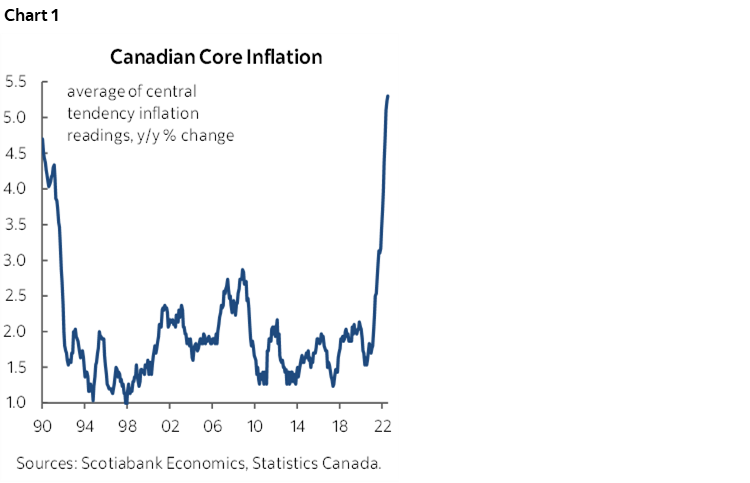

- Average core inflation continues to climb…

- …and put further pressure on the BoC…

- …to move into restrictive territory with another +75bps move

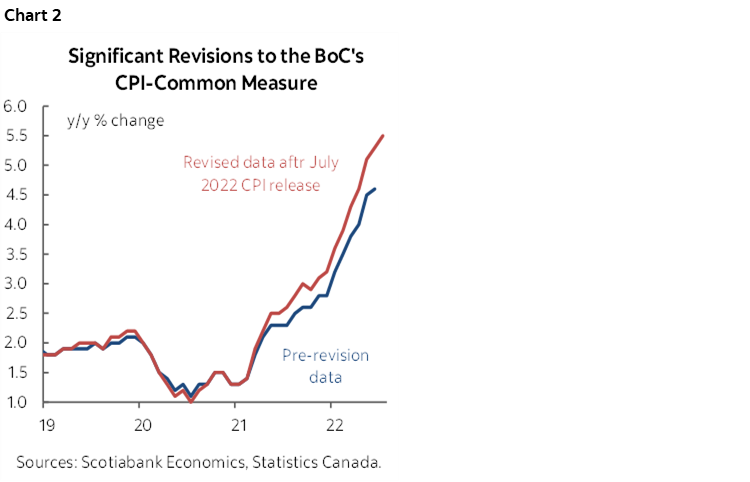

- Large, ongoing revisions to common component CPI…

- …keep raising average core inflation estimates…

- …and question the usefulness of the measure

- CDN CPI m/m % NSA // y/y %, July:

- Actual: 0.1 / 7.6

- Scotia: 0.4 / 7.8

- Consensus: 0.1 / 7.6

- Prior: 0.7 / 8.1

- Average ‘Core’ CPI: 5.3% y/y (5.2% prior, revised up from 5.0%)

Core inflation continues to creep higher to new records each month as inflationary pressures rise and broaden (chart 1). That lends itself toward expectations for another large hike of 75bps at the September 7th meeting that is mostly but not fully priced in OIS markets.

I think the market reaction was generally sensible. GoC two-year yields have climbed about 10bps and the C$ appreciated by about a quarter of a cent on a USDCAD basis. The new information incrementally reinforces a strong tightening bias.

The Bank of Canada won't care about the headline softening. They'll be more concerned about ongoing upward pressure upon core measures. The data lends itself to a 75bps move on September 7th that would bring the policy rate closer to being in very mildly restrictive territory given estimates of the neutral policy rate range of 2–3%. Unlike the Fed, there isn't much on the agenda between now and then that could be incrementally impactful. This is the last CPI reading before that meeting and the next jobs report arrives two days after the decision. Plus, the September meeting is a statement-only affair with a day-after presser to be hosted by an as-yet undisclosed Governing Council member, sans forecast (unlike the Fed that will also update the SEP in September but on the 21st and hence after the BoC). There are no scheduled BoC speakers between now and the blackout period that commences one week prior to the decision.

IS COMMON COMPONENT CPI OF ANY USE?

Average ‘core’ inflation—an average of the three central tendency measures—moved materially higher to 5.3% and with the prior month revised up two-tenths to 5.2% y/y. The prior month’s revision is because they keep messing with common component CPI that was revised up from 4.6% to 5.3% which is large. This issue is worth exploring further before turning toward other details.

The challenges with common component CPI run much deeper. Chart 2 shows the impact of cumulative upward revisions to this measure dating back to May 2021. The original reading for January 2022 was 2.3% y/y and cumulative revisions have taken that up to 3.6 which in the world of inflation estimates is huge. For February it’s now 3.9% versus the 2.6% original reading. For March it’s 4.3% versus 2.8, for April it’s 4.6% versus 3.2% and for May it’s 5.1% versus 3.9%.

So what’s going on here? I don’t know of another country that is messing with its core inflation readings like this while offering little useful explanation other than a remark that the black box changed again:

"In the case of CPI-common, revisions are due to the statistical technique used, as the factor model is estimated over all available historical data."

Wonderful, just sweep it under the rug. One possible explanation is that common component CPI has been getting revised higher as the mean and variance of headline CPI have been moving higher which serve as model inputs to the constantly re-estimated common component CPI inflation factor model. This raises the issue of how useful a measure of ‘core’ inflation is if it simply follows headline CPI in lagging fashion through model revisions. I’m unsure of the degree to which this explanation is valid for chronic upward revisions and so there should be further explanation offered by either StatCan or the Bank of Canada if they wish this measure to have any credibility with market participants and policymakers especially since there is still a segment of market opinion that (wrongly imo) believes the BoC pays more attention to common component CPI than the other measures.

In the meantime, I would advise placing greater emphasis upon other core readings like trimmed mean (5.4% y/y), weighted median CPI (5.0% y/y), and simpler measures dating back to before the BoC over complicated things to no apparent benefit with its central tendency gauges.

The hot core readings are also seen in simpler gauges and there remains an ongoing case for sticking with those gauges in keeping with many other countries. Simple CPI ex-food-and-energy was up 6.1% m/m SAAR which picked up from 5.2% the prior month. CPI excluding the 8 most volatile items was up 5% m/m SAAR and matched the prior month’s estimate. CPIX was up 5% m/m SAAR from 5.9% the prior month. In all of these cases, the rates have cooled from their peaks in March when the economy was reopening from omicron restrictions, but they are all vastly higher than the BoC’s 2% headline CPI target over the medium-term that uses the core readings as an operational guide. The fact that these m/m SAAR core readings are still running at the hot rates that existed on a trend basis before omicron reopening effects should give little to no comfort to doves.

OTHER DETAILS

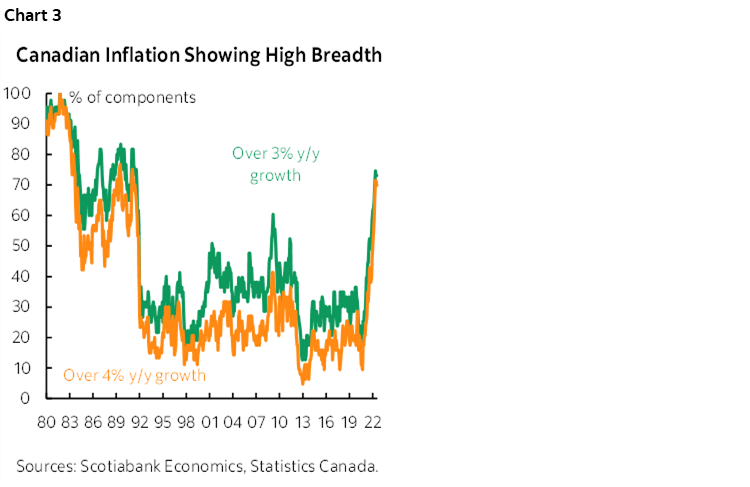

Breadth remains very high (chart 3).

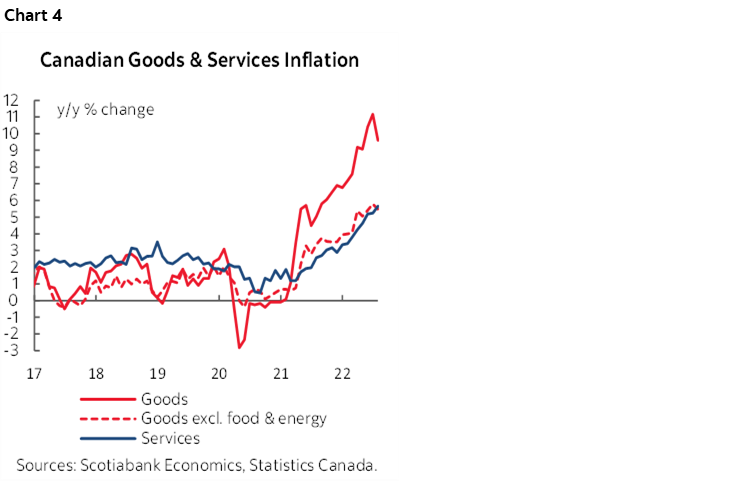

Both services and core goods inflation continue to push higher (chart 4). The driver of weaker all-in goods inflation is weaker commodities, but underlying inflationary pressures remain hot.

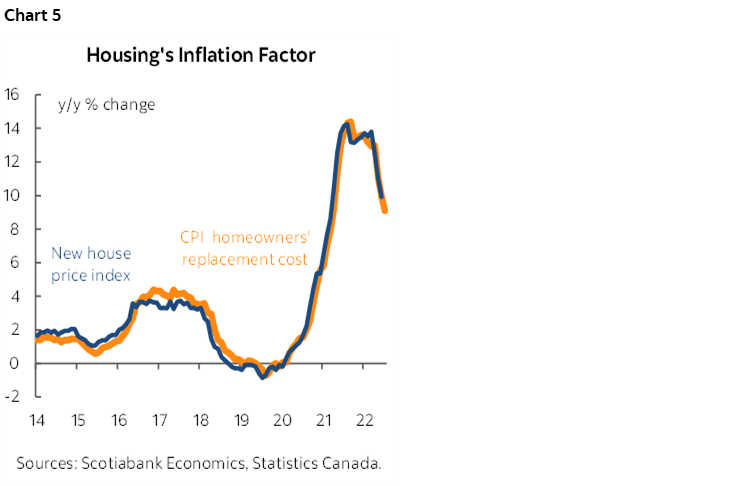

Chart 5 shows that housing is cooling as an inflationary driver, at least the way it’s captured in Canada. Canada captures housing inflation using the house-only component of builder prices (ie: ex-land) as a driver of homeowners’ replacement cost and builder price inflation has been ebbing. Canada does not use owners’ equivalent rent like the US BLS does.

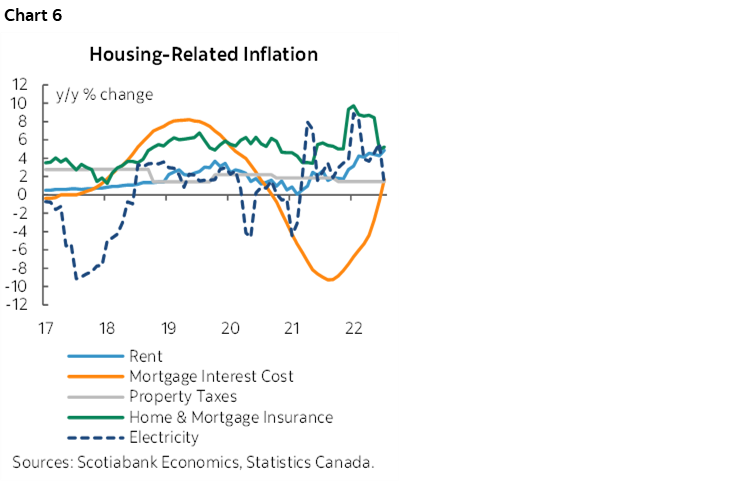

Chart 6 shows other housing-related contributions to CPI inflation. Mortgage interest cost is rising with rate hikes and with much greater upward pressure forthcoming from this reading, but the BoC clearly looks through the directly measured effects of their rate hikes on inflation. Rent has cooled at least for now, but weakening housing markets may keep upward pressure upon this component. Housing’s influences upon CPI inflation nevertheless run much deeper given direct and indirect effects not well captured by just looking at builder prices.

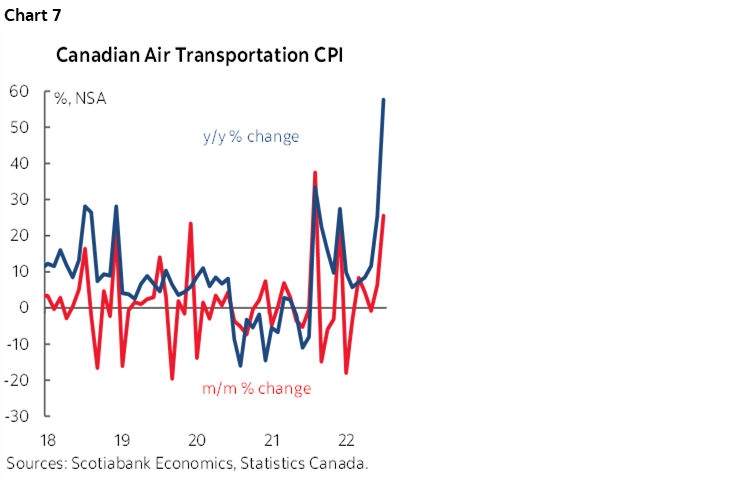

Across other components, airfare continues to soar (chart 7).

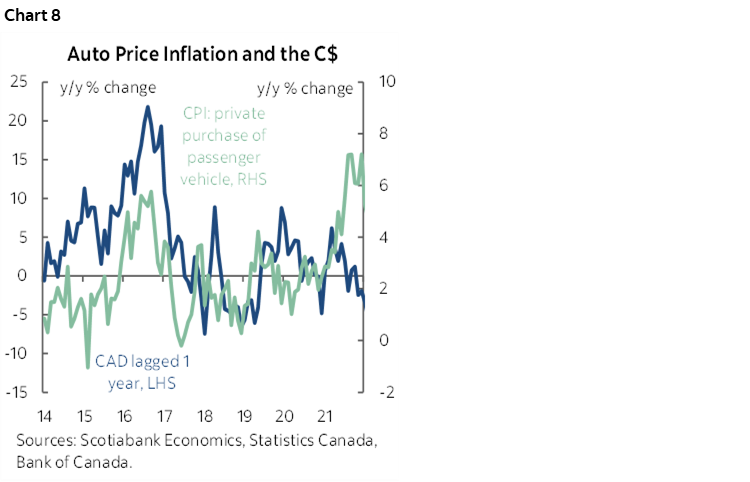

Auto price inflation remains disconnected from CAD changes because of supply chain issues that have made it a seller’s market (chart 8), but even if supply chain issues continue to gradually improve the next upward leg could come from the lagging effects of CAD weakness upon the next couple of years of new models introduced around late summer into the Fall.

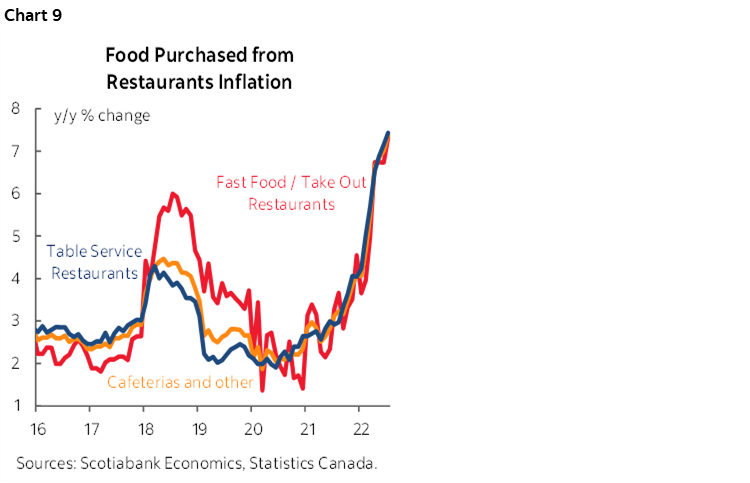

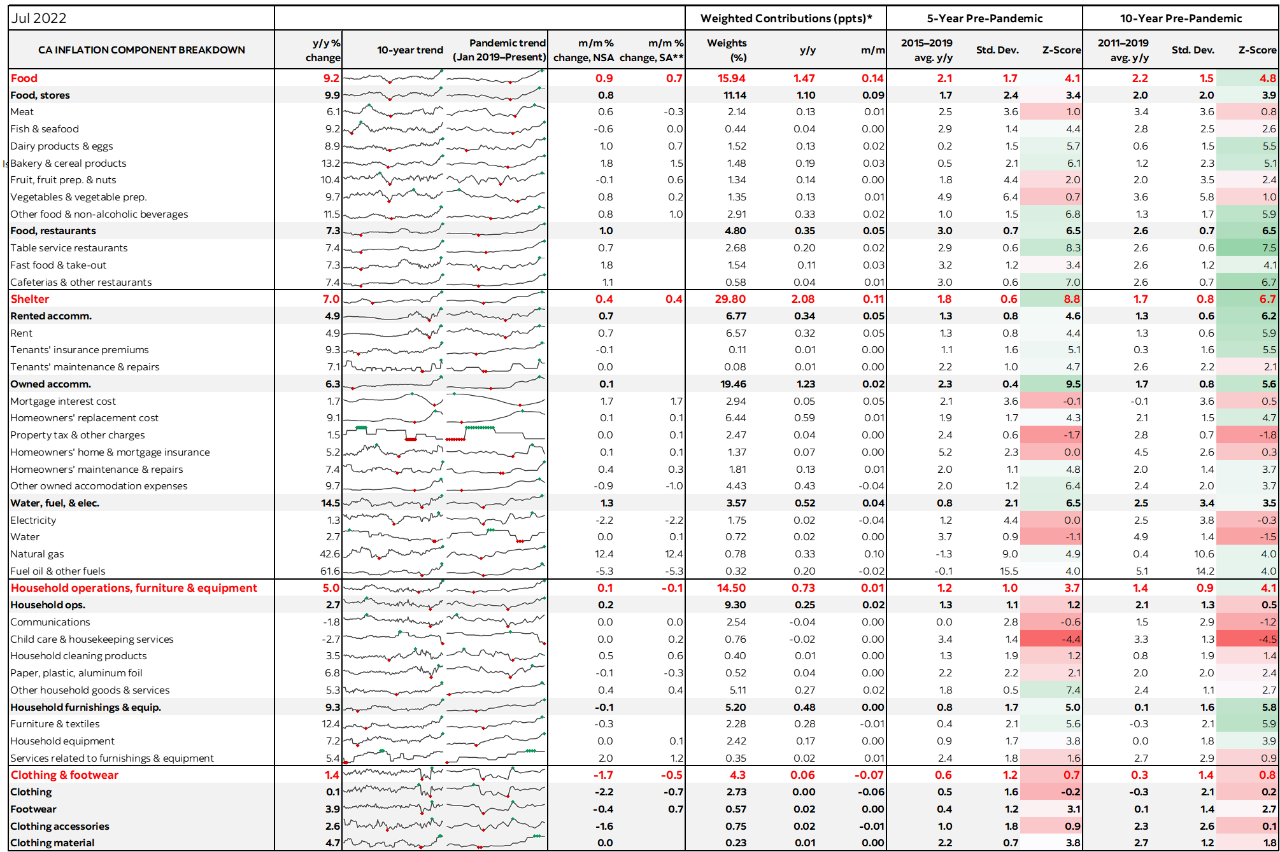

Food inflation remains hot (chart 9).

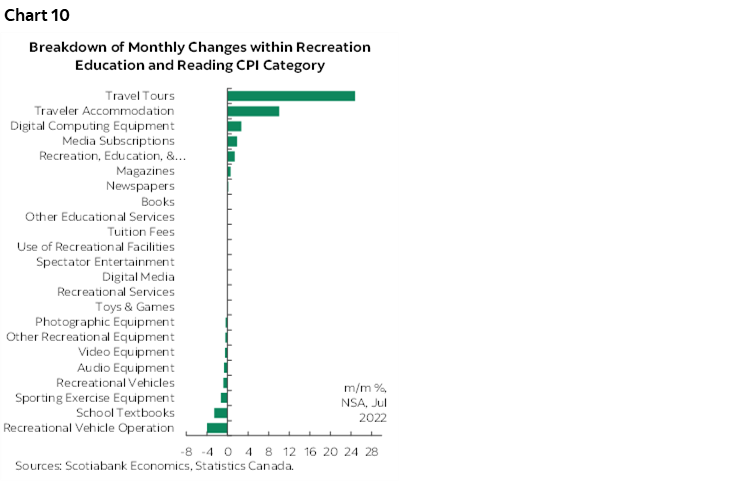

The recreation/reading/education category saw big gains in travel-related categories (chart 10).

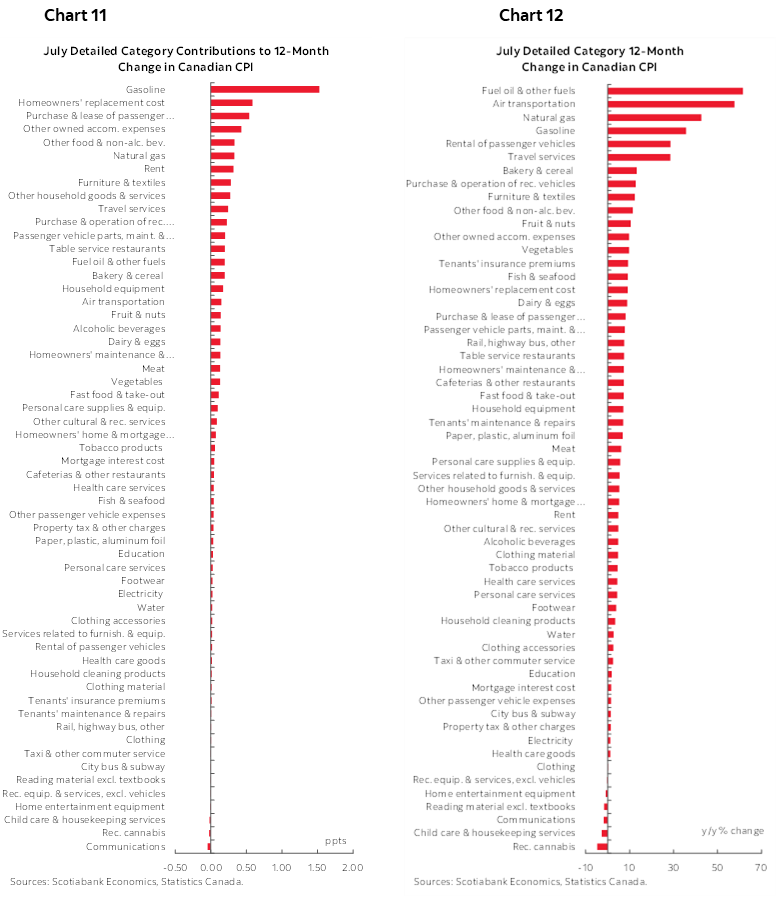

Chart 11 shows a breakdown of the CPI basket in y/y terms and chart 12 does the same thing but in terms of weighted contributions to inflation by category.

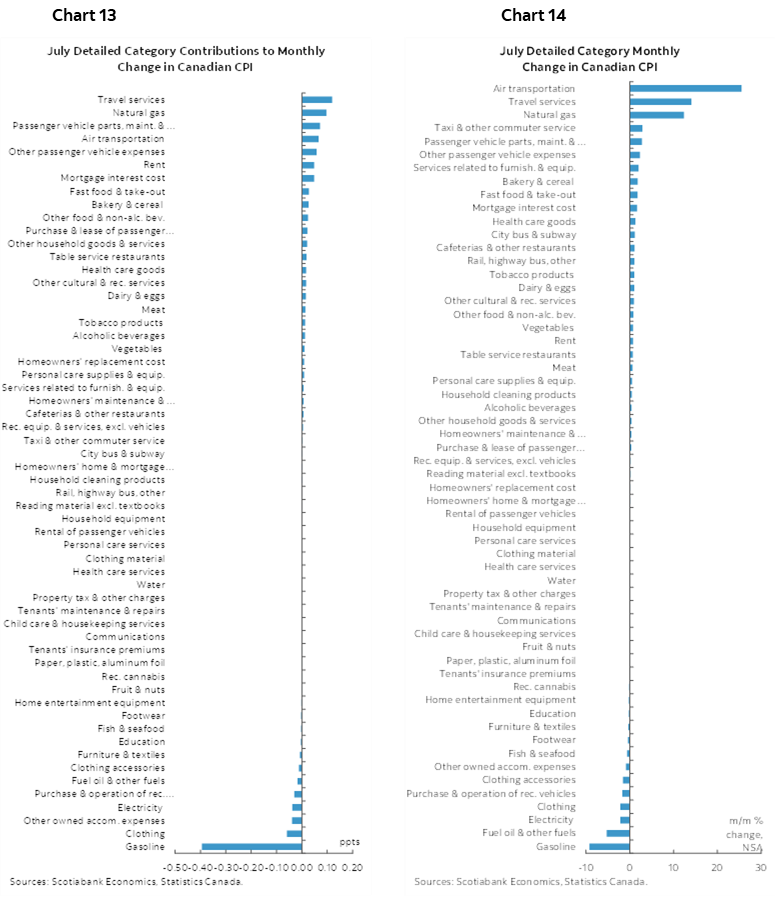

Chart 13 shows a breakdown of the CPI basket in m/m NSA terms and chart 14 does the same thing in terms of weighted contributions.

Please also see the accompanying table that provides a detailed breakdown of the basket including various other measures and micro charts.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.