- Why the BoC must hike during omicron

- BoC forecast to hike next week, hit 2% by year-end

- The latest inflation print shows the BoC is increasingly far behind

Canadian CPI, m/m / y/y %, December:

Actual: -0.1 / 4.8

Scotia: 0.0 / 4.9

Consensus: -0.1 / 4.8

Prior: 0.2 / 4.7

Canadian core CPI, y/y % change, December:

Average: 2.9 (prior 2.7)

Weighted median: 3.0 (prior 2.8)

Common component: 2.1 (prior 2.0%)

Trimmed mean: 3.7 (prior 3.4%)

Having revised our forecasts, the purpose of this note will be to follow-up with a bit more of a narrative in the context of this morning’s inflation figures.

Let me start by saying there is something that worries me much more about Canada than omicron’s effects, notwithstanding those who argue one can’t possibly be so callous as to hike when omicron cases are rising!

What’s the bigger worry? Plenty of international evidence suggests that it never ends well when a nation passively allows an explosive combination of high inflation and soaring house prices to co-exist to the point to which it begins to be extrapolated in measures of expectations and it starts to change behaviour. It typically ends poorly for the economy. It ends poorly for the most disadvantaged within that economy who are least able to adjust. It ends poorly for the broader financial system.

Canada finds itself at a fork in the road marked by these very conditions. It’s not too late to choose which path we want to go down from here, but we’d better decide now which is why we have front-loaded our rate forecasts. House prices are up 27% y/y with such hot demand that you cannot find product. Official inflation is running at just under 5% y/y and unofficial (truer) inflation is probably closer to 6%. Canada has been running twin deficits for many years and therefore importing savings to feed consumption. It is posting poor growth in labour productivity such that unit labour costs (productivity adjusted employment costs) are accelerating. Wage pressures are abundantly clear when properly estimated and further acceleration lies ahead in second round responses to high inflation. Canada is probably at if not beyond maximum employment with a transitory step backward likely to be quickly shaken off. An unproductive debate over how much inflation is being driven by the supply-side versus the demand-side (it’s obviously both btw…) is time wasted if either way businesses and households are not fussing over the drivers while raising expectations, as they are. That has let the genie out of the bottle, quibbling over reasons be darned.

Set against these realities, the decisions the Bank of Canada begins to make at next week’s meeting will go a long way toward informing the composition of forecast risks over the medium-term amid deepening imbalances. They will also determine Governor Macklem’s legacy. The cruellest thing one can do to Canadians dealing with omicron is to be indifferent toward the fact that their cost of living is soaring across virtually everything they consume and which adds insult to injury. Key here is that omicron hit very different macroeconomic conditions than earlier waves and with that goes a different mixture of the risks to monetary policy. The job of monetary policy at such a point is to manage inflation and leave targeted supports and other measures to other policy officials and private enterprise to manage.

Before turning toward the relatively more mundane matter at hand (ie: the latest inflation wiggles), a brief outline of our Bank of Canada forecasts is offered.

BANK OF CANADA FORECASTS

Here is our revised BoC forecast.

• +175bps of hikes this year, +50 next

• +25bps next week

• +25 in March

• +50 in April

• +25 in June

• +25 in July

• End 2022 at 2%

• Two more hikes in early 2023 to a terminal rate of 2.5%.

• Reinvestment roll-off guidance as soon as next week, implementation by Spring.

This is materially more aggressive than when we had first led consensus with our 8 hikes forecast for 2022–23 last Fall. What has changed since then to give us comfort in becoming more aggressive?

- Governor Macklem’s speech in mid-December dropped the gloves. It was a rather large omission if he didn’t intend to forget to mention they wouldn’t hike until spare capacity is shut, and the tone of his speech fully pivoted toward being more uncomfortable with inflation.

- Fed Chair Powell’s December press conference and his testimony last week did likewise. The Fed and the BoC have altered their reaction functions and we need to adapt as a significant barrier to forecasting tightening has been lowered.

- We have more evidence that omicron is less severe in terms of its outcomes than initially feared. Cases are very high, but hospitalizations and ICU cases are generally reflecting much less average intensity of effects. Perhaps perversely, we have more conviction that omicron will give way to higher antibody levels including via sped-up booster campaigns into Spring.

- Q4 GDP growth in Canada is tracking much stronger than we had anticipated. In fact, it’s hard to decipher much of any macroeconomic effect upon the quarter as a whole from BC’s flooding and/or the other drivers of the economy buried this effect in the numbers. That positions the exit point from 2021 at a higher level which helps to insulate against some of the omicron shock into the start of the year.

- The real policy rate has plunged more deeply negative. When policy should have been tightening, it eased. The inflation-adjusted policy rate is the way to look at policy accommodation including through our models and just as inflation climbed and met a policy of benign neglect it eased policy much further. Even with our forecast pace of policy tightening the real rate will remain significantly negative.

- December’s jobs report added to the jobs recovery that is 241k above pre-pandemic employment levels. Taking a transitory step back in January–February will likely only temporarily dent this overshoot on maximum employment before a rebound follows. Canada is more advanced in its jobs recovery and likely has a higher natural rate of unemployment that it may now be undershooting.

- Evidence of wage pressures continues to mount. Month-over-month annualized and seasonally adjusted wage gains have been in the 6–9% for the past half year and businesses expect more wage pressure this year as demands rise.

- Expectations for inflation, wage pressures and house prices continue to mount as we saw in the pair of BoC surveys earlier this week.

- The housing market continues to be very strong. With the mortgage commitments soon arriving into the all-important Spring housing market the BoC faces the risk that failure to tighten policy set against the backdrop of high inflation will only drive a massive further gain in house prices that could prove to be destabilizing.

This latter point is important. The BoC would not tighten policy just because of housing, but housing pressures on top of ripping inflation change the equation. Waiting to hike until April or later and doing so tepidly will be too little too late and the BoC would risk wearing full responsibility for another massive gain in house prices, more investor activity than even what we’ve observed so far, and greater housing imbalances and future vulnerabilities. Mortgage rate commitments will start accelerating in the weeks ahead and into an environment of rising immigration, no supply and a rebounding economy we could see a very strong housing market in the Spring that further strains sustainable housing affordability.

In all, bringing forward rate hikes are the best medicine for attempting to engineer a soft landing. Hard landing risks would rise if the BoC continues to look the other way while maintaining overly accommodative policy.

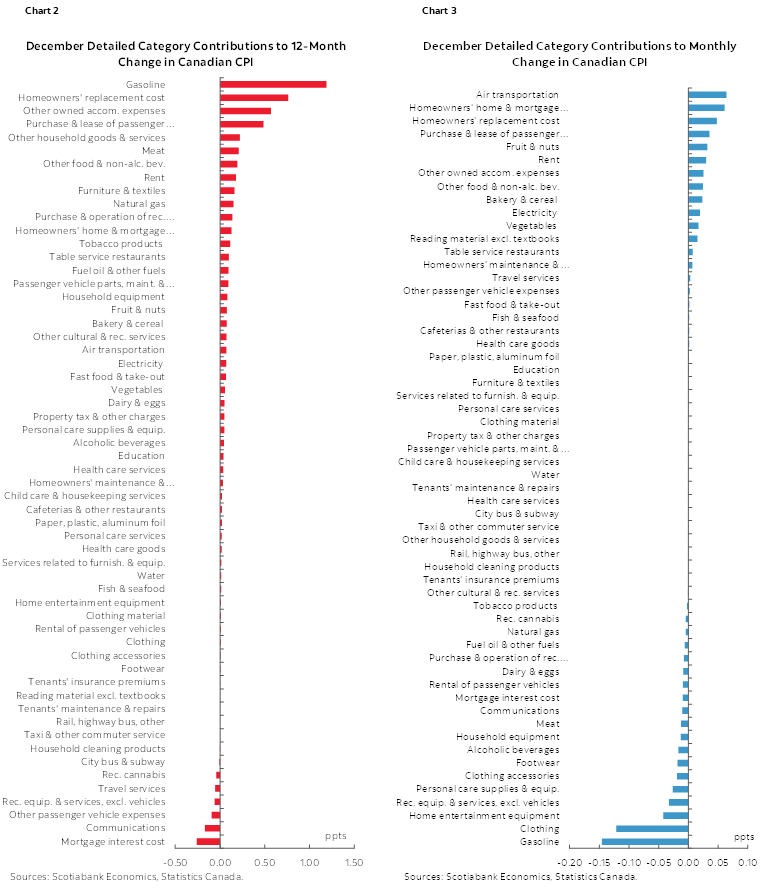

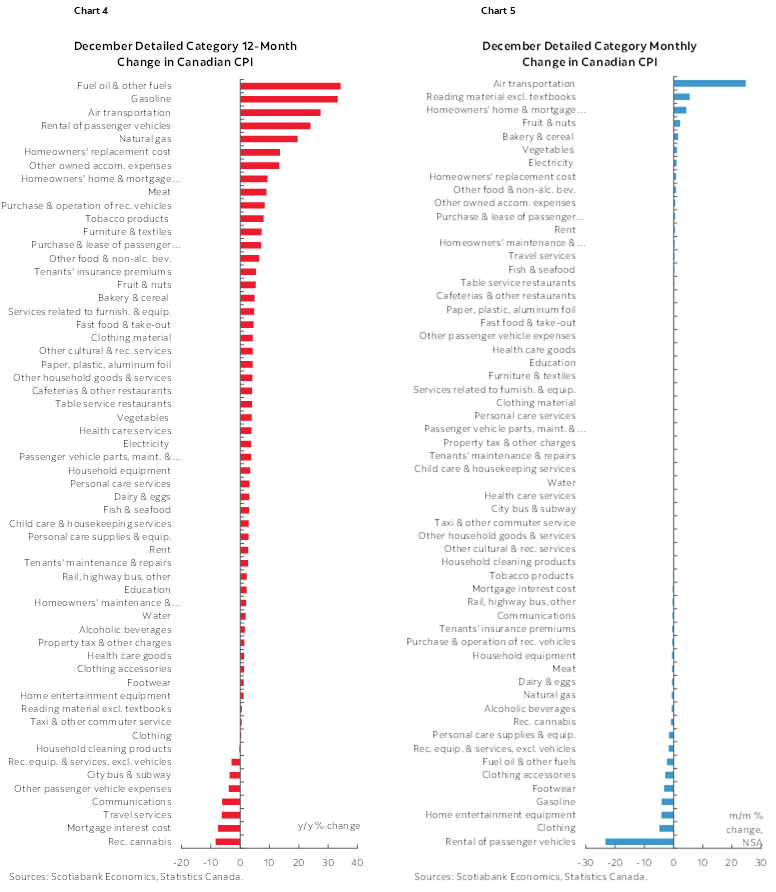

INFLATION LANDED ON THE SCREWS; DETAILS MORE HAWKISH

Headline inflation landed on-consensus in terms of both the year-over-year rate of 4.8% and the month-ago seasonally unadjusted rate of -0.1%.

However, core inflation edged higher and the month-over-month seasonally adjusted headline gain of 0.3% was stronger than I had anticipated. The average of the three core measures of inflation that were introduced by Macklem’s predecessor climbed to 2.9% from 2.7% the prior month (chart 1). All three of the core measures—weighted median, trimmed mean and common component—edged higher. The last time average core inflation was this high was in September 1991 as three decades of inflation targeting are at risk of going up in smoke.

CPI in seasonally adjusted terms was up 0.3% m/m. The month-over-month seasonally adjusted and annualized rate of inflation ex-food and energy was 4.5% in December which indicates there is no loss of pricing pressure at the margin.

Even at that, StatsCan is mismeasuring inflation. True headline inflation is likely running closer to 6–6.1% y/y as argued in the Global Week Ahead. There was zero word from the agency today about its ongoing omission of used vehicle prices versus agencies in the US and UK that seem to have found a solution to the problems.

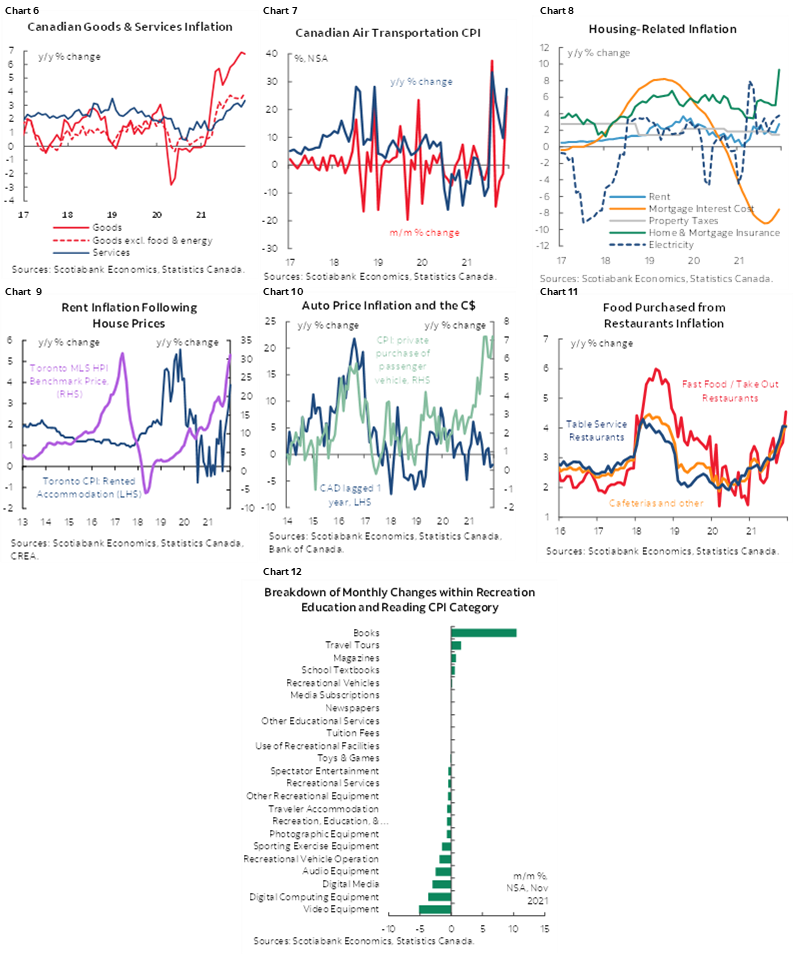

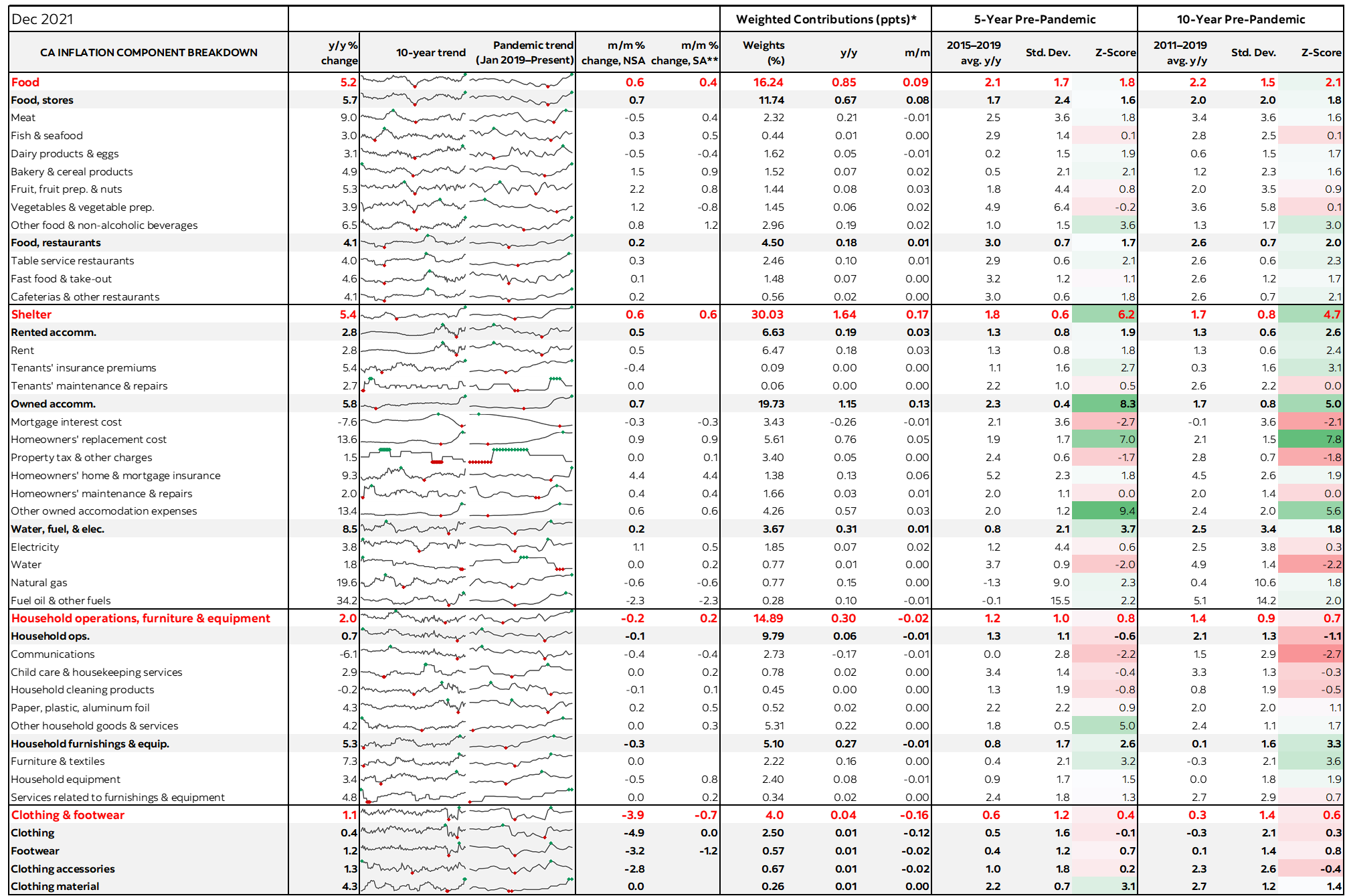

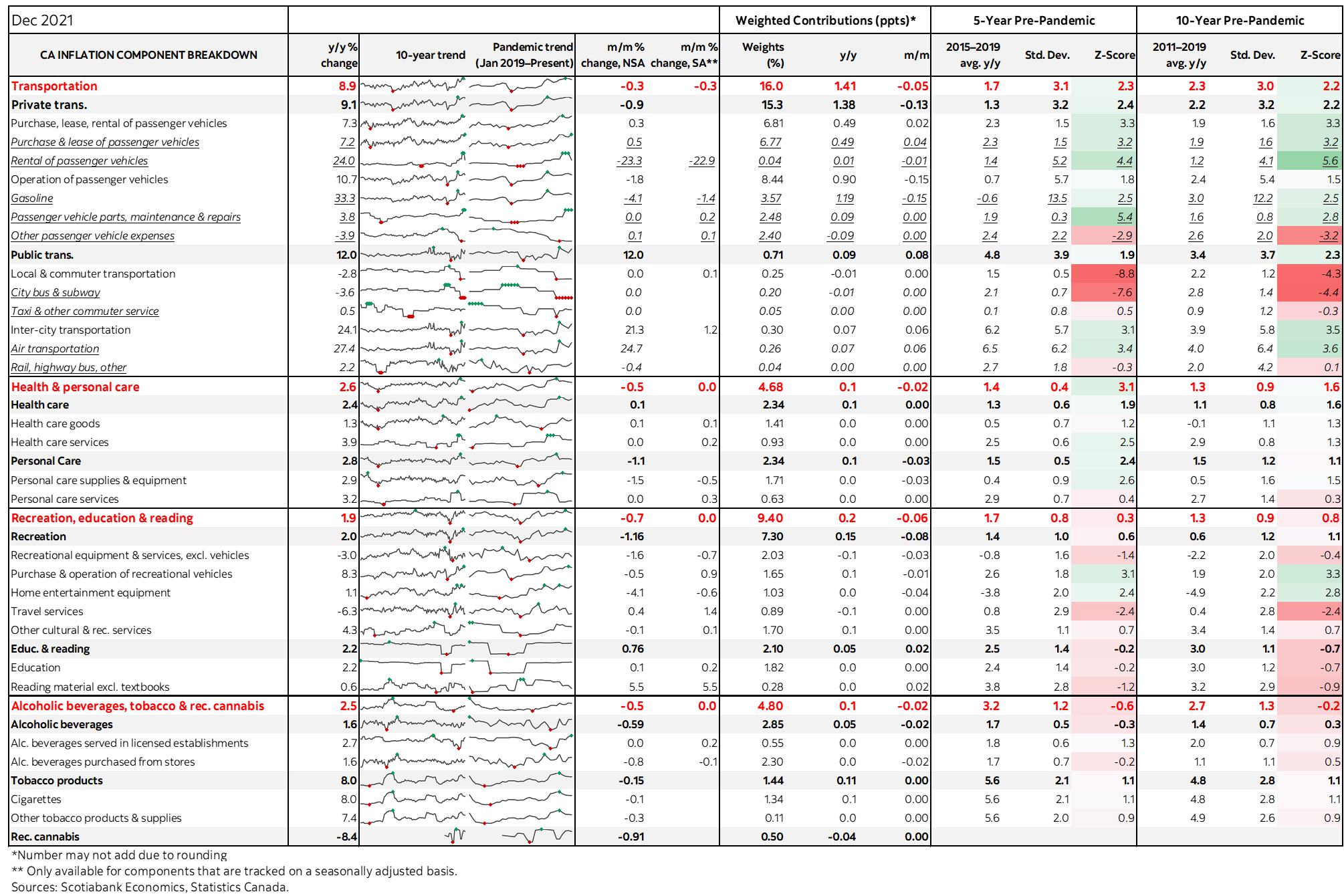

The collection of charts that follows offer further insight into the drivers. The table at the back provides greater detail including micro charts and z-scores to show how unusual today’s price movements are by component compared to recent history.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.