- FOMC delivers a more hawkish than anticipated set of communications

- Why markets reacted the way they did

The FOMC delivered a slightly more hawkish set of messages than markets expected along with much of the press that was flogging a dovish pivot narrative after two lousy CPI prints that landed on the softish side. That was not my expectation as written and they in fact delivered an even slightly more hawkish set of messages than I had thought likely.

That’s because they raised the terminal rate even higher than I thought likely while Powell reaffirmed that they view inflation risk as still skewed toward the upside and dismissed recent CPI readings. He intimated that the bias toward the anticipated peak policy rate remains pointed even higher yet just as they have raised their estimates throughout the past year along with everyone else and to varying degrees. Time will tell if that’s an attempt to use the Fed’s communication tools to offset easing financial conditions of late or what they truly do believe. We’ll see who blinks going forward. Powell also reinforced that sufficient progress toward their goals remains an uphill battle.

MARKET REACTION

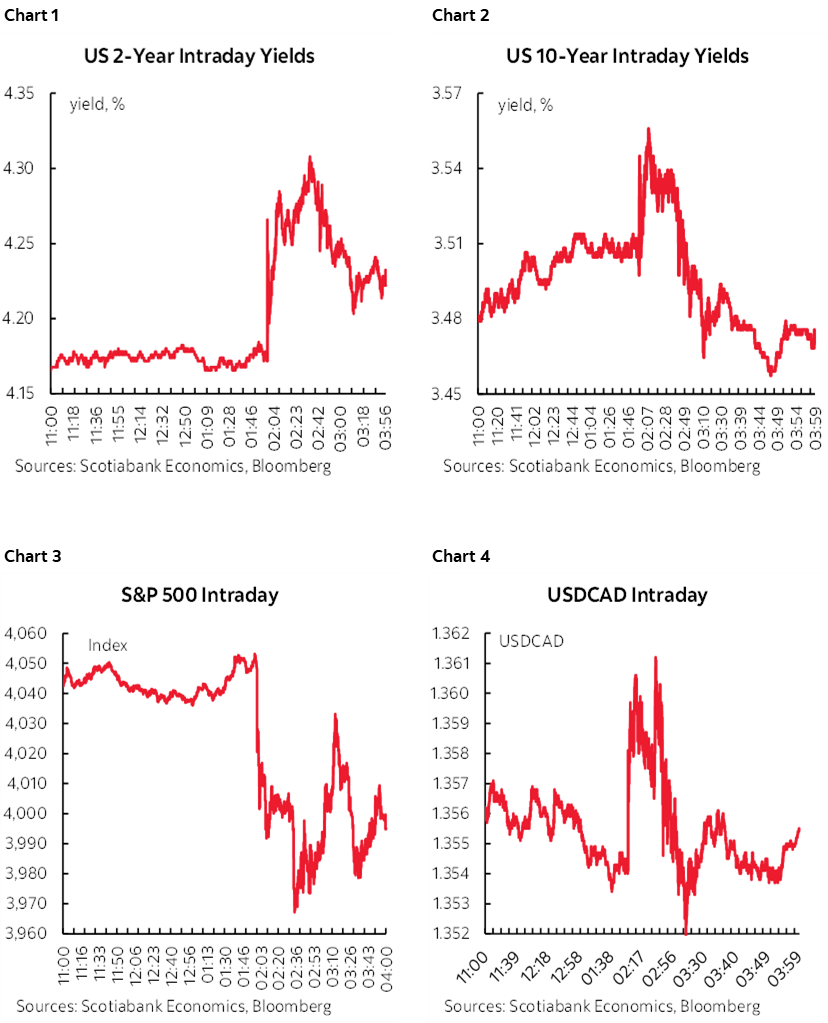

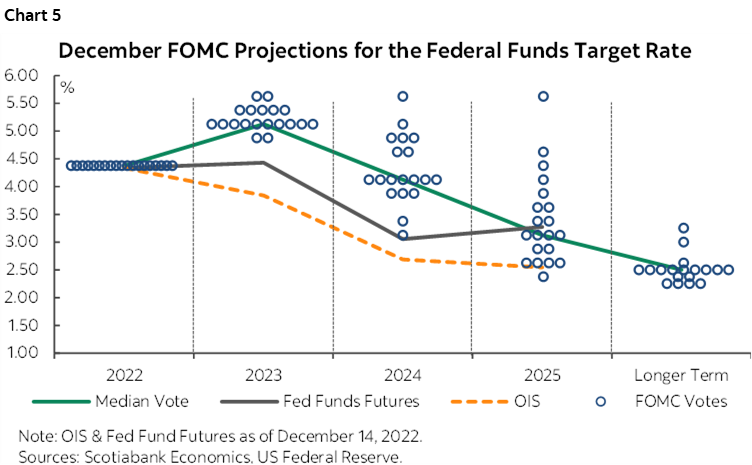

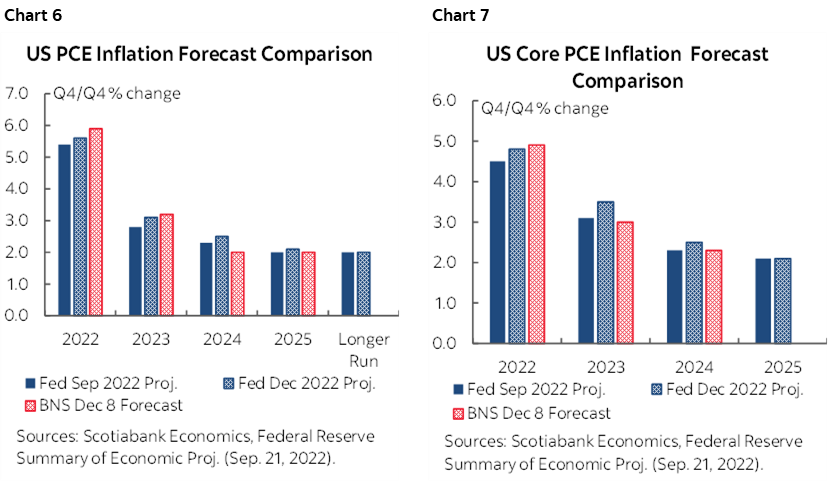

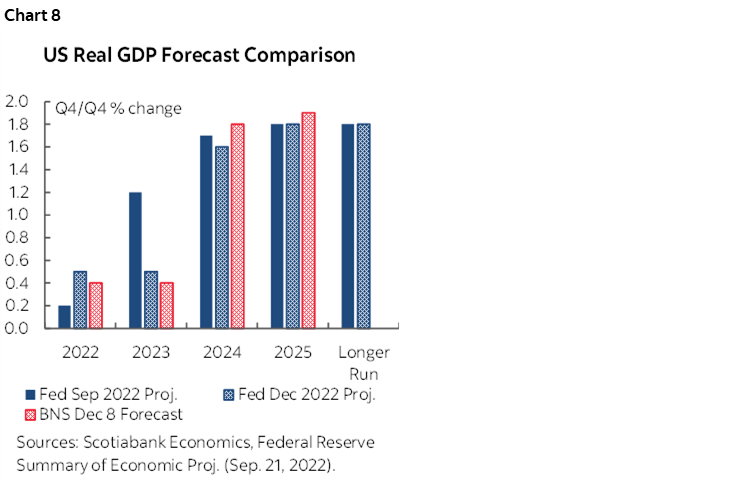

The initial market reactions to the statement and Summary of Economic Projections were reined in somewhat ahead of the press conference and through it, but not consistently so across all asset classes (charts 1–4). The two-year US Treasury yield closed about 4bps higher. The 10 year yield initially went up by 4bps but ultimately fell by a net 4bps into the close. The USD appreciated at first on a DXY basis but wound up largely unchanged by the end of the day. The S&P500, however, lost 1.4% of its value post-statement.

So why such oscillations? Maybe when Treasuries saw equities sustainably drop they sought havens following the initial reactions. Perhaps positions got consolidated into tomorrow’s developments and not least of which uncertainty toward what the ECB may do and its effects on the euro and EGBs. It’s also possible that markets don’t believe Fed guidance at this point but the strong caution on that count is that markets haven’t fared so well chasing rate hikes higher and higher this year.

Here’s what they did in the full suite of communications.

RATE HIKE WAS UNIVERSALLY EXPECTED

The Fed funds upper limit was raised by 50bps to 4.5% as guided and widely expected. What I like about this central bank is that they generally have a word; the verbiage and details can offer some surprises, but the administrated rate changes have consistently avoided game day surprises.

THE DOTS!

The ‘dot plot’ is part of what slammed markets at first (chart 5). They had guided that the terminal rate would be raised “somewhat” at this meeting, but raised it by 50bps instead of a more moderate 25. The FOMC now thinks that the terminal rate may have to rise to 5¼% in 2023.

That’s not just because of a few errant dots. There is pretty high conviction on the Committee that they need to go to a terminal rate of 5.25% instead of just up a quarter to 5%. Only two dots are at 5%, 10 dots are at 5.25%, five at 5.5% and two members went to 5.75%.

STATEMENT CHANGES

Please see the accompanying comparison of today’s statement and the November edition. Statement changes were notable because, well, there were hardly any! The key one that was being watched most closely was hawkishly left unchanged.

There had been some speculation that the reference to the sentence that says “that ongoing increases in the target range will be appropriate” could have been softened or even struck out. It was retained in verbatim fashion.

In fact, the only change in the language was in the second paragraph that might be slightly construed as signalling a little less inflationary pressure being driven by the war in Ukraine and related events. Instead of saying this is “creating additional upward pressure on inflation” they are now saying they “are contributing to upward pressures on inflation.” Not being “created” and simply “contributing” suggests less momentum in this driver of inflation. I’ll come back to explain how this is of minimal consequence to the Fed and how Powell described the Committee’s outlook for inflation’s multiple drivers.

FORWARD GUIDANCE

Chair Powell and his FOMC colleagues had consistently guided that the peak policy rate would be raised “somewhat higher.” Markets had taken that to mean possibly going from a peak policy rate of 4 ¾% to 5%. Instead, the committee raised its peak policy rate forecast by 50bps to 5.25%. They also raised the policy rate projections in 2024–25 by ¼% in each year and left the longer-run neutral rate estimate unchanged at 2.5%.

Another point is that there is pretty high conviction they need to go to a terminal rate of 5.25% instead of just up a quarter to 5%. Only two dots are are 5%, 10 are at 5.25%, five at 5.5% and two cowboys/girls are at 5.75%

The Committee is being playful with the dots again, or it's yet another coincidence. 2023 dots form a mild up arrow, 2024 a primary school down arrow. I suppose it’s possible that I’ve just been looking at these Rorschach plots for too long!

FORECASTS

The macro projections now take a little longer to achieve 2% core inflation with the upward revision to 2024 which is now 2.5% instead of 2.3%. See charts 6, 7.

Growth projections were downgraded (chart 8).

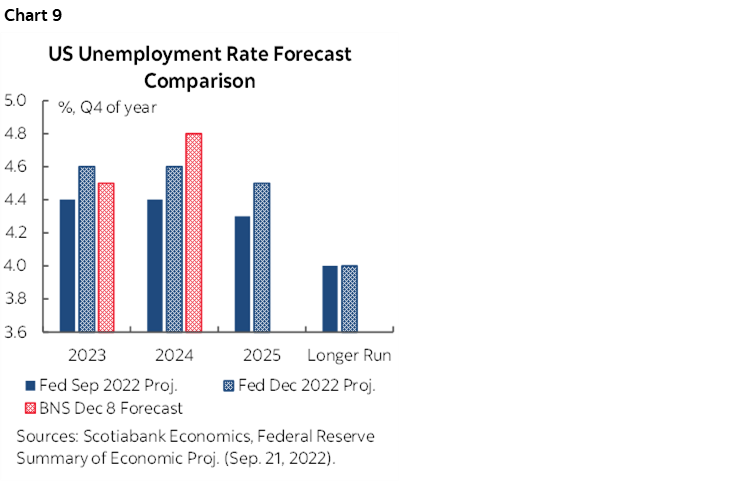

Unemployment rate forecasts were raised (chart 9).

POWELL’S HAWKISH OPENING STATEMENT

Powell came out swinging at the start of his press conference and was clearly determined to push back on those who either think he should pivot or had expected him to do so.

Some of the one-liners in his remarks included the following that reinforced what criteria he requires before being comfortable that they are on the path to 2% inflation:

- "we have more work to do"

- They will be "maintaining a restrictive stance for some time"

- GDP has been roughly unchanged over first 3 quarters of this year. That’s important because he has said he wants a sustained period of below-potential GDP growth to open up slack in the economy.

- “The labour market remains extremely tight"

- “The labour market continues to be out of balance with the demand exceeding supply of available workers." This too is important because Powell has stated very clearly that he won’t be satisfied that inflation could land durable on 2% until balance is brought back to the job market.

- “it will take substantially more evidence to give confidence that inflation is on a sustained downward path."

- "participants continue to see risks to inflation weighted to the upside"

- “Reducing inflation is likely to require a sustained period of below trend growth and rebalancing job market.”

- "The historical record cautions against loosening conditions prematurely."

NOT YET RESTRICTIVE ENOUGH

Powell was asked whether easier financial conditions and the acceleration of GDP growth since the November meeting are something that invites a response from the Fed.

Powell answered that “Our focus is not on short-term moves but persistent moves. We are not at a sufficiently restrictive policy stance yet which is why we say that ongoing hikes will be required. 17 of 19 FOMC participants wrote down a peak rate of 5% or more. At each subsequent SEC this year we have raised this terminal rate. Inflation has moved higher over the year. I can't tell you confidently that we won't raise our terminal rate estimate again in March.”

That last part is more hawkish again. He is acknowledging the pattern while previously saying in the press conference that the risks to inflation projections are pointed higher and thus he is leaving the door open to moving higher yet on the terminal rate projection.

RESTRICTIVE FOR AS LONG AS IT TAKES

Powell was asked what he will be looking at to determine when to stop and be open to a discussion on when easing might arrive and he answered by saying that “The strong view on the committee is that we will need to stay at this peak for some time until inflation clearly comes down.”

He went on to elaborate upon his views on the three main drivers of inflation going forward and what has driven it of late. Powell correctly noted that goods inflation is easing in the last couple of reports. He repeated what he has previously said in noting that the next phase is when Owners’ Equivalent Rent starts to ease which takes a while next year as OER catches up to waning market measures of leases to flow through but that OER is still expected to remain hot for some time next year as prior contracts at lower rates get re-worked.

Then Powell dropped the money quote on inflation. He’s not impressed by easing goods inflation or the prospect for OER to ease and requires that the half of the inflation basket that is represented by core service price increases has to ease up. He argued this requires softer job markets and noted that services inflation is “the biggest part of our inflation forecast.” He noted that “Services inflation may not move down and so we will have to raise rates higher to achieve this.”

Powell also rejected any focus upon pricing rate cuts and said it’s not their focus at this point while history cautions against prematurely easing. He said that the Committee won't see rate cuts until it sees inflation sustainably moving toward 2% (ie: not just the first time, but sustainably). The reader probably realizes he can’t say anything but this at such a tenuous stage without sparking a pile-on into premature cut bets.

Overall, the message here was that Powell welcomes two soft core CPI prints but is looking through them as transitory improvements in goods price inflation.

RECESSION INEVITABLE?

When asked whether the FOMC’s projections are consistent with expecting a recedssion, Powell said “I wouldn’t say that at all. Growth of 0.5% next year in our forecasts is a positive trend. Our projection for a 4.7% UR (actually 4.6 I think...) does not sound like a labour market where a lot of people will have to be put out of work.

FURTHER DOWNSHIFTING?

When asked whether the FOMC would be more comfortable probing where the terminal rate is by now shifting to quarter-point hikes, Powell at first said “I can’t tell you that today.” However, when asked once again on the question of pace he said “We're into restrictive territory and it's not so important how fast we go. It's far more important to determine how high we go and how long we should stay there.” That might be a tentative nod to further downshifting of the pace albeit depending upon data and developments.

ARE YOUR COMMUNICATIONS STALE AFTER YESTERDAY’S CPI?

Powell rejected that notion as he should have. He noted the well understood point among Fed watchers that SEP projections presented on game day are always made on the basis of the best information. He's noting that it's never the case they don't reflect important information that arrives on the first day of the meeting since members can re-submit forecasts into the evening of the first day of the two-day meeting (ie: last night). Mind you, he didn’t say whether anyone did!

NO MBS DISCUSSION

It was a low probability tail risk in any event, but no one even asked Powell to refresh his views on MBS roll-off given the slower than targeted pace in light of developments in bond and mortgage markets this year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.