- The BoC is losing control of inflation, wage and house price expectations

- Hiking now would present the least unpalatable criticisms

The Bank of Canada cannot afford to wait any longer to tighten monetary policy. Whether they will or not next week will further inform the composition of risks overhanging the outlook as I’ve never seen that message being communicated as clearly by businesses and households as it was in this morning’s updated surveys (here and here). The BoC should hike next week by taking a page from the RBNZ’s “least regrets” approach to the choices at hand. Before elaborating, here’s what the surveys indicated.

INFLATION EXPECTATIONS

Chart 1 shows that an all-time high of 67% of businesses expect inflation to cruise above 3% over the next two years and hence above the upper limit of the BoC’s 1–3% inflation target range. Another 30% expect inflation to ride in the upper half of the BoC’s 1–3% range over this same period. Basically no business expects inflation to be below 2% in a prolonged overshoot of the BoC’s 2% target.

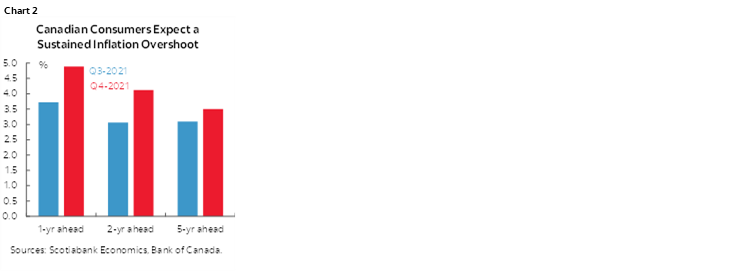

Chart 2 shows that consumers are of a similar mindset. They think inflation will ride at 4.9% y/y over the year ahead, 4.1% over the next two years, and 3.5% over the next five years. They are not saying that they believe that high inflation will be transitory. No one has a lock on forecasting inflation including economists and central banks, but these measures of inflation expectations may have become unmoored and that presents the risk that behavioural adjustments make high inflation a self-fulfilling prophecy that is very difficult to contain without incurring painful adjustments like recessions that at times tend to follow monetary policy mistakes.

WAGE EXPECTATIONS

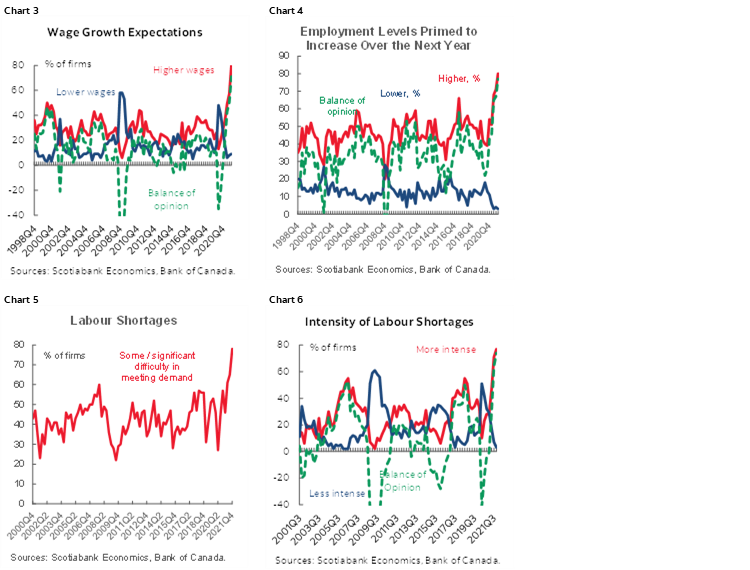

Businesses and households are a bit divided on this issue, but there’s a catch to that. Chart 3 shows that a record 80% of businesses expect wage increases to accelerate over the coming year. That’s because those same businesses are telling the BoC that a record share of them plan to expand their workforce over the coming year (chart 4), they are facing rising labour shortages that are becoming more problematic (chart 5) and that the intensity of labour shortages is the most acute it has been in the history of the survey (chart 6). All of that says that Canada is arguably into a period of excess demand for labour.

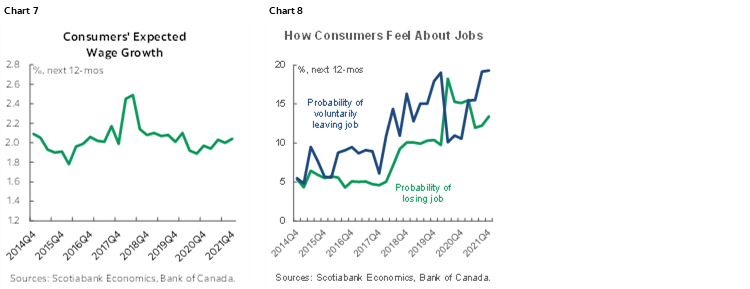

Chart 7, however, shows that consumers aren’t getting the memo and still have modest wage hike expectations. That could be motivating a rising share of them who are saying they’ll seek out other jobs in order to get paid more and that raises retraining and higher costs for employers (chart 8).

CAPACITY PRESSURES

Backing up what they think about inflation going forward is the fact that businesses are saying they are facing rising capacity pressures. Chart 9 shows that 78% of firms are saying they would either face some difficulty meeting unexpected demand (50%) or significant difficulty (28%).

HOUSE PRICE EXPECTATIONS

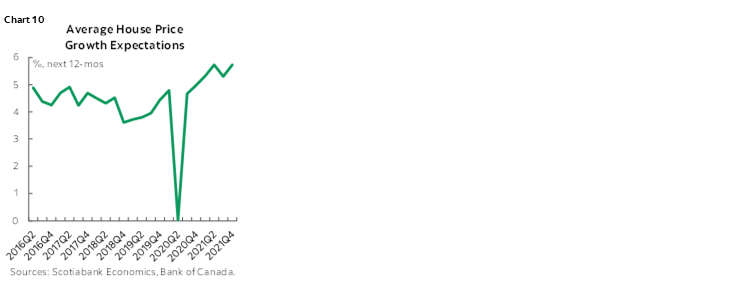

The trend of rising house price expectations continues to point higher (chart 10). Consumers are saying they expect house prices to rise by just under 6% y/y over 2022.

In fairness, consumers are terrible at forecasting house prices in that the true magnitude of the gains throughout the pandemic has far eclipsed what was expected as evidenced by this morning’s update for December that showed consistently-defined house prices up by another 2.5% m/m and ~27% y/y to end 2021. Why? You can’t find product. The sales-to-new-listings ratio increased to 79.7% from 77% the prior month. 80%??!!! Months of inventory now stand at just 1.6 which is an all-time record low.

A combination of no supply and omicron's Q1 impact that will likely drive subsequent pent-up demand could very well drive the Spring housing market to be off the charts in terms of price effects. If so, then seasonal funding pressures could be more acute at that time, and policy pressures may rise. Governments can do little about supply in the near-term. I wouldn't be surprised to see short-sighted policy measures out of Ontario and Quebec that are facing elections this year and we can’t rule out the Feds as well, but a distinction this time around is that the BoC is in play whereas it has not been prior to now during the pandemic.

The rub here is that if the BoC waited until Q2 to hike when all of its fussing over guesstimated output gaps gives them the rigid framework’s ok to do so, then it could be lights out for housing affordability and bigger risks of negative adjustments later. Mortgage pre-commitments and rate locks will be getting inked rapidly over coming weeks with folks locking in 5 year mortgage rates. Hiking by, say, April would be too late for the housing market while inflaming the imbalances through overly easy monetary policy.

ENTER THE BoC’S JANUARY DECISION

Hiking now might expose the BoC to the criticism that they are hiking a touch before their estimates of the output gap shuts. So what. There are many other drivers of inflation beyond the limited usefulness of output gaps as BoC staff research has demonstrated (eg. here). The output gap is a measure of spare capacity that requires being able to accurately measure the economy’s productive potential now, the ability to predict this going forward, the ability to predict actual economic growth with near precision and the ability of it to dominate as an inflation driver. In short, good luck. The evidence on actual inflation and wages plus expectations may be more revealing toward the possibility that slack may be shut now.

Hiking now would trade the risk they may be criticized for hiking a little earlier than when slack may be eliminated for the signal that they are serious about protecting Canadians from runaway inflationary pressures. To households, the choice at this point in the cycle involves paying a little more in interest to try to contain the damaging effects of high inflation on their budgets including the regressive effects. We’re well beyond the point in the cycle here at which there is a free lunch; we either accept tighter policy or we learn to live with potentially runaway prices for everything we buy. The case for hiking right now includes:

- It’s significantly priced by BAX futures and OIS curves. Not hiking now could perversely ease monetary conditions in the face of high inflation which would be more difficult to explain as a logical choice, unless strong guidance to expect +50–75bps by March/April is given. That would make a lot of sense….

- Multiple measures of the BoC’s inflation-adjusted policy rate have sharply declined, one of which is shown in chart 11. I think omicron is a transitory shock, but even if you disagree, the real policy rate has massively eased over the past year during which inflation expectations have risen. This is the way to look at the cost of borrowing—in inflation-adjusted terms—as an input into models determining growth prospects and it says that by neglecting inflation monetary policy has turned increasingly accommodative when it arguably should be turning more restrictive. All the talk of transitory inflation and inclusiveness served to ease monetary policy.

- Measures of wage, inflation and house price expectations are soaring.

- Like the Fed, the BoC should look through omicron's demand side hit while the supply side is getting disrupted again and at a very different part of the cycle than prior variants. Further damage to supply chains due to restrictions and closures in Q2 will likely amplify such price pressures and risk further increases in expected inflation.

- Omicron is a health policy shock for governments to address. Controlling inflation is the BoC’s job full stop. Their tools can do nothing to help the ~7k Canadians in hospitals with COVID-19 and ~1k in ICUs, as tragic as that is. Their tools cannot address backward looking developments that may be transitory. It’s the inflation Canada is importing and the inflation driven by the other 38 million Canadians that should matter to the BoC.

- Unlike the Fed the BoC is done with QE and they don't have to wait to adjust the policy rate. In fact, the BoC has prided itself in being ahead of the Fed all along and hiking before the Fed does so probably in March would be an extension of this.

- We were sharply overshooting our growth forecast for Q4 before omicron and by a lot, so some of the Q1 hit to GDP that is front-loaded at the start of the quarter largely nets out against the Q4 upside in terms of slack.

- The BoC needs to get ahead of the commitments into the Spring housing market.

- The BoC wouldn't hike just on housing, but housing added to being behind on inflation is icing on the cake. Failing to tighten could drive deeper housing imbalances.

- Macklem's speech in Dec was a tone shifter (see recap here). He didn't mention forward guidance hinged upon output gaps and slack once.

- Labour slack is gone. Even if January/Q1 jobs take a step back, Canada had more than fully recovered jobs lost during the pandemic and could come out even after omicron and then keep marching higher on labour demand.

- Even after a January hike, policy would remain uber-easy.

The only ultimate consideration should be doing the right thing. Instead of rigidly adhering to gap-based forward guidance, I’d worry much more about the risk that three decades of inflation targeting experience could be going up in smoke here with the BoC losing its right to brag about being a leading light among inflation-targeting central banks. It undershot its inflation target for a long period, but the magnitude of sustained overshooting now being signalled could be an overly abrupt swing to the other side of the ship.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.