Q3 is still tracking a massive rebound in sales volumes

A strong preliminary reading for August…

…helps to downplay concerns the consumer lost momentum

Conflicting forces will guide the way forward into the holiday shopping season

CDN retail sales m/m % change, headline / ex-autos, SA, July:

Actual: 0.6 / -0.4

Scotia: 0.7 / 0.5

Consensus: 1.0 / 0.5

Prior: 23.7 / 15.7

August guidance: +1.1 m/m

Canadian consumers are keeping the recovery alive. Retail sales grew in line with advance guidance for July and early guidance for sales in August was strong. In fact, if August guidance confirms slowing, then ship it in because at this pace I’ll take slower any day. Softness in core sales during July was likely a function of distortions affecting a handful of categories rather than more fundamental concerns.

July sales growth of 0.6% m/m was similar to the guidance provided by Statistics Canada on August 21st when they indicated July would rise by 0.7% and it was in line with my estimate. August advance guidance of 1.1% m/m in the total value of retail sales would be considered a robust gain in any non-pandemic year. Most of that August gain was likely driven by higher volumes because we know that August CPI was only up by 0.1% m/m SA in terms of both headline and ex-food and energy although there was a little firmer price pressure in more retail-oriented categories.

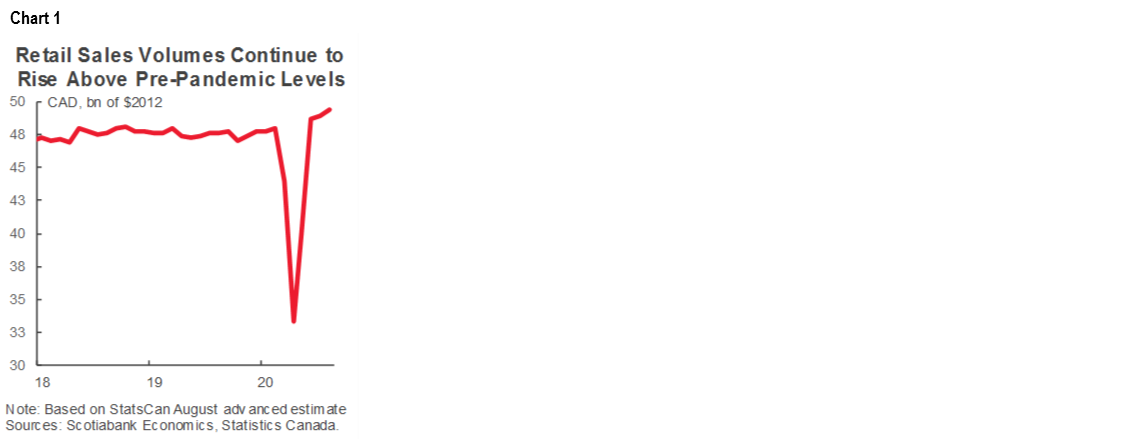

Sales volumes continue to move above pre-pandemic levels as the retail sector in aggregate has witnessed a full recovery and then some (chart 1). That not all types of spending and channels have rebounded is true, but should not cloud one’s understanding of the sector’s overall rebound.

Q3 is tracking a very strong rise (chart 2). After a 42% q/q annualized drop in retail sales volumes in Q2 over Q1, Q3 is tracking a gain of 115% q/q SAAR. This assumes most of the August advance guidance was volume-driven and that September will be flat just to focus the math on the effects of what we know about Q2 and Q3 so far.

We don’t have any details to go with the advance guidance for August. As for July’s softness in sales ex-autos, I think that’s explainable. Much of the softness came through building materials and garden equipment stores (-11.6% m/m), groceries (-2.1% food/beverage) and sporting/hobby stores (-8.8%). They are not bad reasons for softness. Seasonal adjustments might be messed up by the fact that pandemic hording likely brought forward food buying, the later Spring was distorted by closings that delayed activity at building/garden stores that delayed a spending surge that pulled forward from July and by many cancelled organized sports.

Chart 3 shows the weighted breakdown of contributions to overall growth in retail sales volumes by sector during July. In weighted terms, autos, clothing and gasoline plus ancillary sales at gas stations played the biggest roles in keeping sales growth in the black.

Other categories posted robust gains in July. Autos and parts were up by 3.3% m/m led by a 2.8% rise in sales at new car dealers but especially by an 11.5% gain in used car dealer sales with ‘other’ vehicles (atvs etc) up 3.2%. Furniture and furnishings stores saw sales going up by 5% led by a 14.7% rise in sales at home furnishings stores. Electronics and appliances were up a bit at 0.6%, clothing and accessories were up 11.2% m/m.

By province, July’s rise was skewed toward Toronto’s reopening effects that drove sales in that city up by 3.9% m/m. Manitoba saw a 1.9% rise. BC was up by 2.1% with Vancouver up 0.9%. Alberta registered a gain of 1.2%. Other provinces were either flat or, in the case of the east coast, generally lower. We don’t know the regional breakdown for August yet, but the fact it was a solid rise works against the possible interpretation of July’s numbers as simply based on, say, Toronto’s lagging reopening.

In conclusion, if the outlook following the initial off-the-charts spurt of growth as economies reopened involves settling in upon a trajectory that would be considered robust in any other year then I’ll take it. Of course the sector will slow compared to the torrid pace of recovery when the switch got flicked back on. But that doesn’t mean solid growth can’t follow in the wake of this period. We’ve forgotten that Canadians jacked up their savings to the tune of C$350 billion over the first and second quarters of this year at an annualized rate which amounted to about one-third of total consumer spending in Q2. Savings always overshoot in a shock and if the release of this pent-up demand continues then it could still mean decent growth even *if* income supports wane. The wild card, of course, is up to you in managing covid-19 risk of curtailed re-openings and other effects.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.