- Inflation expectations remain well above target for years to come

What will catch the BoC’s eye in surveys of business expectations (here) and consumer expectations (here) is likely to be the evidence of sticky wage and price pressures.

USDCAD was left unchanged by the results. Canadian short-term yields are outperforming other markets today. Two-thirds of today’s 9bps rally in the two-year yield occurred before the releases this morning and another 3bps decline has been tacked on since. In my view, this reflects dovish positioning into the start of the week ahead of CPI tomorrow with either little incremental effect from the surveys and/or markets and some media outlets are not reading their implications the same way as I am.

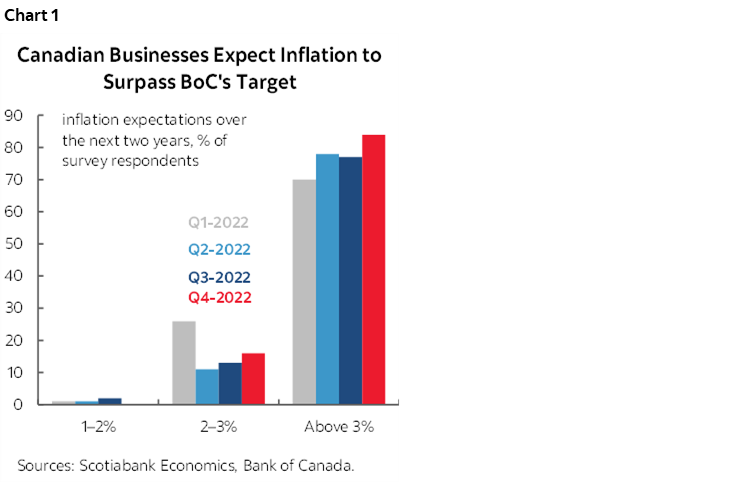

Businesses are demonstrating no faith in 2% (chart 1). The latest results point to a whopping 84% of businesses who think that inflation will average over 3% over the next two years which is up from 77% the prior quarter.

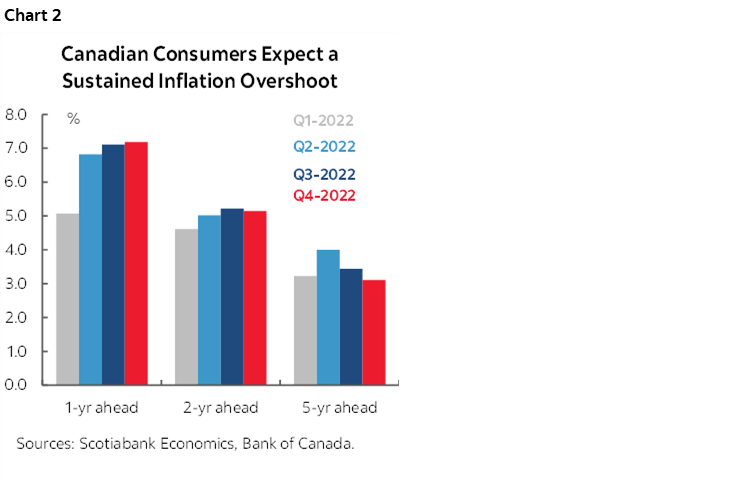

Consumers not only do not believe that the BoC will hit its 2% inflation target within any reasonable time period, they also don’t believe that inflation will land within the 1–3% policy target range for many years (chart 2). Consumers’ expectations for inflation held steady in the 1- and 2-year horizons at 7.2% (prior 7.1%) and 5.1% (prior 5.2%) respectively, while the 5-year ahead inflation expectations gauge eased a touch to 3.1% (prior 3.4%) but remains above 3%.

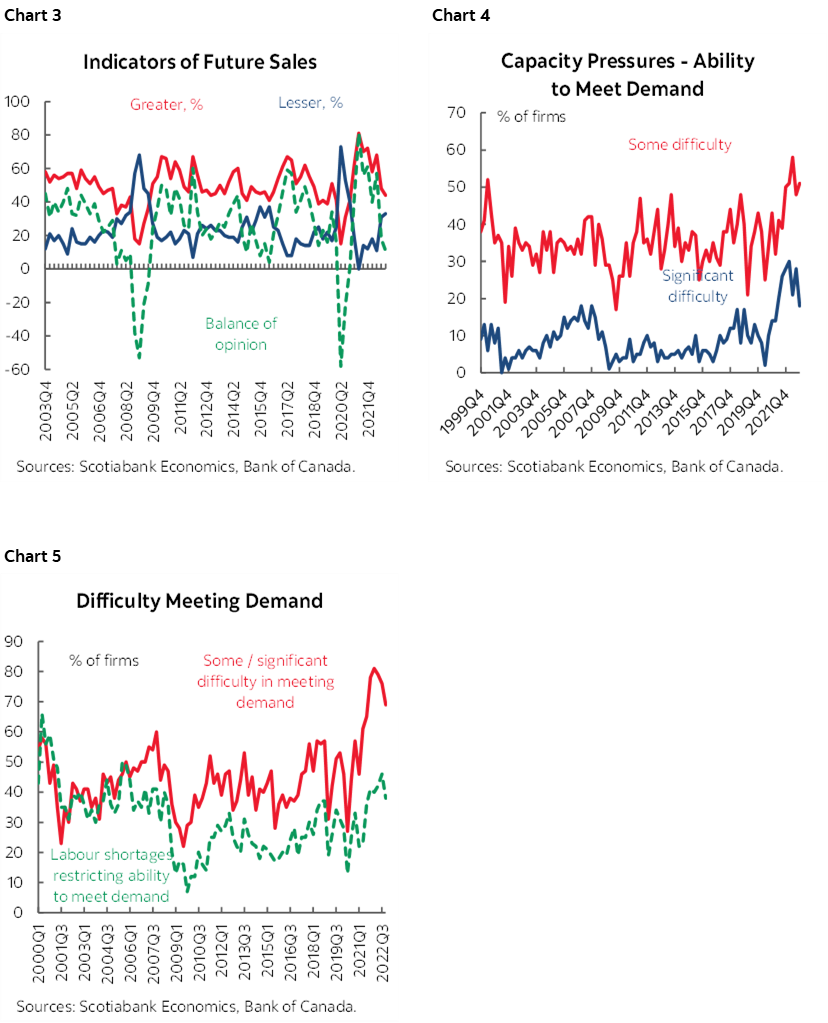

Businesses are also showing lessened optimism toward future sales growth (chart 3), but they still expect growth to stay in the black and recall that this is coming off a period of torrid growth when Canada’s economy outshone the rest of the world throughout 2021Q3-2022Q3. That’s a point of resilience and against recession talk. Businesses continue to report ongoing capacity pressures that are just a little lighter than previously (chart 4). Businesses are also continuing to indicate very high difficulty meeting demand with only a slight easing compared to prior quarters (chart 5).

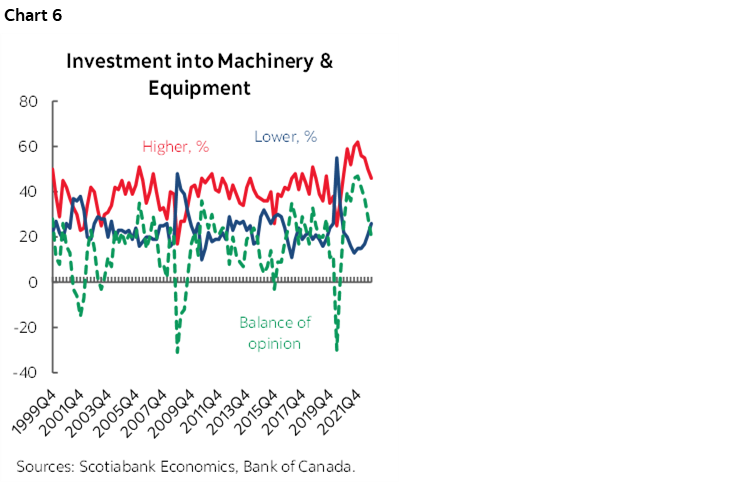

In order to rise to the occasion, businesses are signalling continued appetite to investment in machinery and equipment with a modest deterioration in the balance of opinion in favour of investing (chart 6).

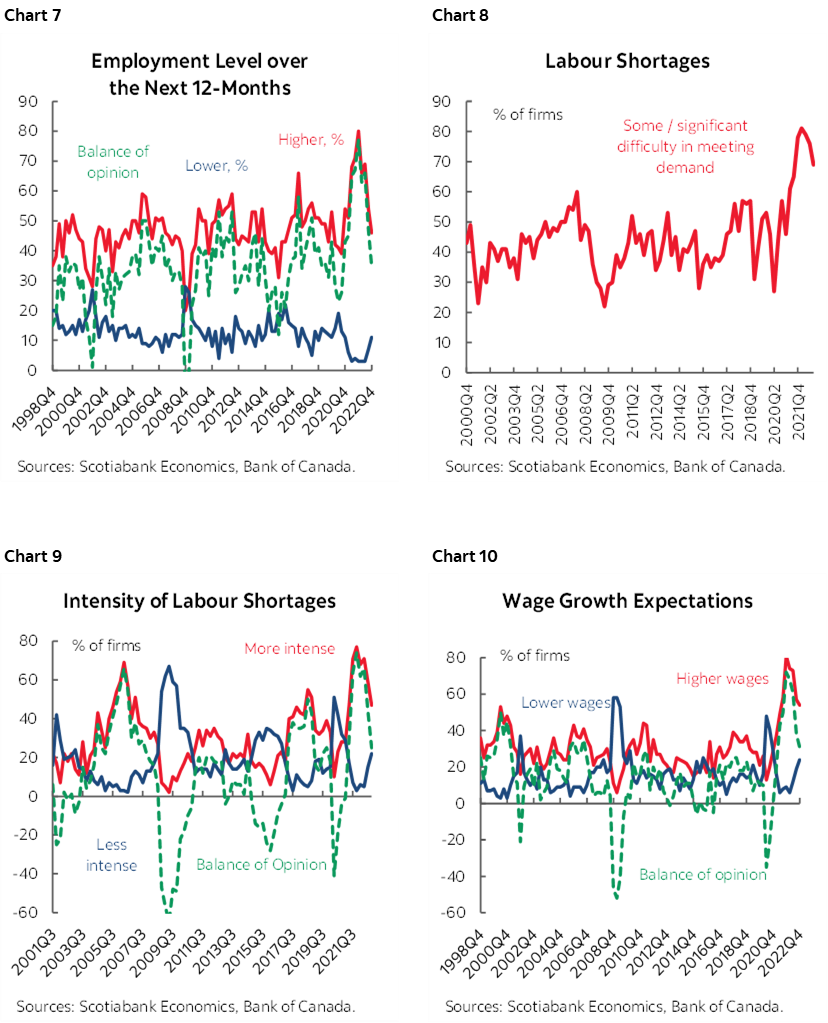

A majority of firms also continue to signal that they intend to hire more workers over the next year than firms signalling they intend to let some go and the net balance of opinion in favour of more hiring is now back toward longer-run averages from historically elevated readings (chart 7). One reason for positive but somewhat lessened hiring appetite lies in what they are saying about the ongoing difficulty getting workers that improved in negligible fashion and remains a historically pessimistic heights (charts 8, 9). Accordingly, firms believe they will have to continue to raise wages going forward but the net balance of opinion of firms saying they will have to raise wages has softened somewhat (chart 10).

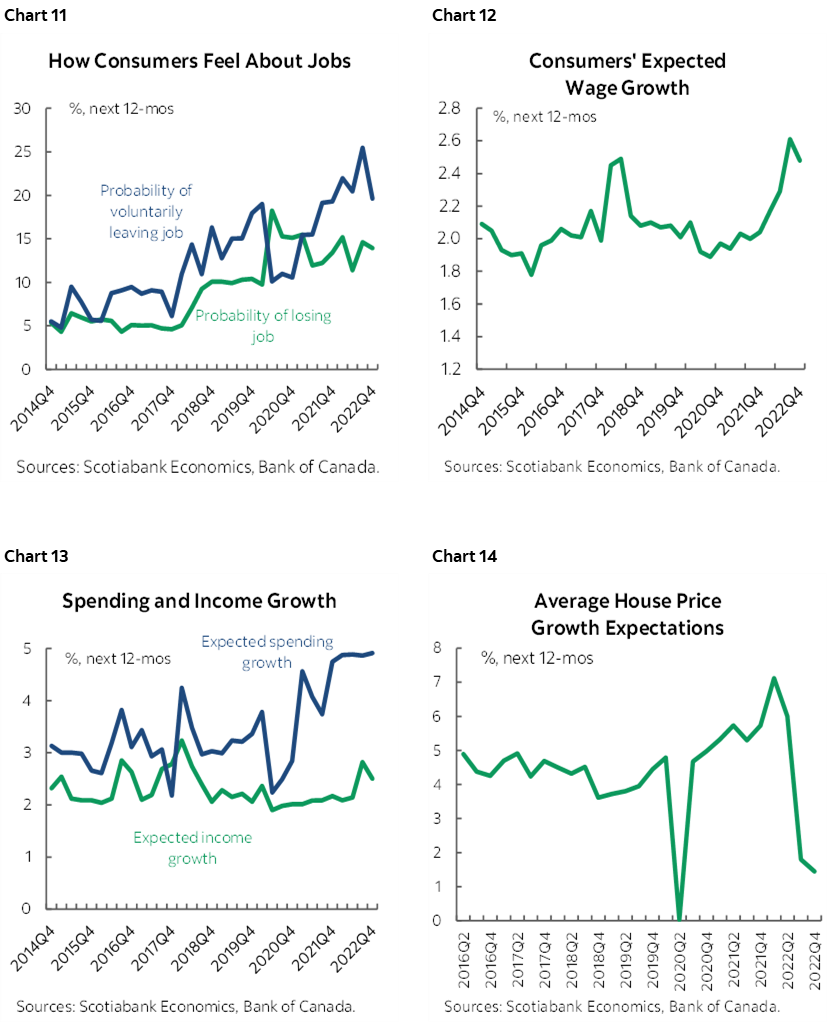

A large number of consumers are still signalling willingness to voluntarily leave their job which is a plus in terms of appetite for mobility and with a steady percentage response to the probability of losing their jobs (chart 11). Consumers still expect relatively faster wage growth going forward than in prior years at only a very slightly cooler pace (chart 12) and bear in mind that their perceptions bear little resemble to what the data shows on quicker wage growth over the years. Consumers still signal that they expect to spend at a faster rate than save as they have been signalling for years (chart 13); hello, debt. The BoC will be pleased by greater caution toward house prices (chart 14).

The surveys have a spotty track record in terms of lining up with what actually happens. They also lack some freshness (October 27th to November 17th for the consumer survey, . November 14th to December 2nd for the business survey). Onto CPI tomorrow!

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.