- Communications largely met expectations…

- ...while avoiding feared outcomes

- Tapering and rate hikes were brought forward

- Powell more fully explained his pivot

- The meeting minutes may further inform key questions

The Federal Reserve successfully took a further step toward the exits and without significantly disrupting financial markets. In fact, stocks rallied, Treasuries hardly budged, and the USD depreciated largely out of relief that a more abruptly hawkish pivot was not pursued. Yet. For now, the Fed gets high marks for advance communication around a hawkish pivot that was reasonably well telegraphed. A lot has been learned since the 2013 taper tantrum.

WHAT CHANGED

What they did can be summed up in five main points derived from the statement (here), the Summary of Economic Projections (here) and the press conference. Please also see the attached statement comparison.

1. Rate hikes pulled forward

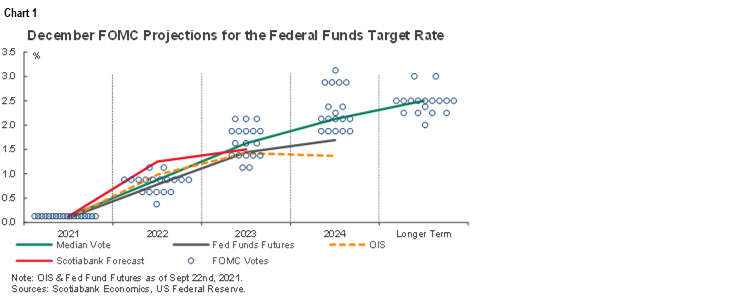

Chart 1 shows the updated dot plot in relation to our forecast and both fed funds futures and OIS pricing.

The median FOMC projection calls for 75bps of hikes in 2022 and then another identical move in 2023. The end result would be to still wind up below most estimates of the neutral policy rate two years from now. That implies that the Fed would still be applying a marginal amount of stimulus to an economy well past the point of needing it. I suspect they’ll coax markets along a tighter path over time and that the dots are one part about economics and reflective of present uncertainties, and the other about managing markets. Still, the fact that there were only two FOMC members who were willing to signal more than 3 hikes and that even they only went one above helped to assuage some market fears around the pace at which Powell and Co would run screaming toward the exits.

Markets might have also been relieved if they inferred that the committee wants a bit of distance from ending purchases in March and subsequently hiking. Three hikes in 2022 and the distribution of meetings over 2022 could inform this view. I think the first hike is most likely to be delivered at a full meeting with full communications which could mean March, but then if they go as soon as March then they're signalling only two hikes over the remaining 6 meetings which doesn't signal much conviction to tighten every third meeting on balance. Our forecast for lift-off is June and for 100bps of hikes over 2022.

Powell noted that the FOMC still intends to maintain an unchanged fed funds rate range until maximum employment is achieved and that all FOMC members expect this to happen next year. Powell did note, however, that “In my view we are making rapid progress toward maximum employment.”

2. Earlier end to bond purchases

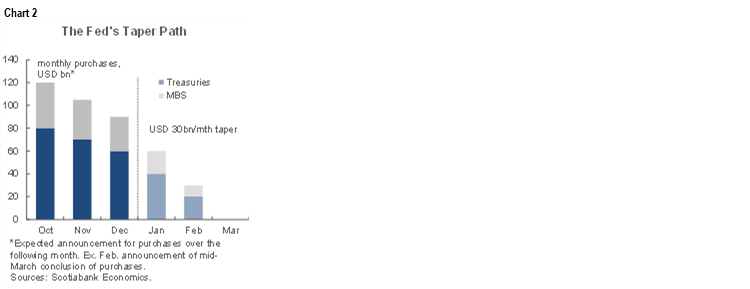

Big surprise here! Not. Everyone—probably even the pizza delivery guy—expected the FOMC to expedite tapering by the amounts and pace described in the statement and as shown in chart 2. Another US$30 billion reduction in monthly Treasury and MBS purchases is planned for implementation in January and “similar reductions in the pace of net asset purchases will likely be appropriate each month.” There are only so many months before that path gets to zero. By March, in fact.

One motivation for ending purchases earlier was confirmed when Chair Powell stated that "a quicker conclusion of our purchases will give us more flexibility to consider the full range of outcomes" and policy choices.

3. Open guidance on other balance sheet plans

Before purchases end in March, the FOMC will have to make some other key decisions on balance sheet management.

When asked about how much distance he thinks there may be between ending purchases and hiking and what to do in between and after the first hike, the short answer involved guidance to wait for the minutes in three weeks time and specifically watch for language that cites the frequency of opinion (eg. “some”, “a few,” “many,” “most,” etc.) around whether to pursue a period of reinvestment and for how long before hiking and for how long after how many hikes. Powell simply said they discussed balance sheet issues but haven’t made any decisions of that nature. He indicated that the committee discussed differences compared to the 2013–15 experience and stated “I don't foresee us taking that long a period of time after ending purchases before hiking.” That wasn’t terribly useful to markets since markets are priced for lift off by June and hence much sooner than after ending purchases in 2014.

4. Transitory?? Pfft. Who said that anyway?!!

There were material changes to the statement language around inflation that confirms the Powell-led FOMC has done a full pivot.

First, the November 3rd statement had said “Inflation is elevated, largely reflecting factors that are expected to be transitory.” That’s gone. You won’t find the word anywhere in the December statement.

Second, the statement now struck out “With inflation having run persistently below this longer-run goal” and replaced it with “With inflation having exceeded 2 percent for some time….”

Third, the language around current inflation was refreshed to “elevated levels of inflation” instead of “sizable price increases in some sectors.”

5. Forecasts: Lower Unemployment and More Inflation

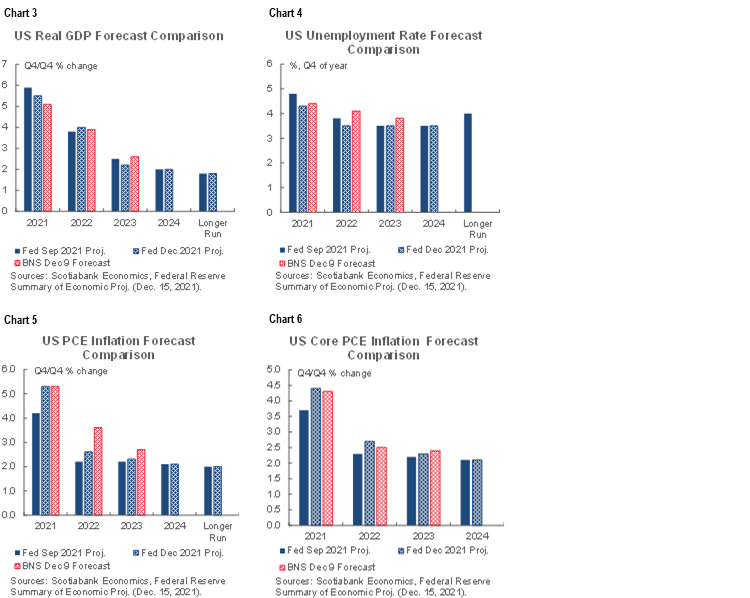

Charts 3–6 show the updated FOMC forecasts for growth, inflation and the unemployment rate. GDP growth was lowered a bit this year given year-to-date tracking, upped a touch in 2022, lowered a bit in 2023 and left unchanged beyond that. Strong growth is forecast for next year and growth in 2023–24 is forecast to be a little above the economy’s noninflationary speed limit.

The unemployment rate projections were revised down for this year by a half point given stronger job markets, lowered again for 2022 partly given this better starting point plus assumed additional progress, and then left unchanged thereafter.

PCE and core PCE inflation were revised up this year given year-to-date tracking. Both were also revised up next year which is consistent with firmer growth but also Chair Powell’s view that supply side challenges will persist “well into next year.” A touch more inflation was also added into 2023 before it returns toward target thereafter. Powell’s opening remarks to his press conference noted that “price increases have now spread to a greater numbers of goods and services" but wage growth isn't very hot so far but is being monitored.

RELATED DISCUSSIONS

There were a number of other areas of discussion during the press conference that further informed the Powell pivot.

Maximum Employment and Wages

This is where I thought Powell’s communications were somewhat confusing and somewhat revisionist in nature. During the press conference, he noted that real wage gains are not in excess of productivity growth and are therefore not inflationary. He’s likely reference average hourly wages minus inflation relative to trend productivity.

He also went on to note, however, that the spike in the Employment Cost Index on the eve of the November FOMC meeting was among the short list of factors that motivated him to change his mind on inflation. ECI captures wages and benefits. Yet unit labour costs are an all-in-one measure of employment costs relative to real GDP with the latter embodying productivity. ULCs are accelerating faster during the pandemic than before which doesn’t seem to support the narrative that employment costs are not more inflationary than previously (chart 7).

The other cited factors were the strong jobs report and the strong CPI report. Powell said “I honestly at that point really decided we needed to speed up the taper.”

Perhaps, but there will always be doubts around whether the Fed Chair just simply fouled up on ‘transitory’ inflation—which I think he did—and whether his candidacy for a second term as Fed Chair clouded his thinking.

Still, when probed about why he thinks progress toward maximum employment is faster, Powell’s main point was that “the disappointing metric has been labour force participation. I thought last Fall that we would see a significant surge in labour force participation due to vaccinations and return to school and lower job supports etc. It seems now that the return to the labour force will take longer which is what has happened in past cycles.”

Also note that gone was any reference toward more inclusive measures of progress in labour markets compared to the strong amount of emphasis Powell put on them in earlier press conferences.

Omicron worries?

The statement noted that "risks to the outlook remain, including from new variants of the virus” which leaves open the possibility we may see additional variants. Powell said “I think there’s a lot of uncertainty which is why we put it as a risk in our statement.” He went on, however, to note that “The early evidence is that omicron is highly transmissable, but less severe. But what will be the effect on the economy depends upon how it operates on demand and also supply and hence the impact on inflation is uncertain. This is going on at the same time as a wave of Delta cases. I do think wave upon wave people are learning to live with it, and more people are getting vaccinated.”

Powell nevertheless noted that "notwithstanding this the committee participants continue to foresee rapid growth."

One reason for this is that both the statement and Chair Powell’s comments expect two influences to cross one another: they expect supply constraints to ease up as an offset to omicron worries. The statement spelled it out by noting “progress on vaccinations and an easing of supply constraints are expected to support continued gains in economic activity and employment as well as a reduction in inflation.”

He did sensibly note that the Summary of Economic Projections put out by the FOMC is not a plan, it is an expectation for policy that is based upon their forecasts. The median forecast expects strong growth and strong inflation. If the economy turns out to be quite different from that then Powell said “of course we'd change our actual rate decisions that depend upon the evolving nature of the forecast.” This matches our philosophy. Forecast with the best reasonably know information at a point of time and then monitor.

Still, at the end of the day, Powell says that he thinks the economy can handle putting away bond purchases no matter what omicron brings.

Is the Fed Behind the Curve?

Powell’s belief is that the lags between changes in monetary policy signals, the impact upon financial conditions and the linkages to the economy and inflation may be shorter than others may assume. This was offered as a defence against why he shouldn’t get out of bond purchases and onto hikes even faster if taking his time were to mean a slower response to inflationary pressures. Powell’s argument was that “we think markets can be sensitive to it and we've always preferred a methodical approach. I do think that in this connected world, financial conditions can affect economies shorter than 6 months. In addition, when we communicate changes, financial conditions can react immediately. They don't wait to change, they change when they expect changes.”

In my personal view, he’s right on financial conditions reacting rapidly and in anticipation, but I didn’t like his implied tone on how long it takes for such changes to impact the economy and inflation.

Does the Treasury Curve Worry Powell?

When asked if he’s worried about the bond market signals and specifically if he would prefer a steeper curve before hiking Powell’s answer wasn’t very compelling. He noted “A lot of things go into long rates. Around the world they are so much lower elsewhere. It's not surprising to have so much demand for Treasuries relative to bunds and JGBs. There may also be some assessment of the neutral rate embedded in the Treasury market. We'll make decisions based on what we think is appropriate for the economy. I'm not troubled by where the long bond is.”

The debate is around whether a relatively flat curve is a bond market warning sign against hiking too much too fast, or whether the curve is distorted. Time will tell. It could be too flat because of another over-reaction to omicron just as Ts rallied into the summer/Fall wave. One could also argue that earlier debt ceiling and funding uncertainty pushed yields temporarily lower. As supply gets taken down in markets with the dwindled amount in Treasury’s General Account and as the Fed shuts down bond purchases we could wind up facing a very different bond market into 2022.

As a final point, there remains work to be done in controlling Fed releases. The communications began to arrive just before the 2pmET window. There may not have been equal monitoring across market participants which would connote an advantage to some.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.