- A 25bps rate hike was delivered…

- ...and guidance still points to “ongoing” rate hikes in the plural sense…

- …and against rate cuts this year...

- ...but financial markets rejoiced upon hearing Chair Powell waffle on key matters

- Next steps: high data dependency, opportunity to clarify

The FOMC raised the Fed’s policy rate by 25bps to a new upper limit of the fed funds target range of 4.75% as widely anticipated except for a minority who thought they might either hold or raise by 50bps.

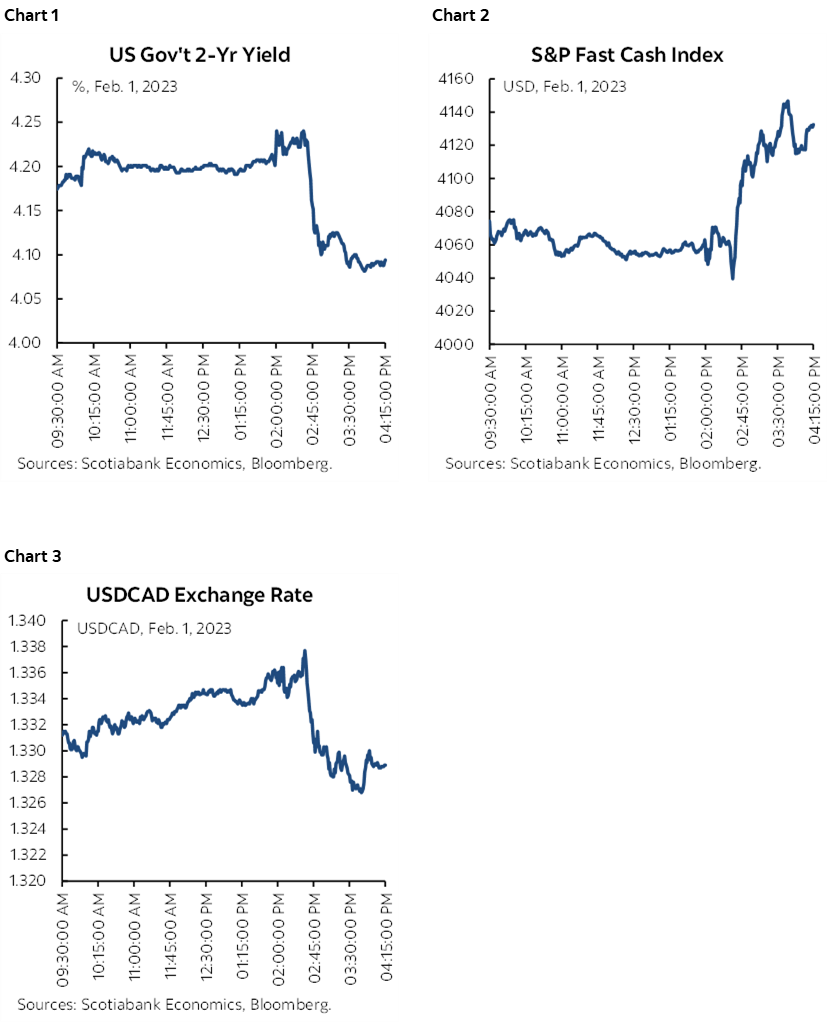

Whether deliberate or not, an initially hawkish reaction immediately following the statement then gave way to Chair Powell’s press conference that served to ease financial conditions as reflected in lower bond yields, higher equity prices and a weaker USD. Charts 1–3 show the intraday movements in markets. Some of that could be due to positioning swings or markets misinterpreting the path forward.

I think a big portion of the reaction was due to the lack of conviction that Powell demonstrated during his presser as he waffled a fair bit and read pre-prepared answers to key issues. Again, that may have been either deliberate in terms of his views, or as a signal of greater uncertainty on the Committee, or perhaps it just was not his best performance and in fairness some of them have been better than others in the past. My general impression is that recent illness notwithstanding, he left his ‘A’ game behind back in December.

What follows is discussion of the changes to the statement, comments made in Powell’s opening statement to the press conference, and then a detailed dissection of the salient points drawn from the press conference.

STATEMENT CHANGES

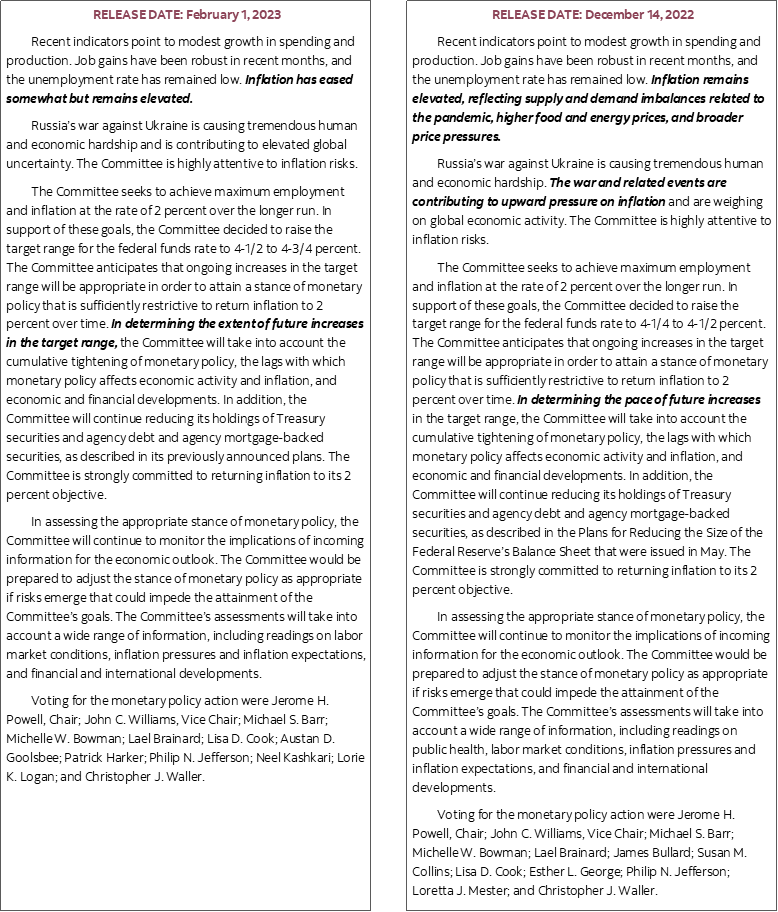

There were a few modest changes to the statement as flagged in the accompanying statement comparison.

1. First up are the omissions

The second paragraph deleted reference to how “The war and related events are contributing to upward pressure on inflation.” That’s perhaps true but risks remain on that matter.

The first paragraph struck out further explanation of inflation’s drivers as “reflecting supply and demand imbalances related to the pandemic, higher food and energy prices, and broader price pressures.” Powell explained the pandemic omission during the press conference (see below).

2. The changed wording references

The FOMC acknowledged some progress toward lower inflation by softening the reference in the opening paragraph from how “Inflation remains elevated” to “Inflation has eased somewhat but remains elevated.” This is largely a factual acknowledgement and retained caution around the level.

3. What did not change

More important is that against some speculation they might have softened their forward guidance, they instead chose to retain reference to “ongoing increases” in order to be “sufficiently restrictive” which clearly they are saying has yet to be achieved. The plurality of the reference suggests that the FOMC has in mind to raise the policy rate at least twice more by 25bps each. They rejected a pause reference and rejected an attempt to tee up one final hike.

The statement was unanimously supported by the new rotation of FOMC members.

There was no change in guidance around balance sheet plans.

POWELL’S OPENING STATEMENT

Powell said many of the right things in his opening statement at first and before further comments drove easier financial conditions in the Q&A part of the presser.

During his opening statement, Powell said the Fed has "more work to do" and repeated they will need to have a "restrictive stance for some time" while observing that the "labour market remains extremely tight" and that "the labour market continues to be out of balance" with demand exceeding supply. That sounded like Powell completely fading any worries about layoffs.

Powell acknowledged a “welcome reduction in the monthly pace of increases" in inflation but "we will need substantially more evidence that inflation is on a sustained downward path." He also repeated that longer run inflation expectations remain anchored but that inflation remains too high and there is still the risk of it becoming entrenched.

THE PRESS CONFERENCE DROVE EASIER FINANCIAL CONDITIONS

Chair Powell’s answers to several key questions lacked conviction while resisting any effort to lock horns against market pricing of the rate path going forward. It was during the press conference when the Q&A started that markets responded by easing financial conditions.

Dot Plot Guidance Was Less Committal

Powell was asked if the dot plot from December was still applicable in that it had set a terminal rate expectation of 5¼%. His answer was less committal than at the December meeting when he delivered the fresh dots upon raising the forecast while also saying they might raise the terminal rate goalpost even higher at the March meeting. He did not repeat that point and simply said “We did not update the assessment today and will do so in March. We think we have covered a lot of ground. We have not made a decision on March. We will look at incoming data. It could certainly be higher than what we are indicating now. At the same time, if the data comes in in the other direction, then we'll make data dependent decisions.”

Powell was probed more directly on risks to the Committee’s terminal rate guidance and how he weighs them toward either raising or lowering it and his response was that “It's very difficult to manage the risks of doing too little. This is a very difficult risk to manage. We have no incentive and desire to over tighten. We have tools that would work on easing inflation. The job is not yet done.”

Not Fighting Financial Conditions

Reporters lobbed three grapefruit at Powell on whether he is fussed by market pricing that is undercutting the FOMC’s guidance and Powell ducked each time in such fashion as to convey little conviction in his own view which is a much less strident version of Powell than we heard at the December press conference.

The first time when he was asked if easier financial conditions have made his job of fighting inflation harder and whether he is prepared to raise more to offset this, Powell read a prepared answer and said “It is important for financial conditions to reflect what we are doing. We are not focused upon short—term moves but over time.” Ok then. Right below that point might have been a reminder to get milk and bread on the way home.

When asked again, he said “Financial conditions have not changed much since our December meeting. We're just going to have to see how fast inflation comes down. Our forecast is that it will take longer to achieve and we'll have to keep rates higher for longer, but we'll see.” He described markets as having a different forecast.

That’s far short of having much of any conviction in your own forecast and markets seized on the moment.

When it was noted by a reporter who excels at arithmetic that “ongoing" rate hikes implies at least two more hikes but markets are pricing one more and done and asked whether that was plausible or whether he was concerned about market pricing, Powell said:

“I'm not concerned. It is based upon market expectations for inflation coming down. Markets have inflation coming down faster than us and it's a different forecast. I don't see us cutting rates this year but if we do see inflation coming down more quickly then that will play into our views. We’ll have to see.”

In short, Powell resisted locking horns with markets.

Pause?

Powell was asked why he wouldn’t pause now. His answer was “Because inflation is still running very hot. We're trying to make a judgement on exactly how restrictive we need to be.” That suggests uncertainty around the terminal rate.

Powell explicitly said “The Committee did not see a pause as appropriate at this meeting.”

But when pushed further on whether they discussed the conditions for a pause at this meeting, Powell deflected it by saying “Wait for the minutes. The sense of the discussion was talking quite a bit about the path forward.” That kind of comment is flagging the risk that they did indeed discuss a potential pause arriving at some point and so we will closely watch the minutes in three weeks from now.

How Much More Inflation Evidence is Needed?

Powell said “It's a very positive thing" that people believe inflation will come down.

In response to a question about how long a period of softer inflation is required to have conviction they can stop raising rates and be encouraged by easing pressures, Powell deflected and said:

“By the March meeting we'll have two more inflation and two more employment reports. We'll be watching the data. This cumulative evidence will be reflected in our outlook and our policy.”

Ok so two more rounds of softish core inflation and the lemonade stand gets packed up? Hikes are done?

Still, he went on to note that they don’t know the answer to whether the easy part has now been achieved and getting down to 2% sustainably will be harder. He said “We don't know. This is not a standard business cycle where we can look at the past. It's unique. Certainty is just not appropriate here. Inflation is hard to forecast. We're going to be cautious about declaring victory and the game is won. It's early stage. We're in the early stage of disinflation.”

Rate Cuts Ruled Out, Maybe, Kinda, Sorta

On the length of a pause after ending hikes, Powell said “If the economy performs broadly in line with our expectations, then it would not be appropriate to cut rates this year.” He took that back, however, by leaving the door open to possibly easing if inflation cools more than they expect. That suggests high short-term data dependence rather than sticking it out for longer in order to make sure.

Inflation Guidance—Easing, Not Easy, But Might Become Easy

Powell remarked that "We can now say that the disinflationary process has started" which was music to the ears of financial markets.

He nevertheless cautioned that this is truer in goods prices and will probably become truer in the lagging way in which housing gets captured in inflation as the year wears on, but that “56% of the core PCE index is not cooling yet.” He went on to say that disinflation “is happening in about a quarter of the PCE basket in goods. Also in housing within the core PCE basket that we expect to drift lower if new leases continue to be soft. We need to see disinflation in core services within PCE and we're not yet.” He noted that “the disinflation process underway is really at an early stage. Goods price inflation has eased as supply chains have improved and we continue to expect housing inflation to ease in lagging fashion. Core services are not showing disinflation yet. What we are seeing so far is progress but not a weakening in employment conditions.”

Inflation’s Drivers

Powell was asked whether his understanding of the inflation dynamic may be wrong such that he could achieve the inflation target without higher unemployment and without requiring a higher policy rate. This is basically asking Powell if he believes in the Philips curve in any form.

Powell rejected the notion by saying "You're not going to have a sustainable return to 2% inflation in that sector [ed. he's talking core services] without a rise in unemployment.” But then he waffled and said “I still think there is a path toward getting inflation back down to 2% without a big rise in unemployment." He went on to say that “Inflation can return to 2% without a really big increase in unemployment or a really big contraction" and "most forecasters would say that's not likely but it's possible.”

Powell also continues to keep the door open to a soft landing by saying “I do think positive growth will continue but at a subdued pace." Equities might have liked that. Powell went on to cite strengths in the labour market, an improved global picture, the fact that state and local governments are flush with money and thinking of tax cuts or sending cheques, that falling inflation will improve confidence etc

Skipping on the Way Home?

When asked if the FOMC could skip meetings and have gaps between hikes, Powell rejected the notions and said “We're not exploring this. We used to go every other meeting by 25bps and that was considered fast. We are not on the point of deciding right now.”

The Pandemic is Ovah!

Says Powell. Must be true, I guess. When asked whether he believes that the pandemic is not weighing on the economy, Powell said “It's still out there but we struck that reference out because it is no longer playing a major role in the economy. It doesn't need to be in our statement as an ongoing economic risk.” I could not tell if his fingers were crossed while saying this.

Wage Price Spiral?

Powell said he did not see signs of a wage price spiral at this point, but that “once you see that it's too late. We can't allow that to happen.”

Debt Ceiling

When asked about the debt ceiling and its potential implications, Powell read a scripted response and said he believes Congress will and must act to raise the debt ceiling. “We will of course monitor money market conditions carefully as the process moves on. We understand the Treasury General Account will move lower and then back up with implications for reserves and repo.”

Powell was asked about Fed contingency planning if the debt ceiling risks move past the so-called “x-date” when Treasury runs out of room to use emergency options to avert a default. Would he do what Treasury directs in terms of making prioritized payments? Powell ducked and said “There is only one way forward and that is to raise the debt ceiling. Any deviations from that path will be highly risky. No one should assume the Fed can offset the risks. I'm just going to leave it at that.”

Recall that in the past it has been floated that perhaps the Fed would make payments on defaulted Treasuries but in minutes to a past emergency meeting sounding loathe to go there for obvious reasons.

NEXT STEPS—DATA INTO MARCH, OPPORTUNITY TO CLARIFY

If markets misinterpreted anything that Chair Powell wished to convey today then there will be several opportunities to address this. One will be in the minutes to the meeting in three weeks time. Before that, we’ll hear from Chair Powell on February 7th before the Economic Club of Washington. He will also testify before Congress in semi-annual fashion either later this month or in March presumably before the blackout ahead of the March 22nd meeting.

My overall conclusion is to stay tuned. I think Powell spoke back and forth to multiple sides of the possibilities going forward and we’re going to be extremely data dependent on the path to the March meeting which, frankly, is ridiculous in my view. Inflation is a long game. It’s not about a handful of months. If the Fed overreacts to short-term disinflationary forces then perhaps it risks resurrecting inflation later on.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.