for the short-term is that the BoC will allow the Spring housing market to rip again in perhaps one last big surge before its signals suggest that it could begin rapid rate hikes thereafter if such guidance is to be trusted. Great. House prices will rip again and then hit borrowers with higher rates instead of acting a bit more pre-emptively. Low interest rates are clearly exacerbating underlying supply-demand imbalances in the housing market. During the press conference, SDG Rogers pinned the housing challenges on the supply side but low interest rates are making this worse! The BoC seems to be dramatically downplaying the role of easy money as a contributor to hot housing markets which I find to be an untenable position and one that raises risks further out in our forecast horizon.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.