- BoC communications drive bond yields higher, CAD appreciation

- BoC upgraded growth forecasts, lowered its assessment of uncertainty

- A “micro-cut” was rejected

- Markets are put on watch for timing the next taper

- The BoC may be underestimating consumer strength

- BoC monitoring CAD strength, but not sounding too concerned

- 2022 is still a decent bet for rate hikes

The first step toward eventually reducing stimulus is to know when you’ve probably done enough. The BoC signalled this awareness today.

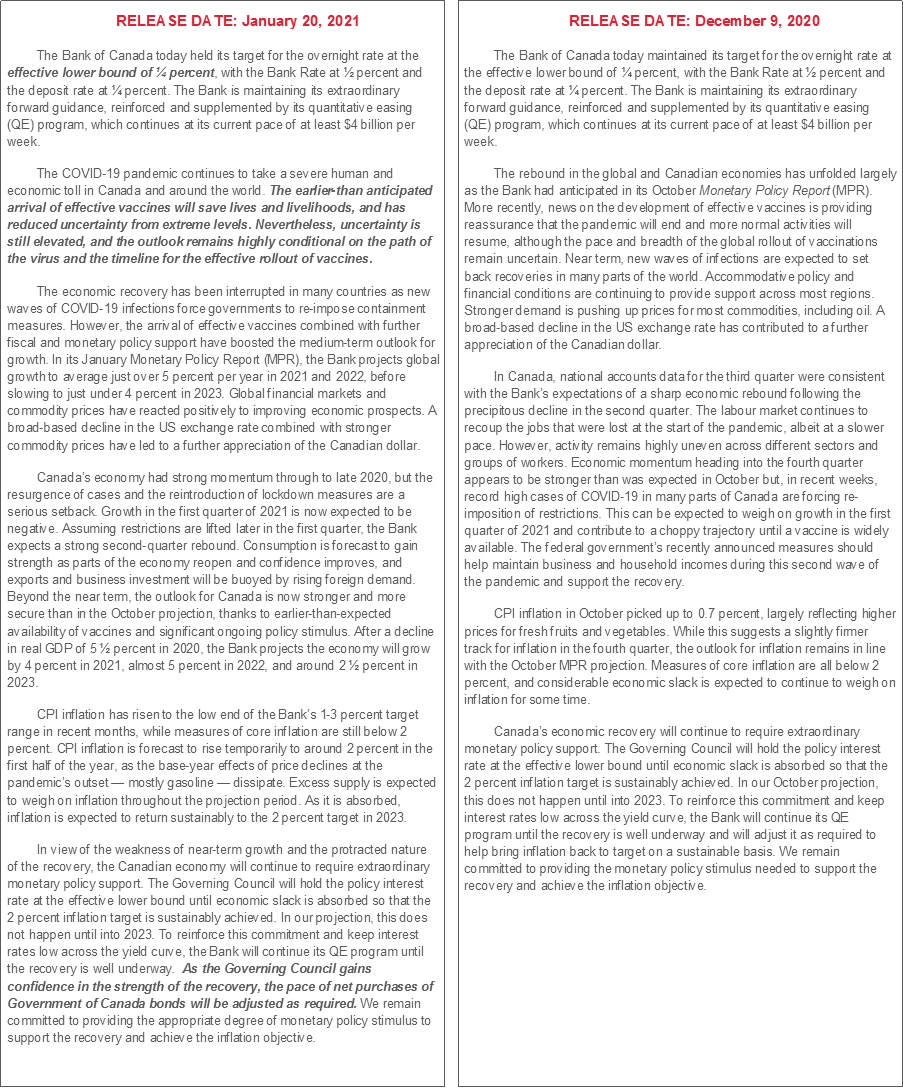

Guidance to fade talk of a micro rate cut worked out well and so did guidance that the BoC would take a small step in the direction of taper talk as the Bank of Canada struck a generally more upbeat tone. The statement is here, the Monetary Policy Report is here and Governor Macklem’s opening remarks to the press conference are here while his comments during the Q&A will be represented below. Macklem deserved high marks for staying on script with a polished and consistent narrative throughout the full suite of communications during a difficult potential transition point for the central bank.

In response to the Bank of Canada’s overall suite of communications, Canada’s government bond yields increased by about 2bps across the curve today as US Treasury yields fell slightly. FX markets signalled the same interpretation as the Canadian dollar became the day’s star pupil through a half cent appreciation versus the USD after reining in a somewhat stronger initial response.

SAYONARA, MICRO CUT

I thought the main takeaway was delivered in the press conference when Governor Macklem basically ruled out a so-called micro rate cut (<0.25% while keeping the policy rate above zero) for non-fundamental reasons. Recall that the issue here is how market-based measures of the Bank of Canada’s policy rate have been below the policy rate itself which motivated some to argue they may as well take the policy rate down to validate what markets are signalling (chart 1). That’s often a slippery slope.

Macklem was rather clear in saying that only fundamentals-related reasons would motivate policy easing and not technical considerations that are driving short-rates lower. Among the technical considerations is that the collapse in Treasury bills outstanding (chart 2 shows the BoC’s holdings) has occurred alongside ongoing liquidity provisions by the central bank that have driven short-term paper prices higher and yields lower. This has occurred for reasons not related to the outlook for the economy and inflation. Macklem’s full quote to this effect is as follows:

“Markets are working very well. We're not focused on issues around market functioning. We're very focused on the amount of stimulus needed to get us back to target. In that vein, reducing the effective lower bound to a lower but still positive value perhaps in combination with other tools would be used to provide more stimulus if needed. That's the way we see it as a monetary policy tool. Market turbulence is a different kind of discussion.”

He also explained that they feel the stance of monetary policy is appropriate at this juncture.

TAPER WHISPER

I wouldn’t quite call it taper talk yet, as opposed to more of a whisper in the market’s ear, but the intent was nevertheless rather clear.

The signal that the BoC is open to tapering the C$4 billion or more per week of Government of Canada bond purchases conditional upon the evolution of its forecasts was delivered in the second last sentence of the statement and the Governor’s opening remarks to kick off the press conference. The quotes below indicate that if they see signs of their forecast recovery unfolding, then they are likely to take steps toward reducing the flow of purchases. What to monitor may include their assumption that restrictions will begin to be lifted next month, vaccine roll-outs and Q2 rebound evidence that could well drive the next taper decision as soon as this Spring.

“And as we gain confidence in the strength of the recovery, the pace of net purchases of Government of Canada bonds will be adjusted as required." [ed. “gain confidence” obviously would imply not expanding purchases, but rather in the opposite direction.]

"We agreed that if the economy turns out to be substantially weaker than we are projecting—leading to more disinflationary pressures—then we have options to add even more stimulus. And we are prepared to use these options as needed.”

“We also agreed that it is too early to consider slowing the pace of our purchases of Government of Canada bonds. However, if the economy and inflation play out broadly in line or stronger than we projected, then the amount of quantitative easing (QE) stimulus needed will diminish over time."

FORECAST UPGRADES

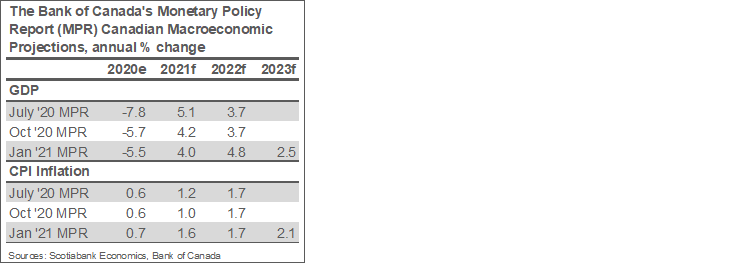

The BoC upgraded its forecasts (table 1 for Canada) and guided that “the arrival of effective vaccines combined with further fiscal and monetary policy support have boosted the medium-term outlook for growth." Macklem emphasized the heavy conditionality of their forecasts upon vaccine progress. It was a positive coincidence to see Pfizer announce earlier that trials on virus mutations have proven to be successful while the WHO announced that they may authorize the Astrazeneca COVID-19 vaccine either this month or next and is planning vaccine approvals for global roll-out.

- Canada’s economy is projected to grow by 4.0% this year (4.2% previously) but next year was revised up to 4.8% (3.7% prior) and 2023 is forecast to growth by 2.5%. All of these numbers are above the economy’s longer term non-inflationary speed limit.

- On the quarterly breakdown, the BoC projects that Canada’s economy will shrink by -2.5% q/q SAAR in Q1 after upgrading Q4 from +1% to 4.8%. This meets the expectation they would upgrade Q4 because we already know the data is tracking stronger for the quarter, but that some of the effects are offset by downgrading Q1 with the net level of GDP tracking not far off expectations. The central bank thinks COVID-19 restrictions will be lifted in February as a nearer term tracking risk (See Box 1, page 12 of the MPR).

- World growth was upgraded to 5.6% this year (4.8% previously), 4.6% in 2022 (4.3% previously) and the first attempt at forecasting 2023 pegs 3.9%.

- US GDP growth was upgraded to 5.0% in 2021 (3.1% prior), 3.9% next year (3.4% prior) and 2.0% in 2023.

Note that alongside its forecasts, the BoC also lowered the risks surrounding them. The direct quote was:

"The earlier-than-anticipated arrival of effective vaccines will save lives and livelihoods, and has reduced uncertainty from extreme levels. Nevertheless, uncertainty is still elevated, and the outlook remains highly conditional on the path of the virus and the timeline for the effective rollout of vaccines. "

Overall the suite of communications sets a very high bar against expectations for any further policy easing as we slip into tracking mode on their forecasts. They are saying they're on auto pilot for a time. Barring a shock out of left field, the next move is likely to tighten policy but even I think that's a 2022 story. As 2021 evolves, market rates through the front-end will more convincingly price such expectations alongside vaccine take-up and data.

IS THERE FURTHER UPSIDE TO THE BoC’S FORECASTS FOR CONSUMERS?

Notwithstanding the forecast upgrades, I think the BoC continues to underestimated how consumer spending will behave. They have not had a good track record at judging how retail sales and housing markets would respond to powerful stimulus to date. More fundamentally, however, I think the arguments offered today are debatable.

Macklem noted that the BoC is assuming most of the horded cash and high saving rates at households will not return as an even more powerful consumer spending surge than they forecast. I think that’s an area where they could be positively surprised. When asked during the press conference why he is assuming that households will not redeploy horded cash in the recovery, Macklem responded with a few points. One was that he thinks that most of the savings are in upper income households that are more likely to spend more of their money on high contact forms of spending with that past spending gone forever. He explained that they are more likely to travel or go to restaurants and that while they've substituted some of this away from high contact spending toward other things, you can’t unleash pent-up demand for services by, say, getting twice as many hair cuts to use his metaphor.

This is where I see it differently. First, it’s not just higher income households that have saved more. The BoC’s October edition of their consumer survey (chart 1–A here) showed that 20% of households earnings less than C$40k per year increased savings, 38% of households earnings $40–99k saved more and 47% of upper income households saved more. A first point is that there are many fewer households in upper-income categories than middle and lower income categories and so multiply these response rates by sheer numbers of people in those cohorts and you’d perhaps get a different picture of where the savings sit. Second, $99k as an upper income definition is a pretty modest one; does the BoC think that level of household income is ‘rich’ in cities like, say, Toronto or Vancouver and that folks in those markets if not elsewhere will just sit on their cash stockpiles? I think that assumption is, well, rather rich, to be cheeky about it. If so, then the BoC is overestimating the amount of savings across these “upper income” households that will continue to be horded.

Further, they don't have to release it such savings on services per se. They can spend it on buying more bigger ticket goods instead. Spending less on gas and transit, restaurants and travel or movie tickets may well mean more spent on a wide variety of other things, like, well, homes, autos, computers and gadgets, boats, atvs etc as we’ve seen. The operating assumption here is never to underestimate the capacity of consumers to spend.

Finally, the BoC is relying perhaps too strongly on survey-based evidence that portrays households as darling little angels who will diligently put all horded savings toward paying down debt. Such surveys are a waste of ink. They said the same thing about American consumers in the lead-up to the GFC and we know how that ended. Actions speak far louder than words when assessing the behaviour of consumers and the BoC is indicating that perhaps it hasn’t spent enough time on assessing the actions to date as retail sales soared to a record during the pandemic and took home sales with them. Hang onto low rates too low with vaccines arriving and I have a hunch we’ll see spending rip over time.

CAD BEING MONITORED, BUT NOT A WORRY YET

When asked about C$ strength and net positioning that continues to indicate net longs in CAD (chart 3), Macklem noted that their convention is to use the current spot exchange rate and that at about 78 CADUSD cents (1.28 USDCAD to market participants) the currency “dampens exports on the margin.” The BoC does this because of the perils associated with a central bank forecasting the currency and probably because of the difficulty in doing so to begin with. He went on to note that “the risk is that we see a further appreciation that will become more of a headwind as a downward risk to our projection. I would underline it's important to assess why the C$ is moving. We don't target CAD. Most of the appreciation of the C$ is because of depreciation in USD and so the C$ is becoming a factor in its own right in our projections.”

Notwithstanding these points, the BoC’s forecasts include a weighted contribution to GDP growth from gross exports of 1.7 percentage points in 2021, 1.9 points in 2022 and another 1.0 point in 2023. The implied assumption is that stronger global—and particularly US—GDP growth will pull in enough export growth to offset the deterioration in export competitiveness. Net of imports, they expect a drag of 1.1 points in 2021, no contribution in 2022 and a small drag in 2023 (-0.3%). Even with this net drag factored into the projections, the BoC’s is still pointing toward strong 4-handled GDP growth in 2021–22 and above potential at 2.5% in 2023. I would think that any drag from net exports through currency strength would have to be materially stronger than they are forecasting to knock their GDP numbers off track, especially if the above argument on consumer spending upsides proves to be on the mark although part of that would leak out through imports.

HOUSING: CLINGING TO A FORECAST BIAS THAT HASN’T WORKED?

On housing markets, the BoC guided that housing’s contribution to GDP growth will slow from a weighted 0.7% lift to GDP this year to no contribution next year and in 2023. They said "Activity should slow toward levels consistent with the rate of new household formation." We’ll see about that. The BoC has seriously underestimated the housing response to rate cuts thus far and they appear to be sweeping that under the rug.

WHY RATE HIKES MAY COME SOONER THAN THE BoC GUIDES

Since November when vaccine trials became a nascent game changer, I’ve been arguing that there is a strong case for the BoC to hike its policy rate earlier than 2023 and that promising longer guidance could perversely drive deeper imbalances in the household sector. To that effect, perhaps the best question posed to the Governor during the press conference was why he has not significantly changed guidance around what the BoC expects for inflation despite upgrading forecasts for growth while leaving the BoC’s forecasts for potential growth (the noninflationary speed limit) unchanged.

Macklem’s response was that the BoC is expecting a choppy recovery, that right now “we're in a big chop” in reference to the Q1 GDP drop and hence a deeper hole now. He went on to explain that forecasts for 2023 are still “a ways away” and that “we're not being overly precise now.” Fair enough in that an awful lot can happen over the next 2–3 years and they have plenty of time ahead to reassess.

But to investors in the Canada rates curve across maturities throughout the belly and longer end, I find that the overall forecast guidance doesn’t hang together terribly well. With very similar forecast numbers—we have 4.3% growth in each of this year and next and the BoC averages 4.4% over this period—the output gap measure of slack closes off by about mid-2022 (chart 4). Inflation is forecast back at 2% and then just above 2% starting around the middle of 2022. That, in turn, counsels guiding rate hike risk along a similar time horizon in 2022.

Governor Macklem likely knows that and no doubt has plenty of economists advising him on the issue, but he probably wants to see the proof in the pudding. At this juncture I wouldn’t blame him while sitting in his seat as a policymaker focused upon risk management, versus an investor who needs to formulate dynamic expectations for such an environment well ahead of time and can’t wait for the BoC to signal the all clear for tighter policy at which point it’s too late. That bifurcation of duties isn’t always understood terribly well outside of Ottawa. For that audience that the street serves, I would continue to emphasize hike risk in 2022 alongside exiting the QE game around the end of this year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.