- Canada’s economy had basically recovered before omicron struck...

- ...but now faces fresh uncertainties and a fuller accounting of BC’s flooding

Canada GDP m/m % change, October:

Actual: 0.8

Scotia: 1.0

Consensus: 0.8

Prior: 0.2 (revised from 0.1)

November ‘flash’: 0.3

Canada’s economy was doing rather well at least in the pre-omicron world. The Canadian dollar and bond markets largely ignored this morning’s figures for monthly GDP because they may be a stale reflection of current conditions and given light holiday trading.

Because of these points, I’ll only offer a few high-level observations.

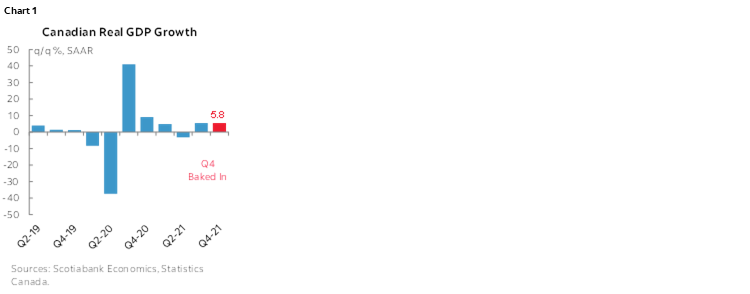

1. Growth is tracking 5.8% q/q SAAR in Q4 based upon the Q3 starting point, the first two months of Q4 including the November ‘flash’ estimate, and with December assumed to be flat simply in order to focus the math upon the effects of what is known so far without imposing artificial judgement. See chart 1.

2. This outcome was the result of not only a strong month of October when the economy grew by 0.8% m/m but also a mild upward revision to September and the preliminary ‘flash’ guidance for November that indicated a further 0.3% expansion.

3. Treat the November ‘flash’ with care. I couldn’t find one word of reference to BC’s flooding in StatsCan’s brief write-up. Presto, it never happened!? Not even worth a comment on effects?? We’ll have to see how the final number holds up (and then subsequent revisions…). The ‘flash’ GDP estimate is based upon the portion of responses that inform other flash readings for components like retail sales, manufacturing shipments etc. As more data comes in covering more of the month I suspect the November GDP guesstimate may be revised downward.

4. For now, we’re only told that growth in November was led by sectors that are probably getting smoked about now. StatsCan said November’s GDP growth was led by sectors like accommodation and food services plus arts and entertainment.

5. Omicron has introduced fresh uncertainties. Mobility readings are still holding up reasonably well and most restrictions are narrowly focused upon bars and restaurants alongside smaller limits on crowd sizes including at sporting events. It’s assumed there is a very high bar to any further broadening of restrictions into the new year but this risk can only be monitored alongside cases, hospitalizations and outcomes into the new year.

The Q4 GDP estimate is based upon monthly GDP concepts whereas the Bank of Canada’s forecast for 4% Q4 growth is based upon GDP using expenditure-based concepts. There may be modest upside risk to the BoC’s forecast but it will all come down to how omicron impacts December readings and November revisions.

Chart 2 shows weighted sectoral contributions to October’s GDP gain of 0.8%. Chart 3 shows that by November, Canada was only –0.066% (less than one-tenth of 1%) away from recapturing all of the pandemic’s hit to the economy before omicron struck. Chart 4 shows October’s unweighted growth by sector and chart 5 updates tracking of the cumulative recovery in GDP by sector during the pandemic.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.