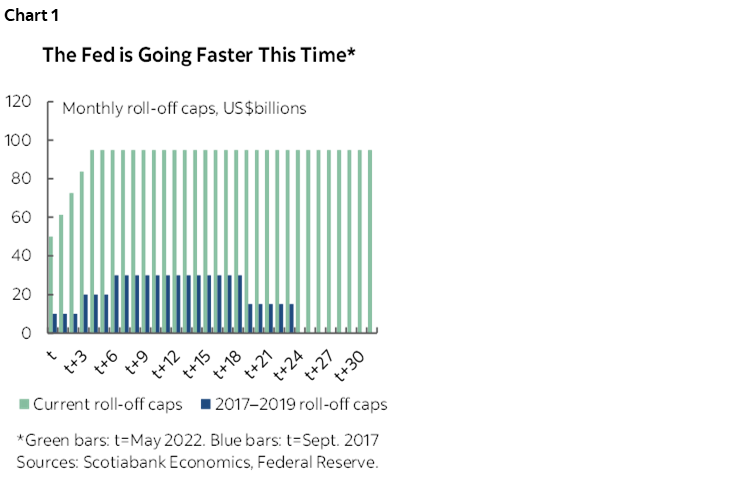

- Roll-off caps will rise to US$95B within about three months, likely starting in May

- That is more than triple the rate in 2017–19

- The Treasury/MBS composition will be similar to 2017–19

- Committee members want to get to a neutral policy rate “expeditiously”

- Outright MBS sales are possible

- The Fed will feel the way toward optimal reserves and when to end roll-off….

- ...as it evaluates market conditions alongside the new Standing Repo Facility

- Overall, markets shook it off as within the bounds of what was already priced

The grand unveiling of the FOMC’s plans to shrink the Fed’s balance sheet came and went with markets hardly even batting an eye. Market moves across two-year and ten-year Treasury yields, the dollar and stocks were all very minor. The FOMC is likely to be rather pleased with this outcome given its emphasis upon communicating in advance and trying as much as possible to minimize abrupt surprises.

The reason for such minor moves is probably because a) the plans could have been more aggressive than what was likely anticipated and priced in advance and b) there are open questions left unanswered in some key respects and intentionally so.

Most of the takeaways are drawn from page 4–5 in the section of the minutes to the March 15th–16th meeting (here) titled “Plans for reducing the size of the balance sheet.” They include the following points.

1. The FOMC will phase-in a planned pace of balance sheet reduction at a roll-off rate of maturing securities not replaced by reinvestment equal to a peak of US$95B per month capped within about three months after commencing or maybe a touch longer. They will likely start in May given guidance that they are “well placed” to begin doing so “as early as after the conclusion of the upcoming meeting in May.” This cap is roughly middle of the road compared to the range of guesstimates across shops. Above this cap will see the maturing amounts being bought in the open market in order to control the pace of decline in holdings.

2. They did not specify a starting amount. This ceiling is more than three times higher than the maximum rate of roll-off that was pursued over the 2017–19 period when it peaked at US$30B/month. The speed with which the FOMC gets up to this maximum rate of roll-off will be considerably faster than in the 2017–19 period when the Fed took three calendar quarters to get up to the maximum pace of roll-off. Chart 1 compares the plan this time around with the prior period.

3. The composition of the peak roll-off cap will be US$60B/month for Treasuries and US$35B for MBS upon full implementation. That is very close to the 60–40 split between roll-off amounts of Ts and MBS in 2017–19.

4. The caps are roughly in the middle of the road in terms of the range of estimates.

5. No one should be surprised by "many" FOMC officials advocating a 50bps move in May if they've been listening to Powell & Co. over recent weeks.

6. The minutes flagged that there could be "one or more" 50bps moves which might mean a slightly faster pace to what is priced.

7. The Committee guided that they wish to get to a neutral rate "expeditiously" but that is probably already priced given that fed funds futures are already there within about 9 months versus taking 2 years the last time around.

8. Outright sales of MBS are possible once unwinding is "well underway" so they're signalling they'll reduce the holdings one way or another through roll-off and/or sales. The relevant passage is as follows: "Participants generally agreed that after balance sheet runoff was well under way, it will be appropriate to consider sales of agency MBS to enable suitable progress toward a longer-run SOMA portfolio composed primarily of Treasury securities. A Committee decision to implement a program of agency MBS sales would be announced well in advance."

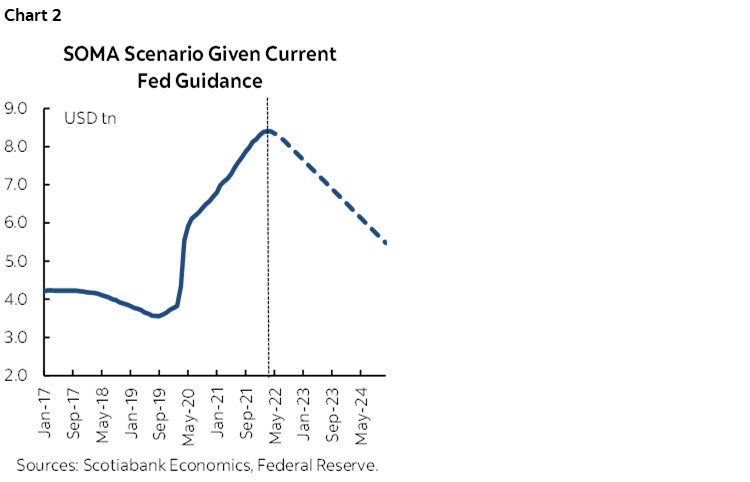

Chart 2 shows an attempt at projecting the size of the SOMA portfolio over time at this pace of roll-off. Recall that the starting point for the Fed’s SOMA portfolio was just under US$4T before the pandemic versus US$8.4 trillion now. Even by 2025 the SOMA account would still be materially bigger than before the pandemic unless asset sales are used to expedite shrinkage. This projection not only assumes an unwavering pace of roll-off but also no outright asset sales.

So why did markets largely shake off the minutes? For three main reasons.

1. These minutes could have been materially more hawkish. They walk down the middle of the road compared to how pricing had already adjusted to pricing future Fed hikes and the wide range of roll-off estimates across shops.

2. Absent was any discussion of outright Treasury sales. Only MBS sales were guided as a possibility later on down the road.

3. One key thing is the vague discussion around optimal reserves. They are wary of repeating what happened the last time and now avoiding any references to the end goal for the targeted SOMA portfolio and reserves. They are just saying this time that they'll monitor money market conditions which will be relied upon to reveal stresses around optimal reserves if they shoot beneath (ie: we'll know it's enough when we get there! not very comforting...).

Further on this last point, a couple of participants are also indicating that the Standing Repo Facility makes for a potentially different ballgame in that regard this time around which I think is true. It removes guesswork around when, how much, at what price etc the NY Fed's open markets desk would intervene around a liquidity shock. Others treated this as contentious in that the SRF was not originally intended to be a substitute for optimal reserves, though it may turn out to be.

In other words, they are noncommittal toward the length of time they will reduce at a US$95B/mth pace and hence noncommittal toward the optimal size of the SOMA portfolio of Treasury, MBS, T-Bill and TIPS holdings, and the optimal size of reserves in the system. That's likely a sensible approach. A plethora of uncertainties would make any firmer guideline entirely arbitrary and potentially with adverse consequences.

Finally, there was no discussion around estimates of equivalent rate effects. The Fed’s primary policy tool will remain the policy rate itself, but there is a vibrant debate around how the pace of unwinding the balance sheet may impact Treasury yields and the equivalent effect of such moves measured in terms of the number of Fed rate hikes. See this morning’s Daily Points for a discussion of the uncertainties around this topic.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.