Strong core inflation may have already arrived

Massive income transfers to buoy the US consumer…

...before vaccines and behaviour must drive sustained growth

US personal income/spending, m/m % change, January, SA:

Actual: 10.0 / 2.4

Scotia: 11.2 / 3.0

Consensus: 9.5 / 2.5

Prior: 0.6 / -0.4 (revised from 0.6 / -0.2)

US PCE inflation / core PCE, y/y % change, January, SA:

Actual: 1.5 / 1.5

Scotia: 1.4 / 1.3

Consensus: 1.4 / 1.4

Prior: 1.3 / 1.4 (revised from 1.3 / 1.5)

A round of updates on the US consumer’s financial position offered a glimpse toward what lies ahead in the form of a strong consumer-led rebound driven by massive fiscal stimulus. In the process, evidence of inflationary pressure may well be upon us already.

INCOME GROWTH HAS JUST STARTED TO SOAR

Nominal personal income increased by 10% m/m SA in January with inflation-adjusted personal disposable income up 11% m/m. Excluding transfers, inflation-adjusted income fell 0.5% m/m for the third consecutive monthly decline. The massive offset came through transfers.

The increased transfers reflected the December stimulus bill provisions that sent out US$600 stimulus cheques per person and boosted unemployment insurance cheques by an extra US$300/week.

This is the start of what will be explosive all-in income growth over 2021H1 through what is bound to be very choppy monthly data (February incomes will fall as cheques don’t repeat). The next disbursements are expected in April following expected passage of the US$1.9 trillion Biden stimulus bill that includes US$1400 cheques per person at a cost of up to US$465 billion as well as further extension and enhancement of unemployment benefits.

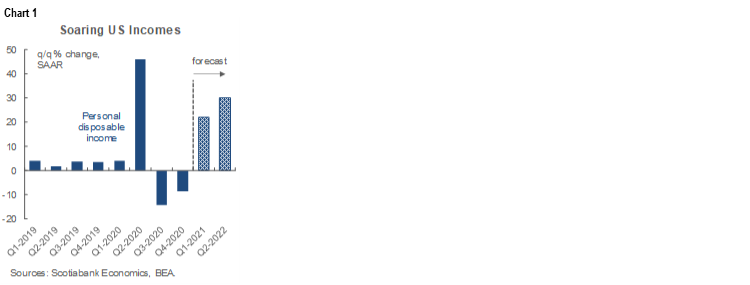

Overall, the effects should be powerful enough to drive US personal disposable income higher by 22% q/q at a seasonally adjusted and annualized rate in Q1 and then another 30% in Q2 (chart 1). These are nominal figures, but even after adjusting for low inflation almost all of that will be a boost to purchasing power that will combine with high stockpiles of cash and near-cash holdings in the household sector and wealth effects through house prices and equity markets.

CONSUMPTION

So how much of a purchasing power effect is translating into consumption so far? We already knew that retail sales were up smartly in January and had several drivers that probably included stronger than usual gift card effects, but soft services spending restrained the overall impact such that total personal spending was up 2.4% m/m in nominal terms and 2.0% in inflation-adjusted terms. That made the month no slouch as it was the fastest inflation-adjusted gain in consumer spending since last June.

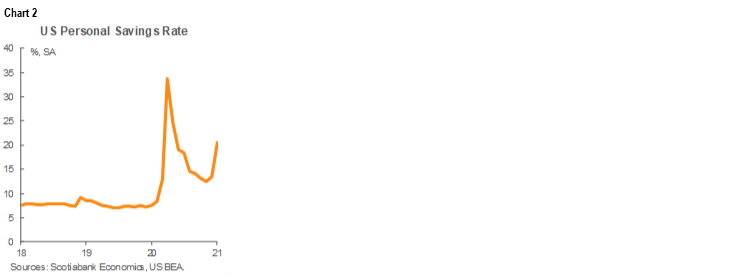

But it’s likely only just the beginning. The saving rate shot up to 20.5% in January for the highest rate since last May (chart 2). The first-round effect of disbursements is to spend a little and hoard a lot. The second-round effects will likely be to spend those amounts in a manner akin to what happened last summer before vaccines were in sight. Further, because many consumers expect another round of cheques and broader stimulus, they may pull that forward and spend some of the proceeds in anticipation while leveraging some of it. Some of the proceeds are still likely to be put toward balance sheet repair and maybe some will think in Ricardian equivalence terms by looking ahead to the possible future tax burden, but we’re talking US consumers here!!

INFLATION IS HERE

Backward-looking inflation readings don’t matter much in a forward-looking bond market, but for what it’s worth, core PCE inflation was a touch firmer than expected at 1.5% y/y last month. That matched headline inflation. The prior month’s core PCE reading was revised down a tick to 1.4%.

So while it’s backward-looking, the inflation readings are not entirely without meaning to the monetary policy debate. What we’re getting in core PCE inflation is not just the stuff of a dead cat base effect bounce and for two reasons.

First, core PCE inflation has risen from a trough of 0.9% y/y last April to 1.5% now despite the fact that one-year ago inflation just before the pandemic was running at 1.75% y/y. The base effect bounce still lies ahead when year-over-year inflation is being compared to the downdraft in the core PCE price index last March/April, but it doesn’t explain why we’ve already rebounded from the lows.

More important, however, is the higher frequency inflation signal we are getting absent base effects. As chart 3 depicts, the annualized and seasonally-adjusted month-ago core PCE inflation rate is running hot at 3.06% in January and was 3.7% the month before for a two-month average of about 3.4% m/m SAAR.

Two months of hot core PCE inflation—barring pesky revisions—do not make a trend yet, but it illustrates what to watch as opposed to Chair Powell’s rather misleading guidance to the street’s economists and markets that inflation will only rise due to soft year-ago base effects and that the Fed will simply look through it. At the margin, inflation is here. It is here now. It may have legs. It may rise further from what is already occurring. It could rise partly on year-ago base effects in the year-over-year comps over coming months. It is already rising on a higher frequency tracking basis and could well accelerate further once all of this stimulus hits the economy. Combine the two arguments and bam, the Fed’s got it’s wish much earlier than they are guiding. Inflation risk could rise quite materially as massive income transfers alongside very low borrowing costs arrive in the context of what is probably going to be inventory depletion and a still damaged supply side owing to the consequences of the pandemic and Trump’s trade wars.

Persistence will still be debated, however, as the matter then migrates back to whether there will be continued momentum after the stimulus has been disbursed. Maybe we will get even further stimulus more focused upon an infrastructure bill given that the Biden administration can use the budget reconciliation approach twice this year to pass stimulus with its thin majority in the Senate.

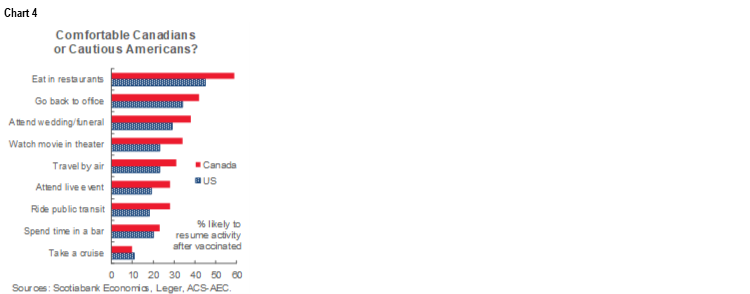

More important is the issue of whether behaviour adapts once the US has full inoculation of the adult population by summer. Chart 4 is repeated here in that it shows 20–50% of respondents in both the US and Canada indicate that after getting jabbed, they will return to pandemic-affected activities especially things like eating in restaurants and returning to the office when they get tired of one way conversations with the family dog. These responses could build with improved confidence, but going from depressed levels of these activities now to 20–50% could well be a very powerful growth catalyst. If not, consumers are likely to spend their stimulus and what they save from not spending on these other activities on all manner of other things. What’s rule number 1 in forecasting the US consumer? Right, never underestimate their capacity to spend, spend and spend some more.

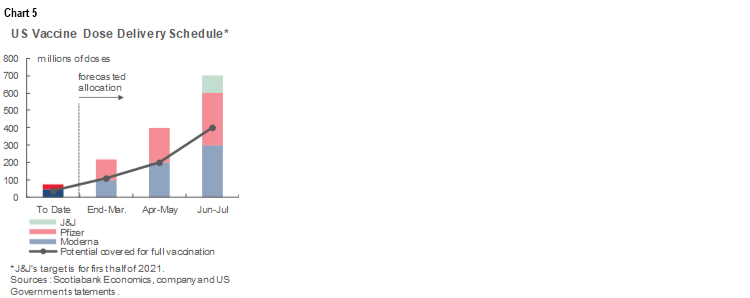

This behavioural response and/or substitution effect toward forms of spending on things that are socially distanced is critical to the outlook. It is what is required for organic growth to eventually take over from flinging cheques around. As America marches toward full vaccination (chart 5), this could very well turn into a rather positive and sustained outlook.

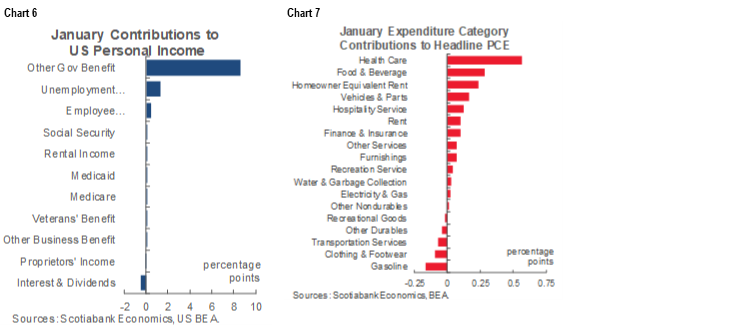

In closing, charts 6 and 7 offer a break down of the sources of income growth last month and the weighted contributions to overall inflation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.