Canadian retail sales are ~8½% above pre-pandemic levels

Canada and the US are enjoying full retail recoveries

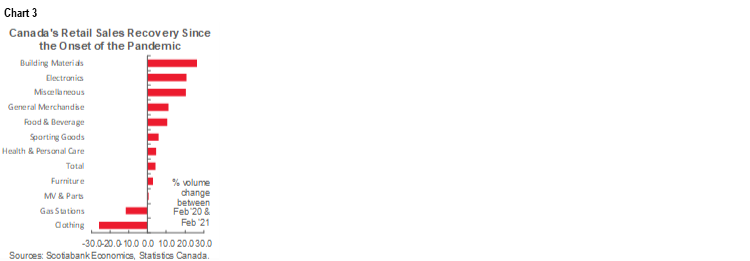

Few retail sectors are still being left behind

February sales beat, March guidance points to further growth

Q2 sales have ‘baked in’ 12% growth over Q1

April/May restrictions will likely knock back that tracking…

…before reopening and vaccines should drive renewed gains

Canadian retail sales, m/m % change in headline /ex-autos, SA, February with March guidance:

Actual: 4.8 / 4.8

Scotia: 4.0 / 2.5

Consensus: 4.0 / 3.5

Prior: 0.0 / -0.1 (revised up from -1.1 / -1.2)

Advance March guidance: +2.3

Canadian retail sales surprised higher on a combination of three factors. One is that the advance guidance for February was revised up. Two is that there were significant revisions dating back to the start of the pandemic. Three is that advance guidance for sales during March was stronger than I had thought it might have been.

The full recovery in aggregate retail sales continues to transition toward outright expansion of the sector (chart 1). Canada’s retail recovery is tracking in similar fashion to the US experience (chart 2). The value of total Canadian retail sales now stands 8.4% higher than where it was in February 2020 just before the pandemic struck. By comparison, US retail sales are 17% higher than February 2020.

Chart 3 shows the somewhat uneven breakdown by sector. Most retail sectors are into outright growth mode with sales higher than they were before the pandemic. Gas and clothing sales are two exceptions which likely makes sense given work from home.

Personally I still think it’s a mistake for monetary policy to focus upon the composition that is still leaving behind some types of spending rather than focusing upon the broad totals. Ditto for jobs if the hope for a rebound to February 2020 employment levels later this year comes to fruition.

February’s advance guidance that indicated sales would be up 4% based upon an incomplete sample was surpassed by a 4.8% tally with the full sample.

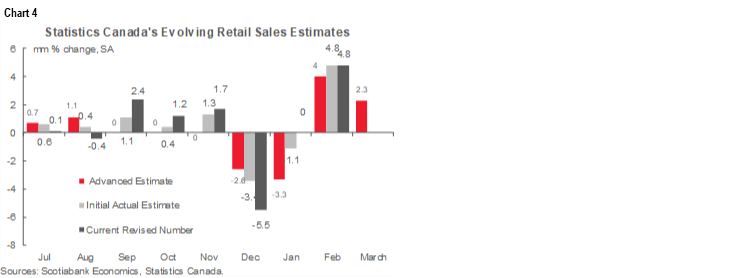

Revisions that stretched back over multiple months had a particularly powerful effect on January. Recall that January started off with ‘flash’ guidance for a 3.3% m/m drop until the fuller sample indicated a drop of 1.1% m/m. Today, StatsCan revised that up to a flat reading for a swing of over three percentage points compared to the initial guidance which needless to say is breathtakingly large for a single month. Chart 4 shows the history of StatsCan’s advance guidance initial estimates and current ‘final’ estimates.

Then along comes advance guidance for March sales that we’re told are tracking a 2.3% m/m gain. We’ll see what that ultimately looks like, but for now, it indicates that continued reopening effects through March buoyed the sector.

Of course we all know that April brought with it tighter restrictions because of the third wave of COVID-19 cases. That is likely to dampen the enthusiasm somewhat, but not necessarily for Q2 overall. That depends upon whether the COVID-19 curve bends enough and restrictions ease later and upon continued vaccine progress. It also depends upon whether consumers and retailers continue to find ways to spend and meet demand through online sales, home deliveries, curbside pick-up and limited traffic.

In fact, chart 5 shows tracking of quarter-over-quarter growth in retail sales volumes and how Q2 growth is likely to accelerate. Q1 slipped with sales volumes down by 1.75% q/q despite the strength over February and into March and that was because of the way momentum was lost over Q4 heading into the start of Q1 only to be partly made up by the way Q1 ended. Now the momentum argument points in the other direction by guiding a ‘baked in’ estimate for 12% q/q annualized and seasonally adjusted growth in sales volumes during Q2 assuming zero monthly change in volumes in each of April, May and June in order to focus upon the effects of what we know so far. Sales volumes accelerated during Q1 and transitioned into Q2 at a high level. There could still be powerful growth in sales volumes during Q2 even if April brings a setback. Further, if restrictions ease into the end of Q2 then it’s possible the quarter exits on a high note, but we’ll need to monitor the COVID case and vaccine curves for that.

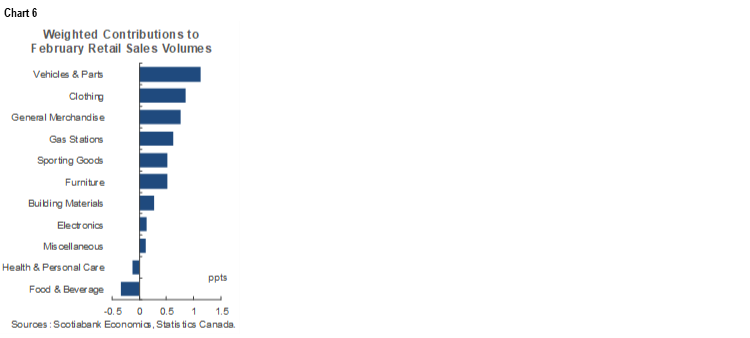

Chart 6 shows which sectors drove the sales gain during February over January in terms of weighted contributions to overall growth. Multiple sectors played a role in driving strength. We won’t get the break down of the flash guidance for March until the next report.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.