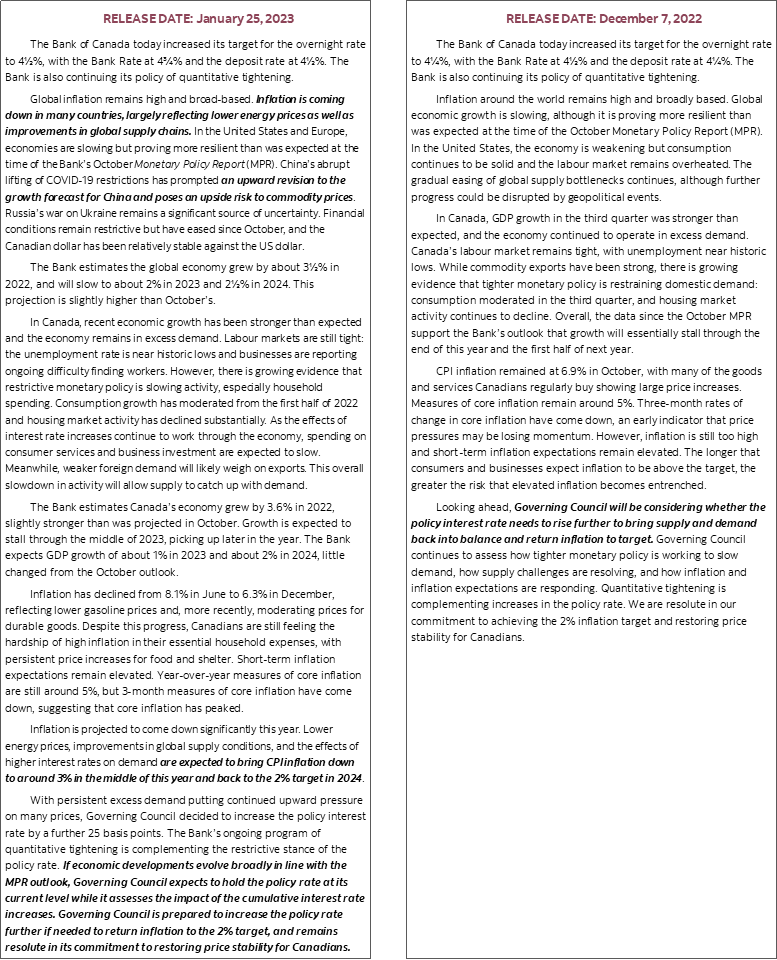

- BoC hiked 25bps and signalled a pause

- Why financial conditions eased further

- What could go wrong

- Bank of Canada overnight policy rate (%):

- Actual: 4.5%

- Scotia: 4.5%

- Consensus: 4.5%

Governor Macklem threw a strike and promptly headed to the dug out for what may only prove to be a rain delay in the fight against inflation.

In hiking 25bps with fairly strong pause language and only soft pushback against rate cut pricing his decisions motivated a further easing of financial conditions broadly in keeping with my base case scenario going into the decision. Whether they are done or not depends critically upon the accuracy of their inflation forecasts over time and how labour and housing markets contribute to such views.

Please see the statement here, the statement comparison at the back of this publication, the MPR here, and the Governor’s opening statement to his press conference here. The first-ever minutes to this meeting will land on February 8th and Governor Macklem promised “more insight into our decision making” at that time.

MARKET REACTION

It’s not the worst outcome that would have been a total whiff and dovish pause that would have prematurely rung the all clear bell on inflation risk. But it’s a close second. In driving a further easing of financial conditions today, I think the BoC has taken another micro step toward amplifying upside risk to housing, growth and inflation into 2024 and beyond that point which may frustrate their attempts to get inflation durably under control across the full cycle of what lies ahead.

In calling time-out on hikes, they are placing emphasis upon the lagging effects of tightening into this year when the ship has sailed on that outcome; they are paying little to no heed to the lagging effects of market easing into next year and putting a lot of stock in their ability to forecast waning inflation. Uh oh.

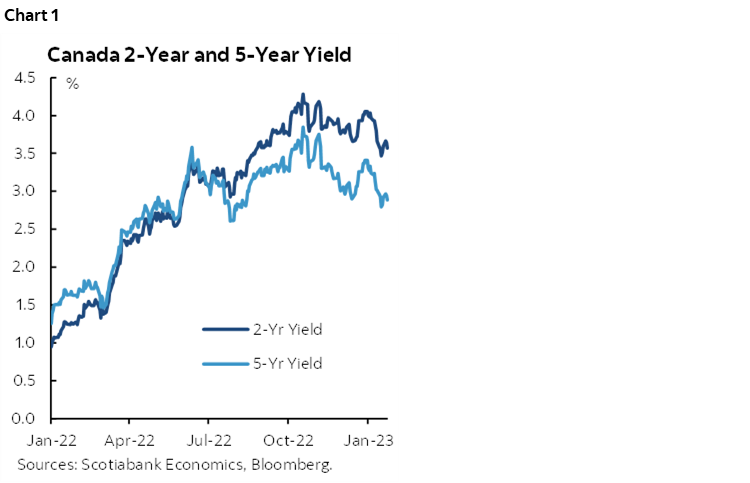

Witness chart 1 that shows the Canada fiver that’s back to being about a full percentage point lower than October’s peak with another nickel subtracted from the yield today. Or witness the 8bps rally in 2s on the day that is now about 75bps lower than the October peak. Market participants were rewarded by positioning toward a rally on the combined policy rate decision and the bias.

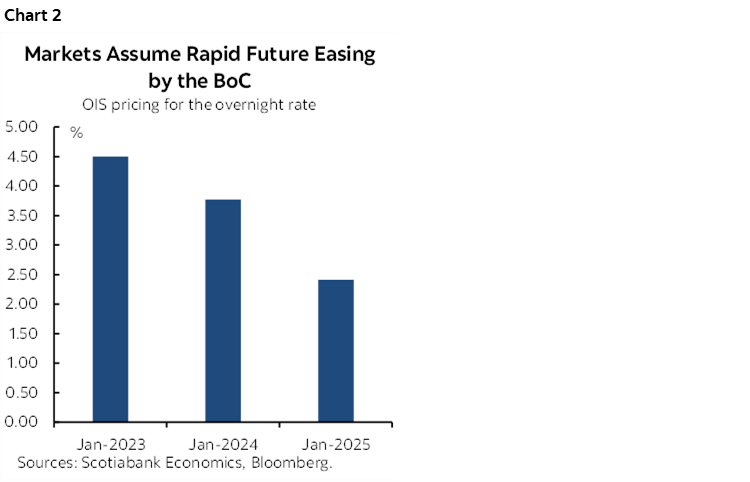

Markets are pricing significant rate cuts starting later this year and throughout 2024 such that by the end of next year they foresee getting back toward a neutral stance (chart 2).

And it’s probably not over yet. I think we’ll see a further fixed rate rally in Canada into the Spring housing market based upon a) the likelihood the BoC stays on the sidelines for a long while yet, and b) the debt ceiling dysfunction in Congress that will likely drive increased flow into fixed income markets spilling over into Canada over the months ahead.

Key to understanding the market reaction is to walk through the salient aspects of the BoC’s communications including core messages drawn from the press conference.

A MATERIAL BIAS SHIFT

The final paragraph to the statement is key to understanding the pause signal. In December, they teed up a coming pause by saying they “will be considering whether the policy interest rate needs to rise further.” They now say:

“If economic developments evolve broadly in line with the MPR outlook, Governing Council expects to hold the policy rate at its current level while it assesses the impact of the cumulative interest rate increases. Governing Council is prepared to increase the policy rate further if needed to return inflation to the 2% target, and remains resolute in its commitment to restoring price stability for Canadians.”

That may be taken as setting a high bar for any further rate hikes in future and only if conditions evaluated over a significant period of time materially surprise to the upside. Other comments delivered in the press conference reinforce this interpretation and will be covered below.

Before doing so, also note that Macklem was asked if he was still concerned about the risk of under tightening as he has previously emphasized. His answer suggested his concern has eased and he’s more balanced in his opinion now which further adds to the evidence of a materially more dovish bias shift:

"We are trying to balance the risks of under- and over-tightening. If we do too little, the decline in inflation will stall before we get back to target. But if we do too much, we will make the adjustment unnecessarily painful and undershoot the inflation target."

and

“This is a conditional pause. Conditional upon developments relative to our forecasts. If upside risks materialize through an accumulation of evidence that inflation is not coming down, then we are prepared to raise again.”

That’s a whole lot less conviction than saying that you’re still worried more about doing too little and I think this is part of what markets seized upon. How did your worry about doing too little really materially change toward being more balanced after only a lousy additional quarter point hike? There is something deeper going on here as covered below across multiple observations.

A LENGTHY PAUSE AND A HIGH BAR SET AGAINST HIKING AGAIN

The market reaction also latched onto guidance toward the length of a pause. When Governor Macklem was asked what he would need to see in order to hike rates again, his answer intimated that they would be on a rather lengthy pause before reassessing. He did so by saying the following:

“We are looking for an accumulation of evidence. Not one piece of evidence. We are already seeing the effects of higher rates slowing demand in interest sensitive sectors. We expect that to feed through to service prices. We will be looking to see if inflation expectations come down and inflation itself is coming down.”

That says to me that we’ll be looking at many months or quarters of multiple rounds of information on the economy, job market, inflation, and external developments before they look back at an accumulation of a material amount of evidence and decide what’s best later.

PUSH BACK AGAINST RATE CUT PRICING COULD HAVE BEEN STRONGER

Markets also heard only a soft pushback against rate cut pricing and that egged them on a bit more. When asked what he thinks about markets that are pricing aggressive rate cuts starting later this year into 2024 and the parameters that would guide him to ease, the Governor wasn’t strong enough in my view and that’s part of why financial conditions eased further today:

“Let's keep in mind inflation is still over 6%. It's far too early to be talking about cuts. We’re talking about a pause which is about assessing whether we have done enough to rein in inflation. The pause is designed to give us time to assess if we have hiked enough.”

When Macklem was asked about what parameters might motivate future rate cuts, he answered by saying “It's way too early to talk about that. We're talking about a pause which is about assessing whether we have done enough to rein in inflation.” If you really don’t like rate cut pricing, then why not a reverse conditional commitment not to cut this year unless you’re really blown away?

MACKLEM DODGED QUESTIONS ON FINANCIAL CONDITIONS

If the Governor really wanted to balance the risks of over- and under-tightening then he might have leaned more strongly against easing financial conditions.

Yet when given the opportunity to comment on how he views easing financial conditions, Governor Macklem answered like a real economy central banker versus how a markets person might have. He did not acknowledge the broad easing of financial conditions and just pointed to the BoC’s administered rate hikes. It’s possible he either missed the point of the question—or perhaps chose to miss it versus a bun fight with markets.

I think that if the Governor were really uneasy toward easing financial conditions then he might have sounded more aggressive on this point. The fact that he did not added to the sense of a bias shift.

THE BANK OF CANADA IS RELYING UPON ITS INFLATION FORECASTS

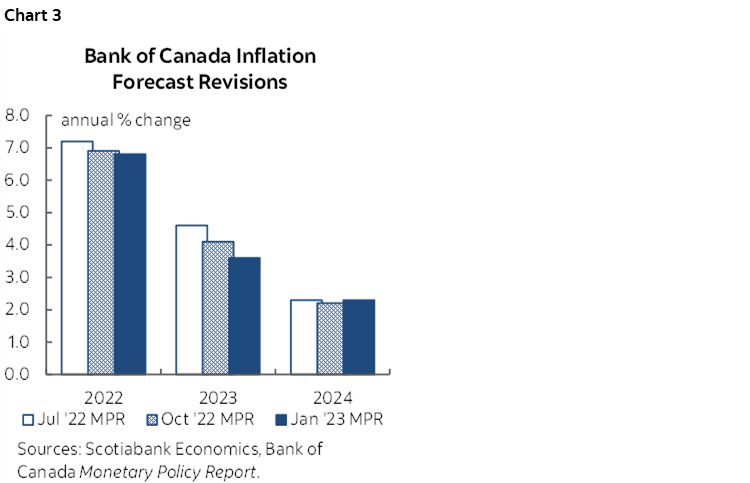

So what gives the BoC such a sense that it has probably done enough? The communications point to two main arguments. One is the significance they attach to nascent evidence that core inflation has softened, but is not yet soft. Two is that they think inflation will rapidly ebb as shown in chart 3.

Paint me worried. Central bankers please do not look at Medusa’s locks in chart 4, but call me nervous that the BoC’s policy bias hangs on its ability to forecast inflation! The BoC keeps pushing out its model-based forecast collapse of inflation; maybe one day they’ll get it right.

In general, I thought the Governor was overly confident that inflation was coming down and would continue to do so durably. When asked about his degree of confidence, he said:

“We are seeing evidence that higher rates are working. Interest-sensitive parts of the economy are starting to show this. We have also had more favourable developments with global supply chains faster than we were expecting. Shorter-term measures of inflation like 3 month moving averages are cooling. Finally we now have a cumulative 425bps of hikes into restrictive territory and we know there are lagging effects.”

LABOUR MARKETS COULD MOTIVATE A RETURN TO HIKING...

Pivoting away from reasons to call it quits on hikes, what could instead motivate the BoC to reset the narrative back toward hiking again later if its present views prove to be too sanguine?

Macklem was asked point blank whether failure to see declining employment would drive him to resume tightening given the implications for inflation and he answered in the affirmative:

“If the labour market remains really tight and that continues to put upward pressure on prices then that is something we'll have to take into account. You'll see that in service prices. We're seeing goods inflation come down. But we need service price inflation to come down.”

That’s not just one job report they’ll be watching, but a whole series of them in order to evaluate the degree to which the labour market remains very, very tight.

...AND SO COULD WAGE-PRICE SPIRAL CONCERNS

An offshoot of labour market tightness is wage growth which is where the labour market links to inflation. Macklem was asked how he now views the risk of a wage-price spiral and emphasized that wage growth is one of the conditions they are closely watching to determine whether they have done enough.

“Labour markets are very tight. This is a symptom of an overheating economy. Part of rebalancing supply and demand is cooling the labour market which we expect will happen. On wage-price spiral concerns, we think this has diminished with wage growth at 4–5% and our surveys of inflation expectations suggest fewer people expect inflation to remain high for a long time. If wages at 4–5% were to be sustained, then unless there is a surprisingly strong acceleration in productivity that's not consistent with getting inflation back to target.”

I think he’s overstating improvement in survey-based measures of inflation. In fact, I’m not even terribly sure the BoC’s own surveys say nobody believes they’ll achieve their inflation target (recall here). Nevertheless, watch the wage data very closely over coming months and quarters.

HOUSING UPSIDE—AND HOW IT COULD BE EVEN GREATER THAN THE BOC THINKS

The BoC wishes to send the signal it won’t be surprised by future stabilization of housing but they still might not have gone far enough in my view and that could explain a part of why they think they’ve hiked enough.

When asked about the outlook for housing, SDG Rogers answered by saying the following:

“The housing market is evolving broadly in line with our expectations. There are some fundamentals that we do expect to bring a pick-up later in the year, like immigration and lower mortgage rates. That may drive a rebound, but we do think the housing market has a little bit further downside.

This is similar to arguments I’ve given but not quite as aggressive. We should leave the door open to a potentially better Spring housing market and could be faced with another strong rebound over 2024–25.

In fact, I continue to argue against the consensus narrative that Canada is hooped because it has so much greater sensitivity to household debt and housing markets than, say, the US. That remains a grossly exaggerated argument. One problem with this view is that it slaps on horse blinders toward everything else going on in Canada by way of risk mitigants, like the terms of trade and commodities, like free spending governments into another round of budgets, like very strong nonfinancial corporate balance sheets, and like incredibly strong job markets that might be more resilient than some fear.

Another reason is that OSFI’s B20 mortgage stress test took out much of the rate sensitivity in Canadian housing. For years now, new borrowers have had to qualify at the higher of either the contract rate plus 2% or 5.25% (up from 5% in mid-2021). That did not eliminate rate sensitivity by any stretch, but it made the sensitivities far less than argued by folks who advance the worse-this-time narrative while never even mentioning B20. It was Canada’s first housing correction in response to a rate shock and it reset the market years ago from which it subsequently recovered. I see no reason why that can’t happen again.

Another reason is that housing faces supports that could easily offset what is a modest mortgage rate shock relative to B20. Like depleted new home inventories. Like the listings strike still holding the resale months’ supply measure below its long-term average. Like first time homebuyers amassing bigger down payments to capitalize upon cheaper house prices. Like surging immigration with nowhere as yet to put them all. Like resilient job markets. And like easing financial conditions and implications for mortgage rates.

RECESSION?

What balances some of the risks facing the BoC’s stance is what ultimately happens to the economy. On that, they are walking down the middle of the road. When asked what he thinks about the risk of recession, Macklem had this to say which is generally consistent with our narrative on GDP growth forecasts:

“We project basically no growth. We do need this period of no growth to allow supply to catch up. It's not painless. It's just as likely that we'll have slightly negative growth as having slightly positive growth around our basically flat projection but we don't expect a major contraction.”

THE BANK’S LOSSES

As a technical aside, Governor Macklem came well prepared for a question about the losses the BoC is incurring due to quantitative tightening and whether they are closer to striking an agreement with the Federal Government on how to address this. Macklem’s full quote is as follows:

“Our losses are temporary. Normally the Bank of Canada makes positive net earnings. Through the first parts of the pandemic with QE we remitted higher income to the government. Interest we're now paying on settlement balances means our net interest income has turned negative. That has resulted in our net income turning negative for the first time and there will be a period of a good couple of years of negative income before our income reverts back to its normal positive state. In our current legislation we cannot offset losses with retained earnings; we remit all of them to the government. Further, all central banks are going through this. The Bank of Canada and the Department of Finance are discussing solutions and the Minister of Finance has told us that in future they will allow the Bank of Canada to retain earnings on a temporary basis rather than remit them to the government until positive equity is restored.”

Excellent answer. Some folks forget the BoC was a money maker earlier in the pandemic when rates were low and it jumped into illiquid asset markets. A central bank has to be free to operate monetary policy as it sees fit over the full cycle.

Please also see the attached statement comparison.

Governor Macklem speaks on February 7th, one day before minutes to this meeting will arrive.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.