- Solid job growth exceeded the fear factor…

- ...but fell short of expectations after removing ‘soft’ categories

- Long-term unemployment continues to rise

- Absent job openings and amidst diminishing gains…

- ...the next phase for a job recovery is more uncertain

U.S., Change in Non-farm Payrolls SA (m/m 000s) / UR (%) / y/y wage growth (%), August:

Actual: 1371 / 8.4 / 4.7

Scotia: 1500 / 9.8 / 4.5

Consensus: 1350 / 9.8 / 4.5

Prior: 1734 / 10.2 / 4.7 (revised from: 1763 / 10.2 / 4.8)

US job growth was weaker than expected primarily after subtracting the transitory role of Census 2020 hiring and temp help positions. Having regained 1.37 million jobs in August is a positive, but it was really only a gain of 1.03 million net of these two forms of ‘soft’ gains. Still, the gain exceeded market concerns to the extent to which ‘whisper’ numbers are reliable.

While still respectable, that makes this the weakest month for payroll gains in the four-month recovery to date. In light of the high degree of integration of the North American economy that portrays US and Canadian workers as sisters and brothers in arms despite the politics, we have evidence in place that points toward how further job gains after an initial reopening spurt are going to be more uncertain on both sides of the border (also see here).

The market reaction was mixed. The US 10 and 30 year Treasury yields rose by about 4–6bps and the curve re-steepened after flattening of late. The USD appreciated by about 0.4% on a DXY basis. Stocks liked the tally at first as S&P futures gained a touch, but selling resumed into the cash market open perhaps as the waning momentum angle sank in on a second take. Tech stocks are leading decliners again. The absence of a dollar and Treasury curve response to equity selling remains intriguing.

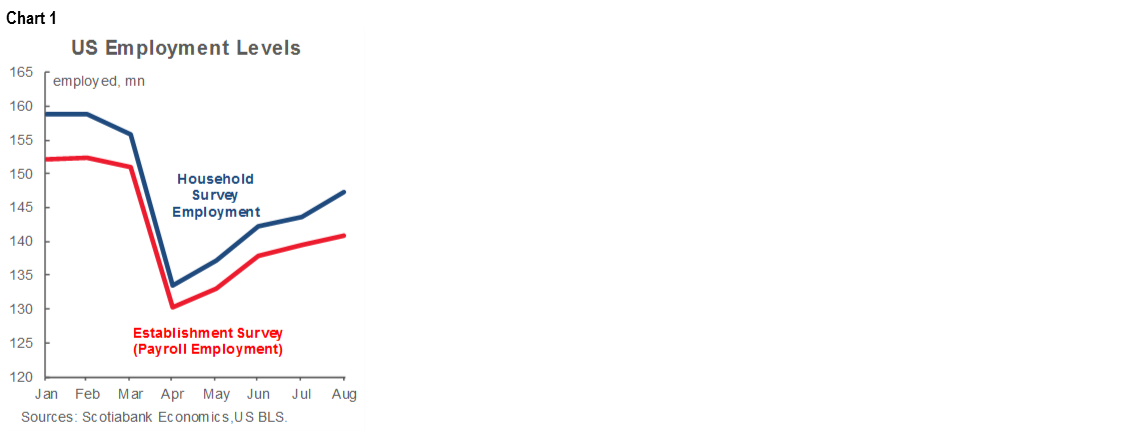

To date, the US household survey has regained 13.9 million jobs out of the 25.4 million drop that had occurred by April for a 55% recovery rate. Using nonfarm payrolls, 10.6 million out of the 22.16 million lost jobs have been regained for a 48% recovery rate. Methodological differences and the household survey’s inclusion of non-payroll small business jobs explain the difference. See chart 1.

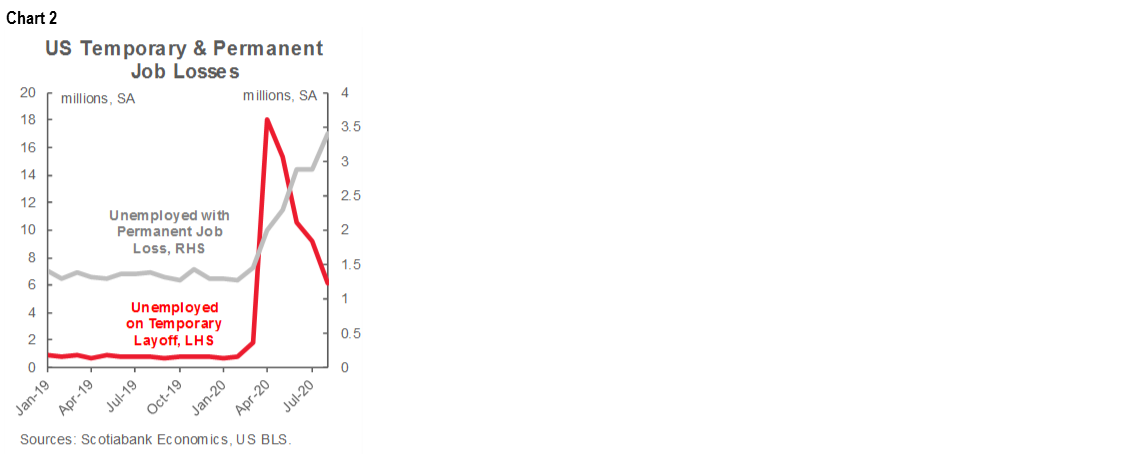

Chart 2 demonstrates the rising burden of long-term unemployment. The number of folks who are unemployed with no prospect of being called back continues to rise and is just under 3 ½ million Americans. The unemployed who are on temporary layoff continues to decline toward 6 million which is one-third of the peak and primarily due to regaining employment followed by switching to longer term unemployment.

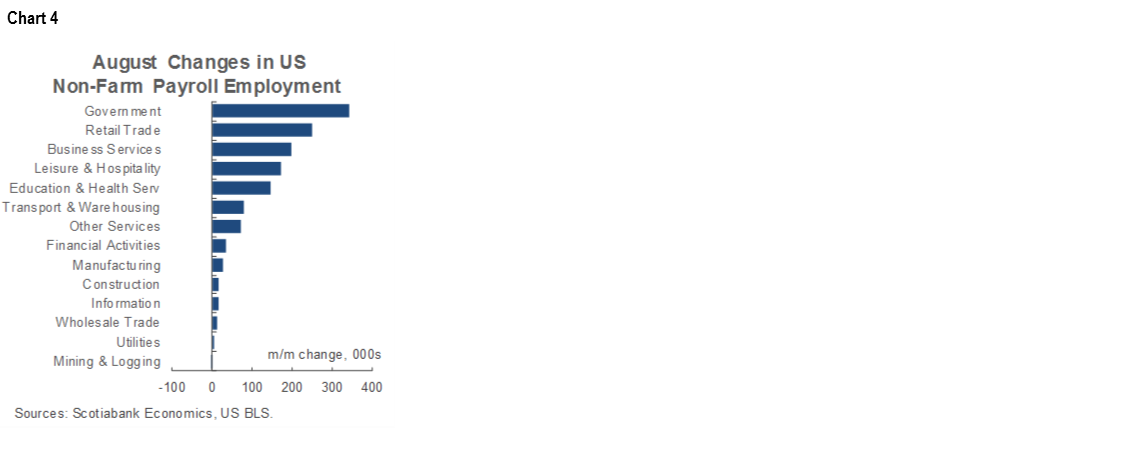

Government hiring was up by 344k including 251k by the Federal government and 93k across all other levels of government skewed toward local governments. Federal hiring was up because of a 238k increase in temporary Census 2020 jobs.

That an inflection point is arriving is reinforced by the updated chart 3. The number of unemployed Americans is falling but remains much higher than job openings. The debate going forward is how the labour market will transition from call backs of furloughed workers toward regaining lost jobs.

There was solid breadth by sector as every broad industry registered gains (chart 4). Service industries added 984k while the goods sector was up by 43k. Within goods, there was a 29k gain in manufacturing jobs and a 16k rise in construction jobs. Within services, trade/transport was up 341k including 249k in retail. Business services added 197k but temp help account for just over half of that (+107k). Leisure and hospitality sectors were up 174k. Education and health sectors added 147k. The financial sector was up 36k and IT added 35k jobs.

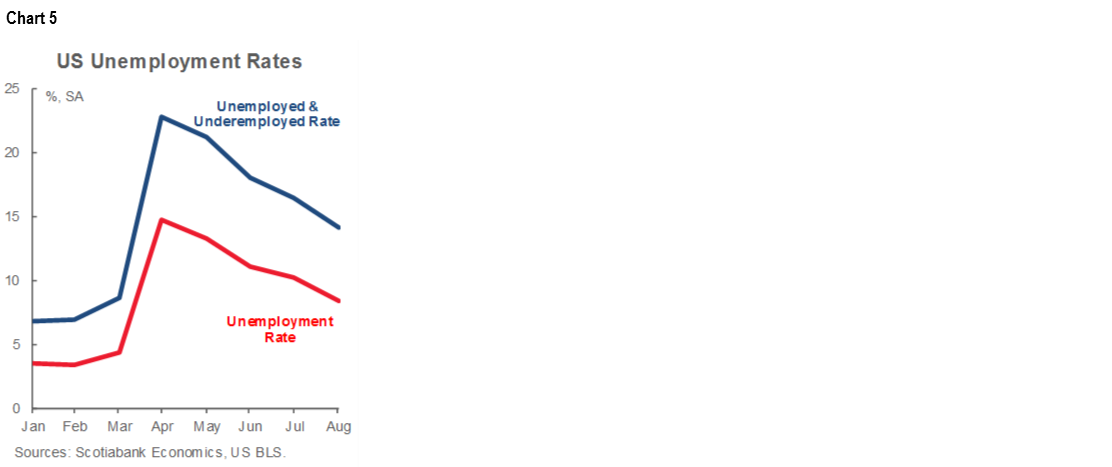

The unemployment rate fell more than expected to 8.4%. It is derived from the companion household survey that registered a job gain of 3.756 million that far eclipsed the labour force change of 968k. The labour force participation rate climbed by three-tenths to 61.7% but it remains 1.7 percentage points below the February level.

The U6 measure of unemployment and underemployment declined by 2.3 percentage points but remains at 14.2% (chart 5). Still, that’s a decline of 8.6 percentage points since April.

Average hourly earnings held steady at 4.7% y/y but were up +0.4% m/m. The compositional effect of the shift in employment makes this reading difficult to interpret by way of true momentum that likely remains considerably softer.

Total hours worked were up by 1.2% m/m. They remain 7.7% lower than the pre-pandemic level in February.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.