- Job growth smashed expectations last month…

- …as mothers returned to work with the kids back in school…

- …and reopening effects were concentrated upon youths

- Details were robust

- Why the next report faces much greater uncertainty

Canada jobs m/m change (000s) / UR (%), SA, September:

Actual: 378.2 / 9.0

Scotia: 100 / 10

Consensus: 150 / 9.8

Prior: 245.8 / 10.2

Canada’s job growth smashed expectations in September and the underlying details were broadly supportive of an overall positive tone. After I review the underlying details and progress, I’ll come back to the two dominant drivers behind why the numbers were much stronger than estimated and the connection to why I think this may be the last of the great jobs reports as October faces rising downside risk.

I think this durability question mark may be why the market reaction was very muted. The Canadian dollar shot upward by about half a cent to the US post-jobs, but this is on a day of general USD weakness and CAD is at best matching gains by others (e.g. euro, stserling) or actually underperforming the gains being registered by many others against the greenback. The rates complex was little affected by the numbers but yields on GoC bonds are slightly lower on the day in rough tandem with the US.

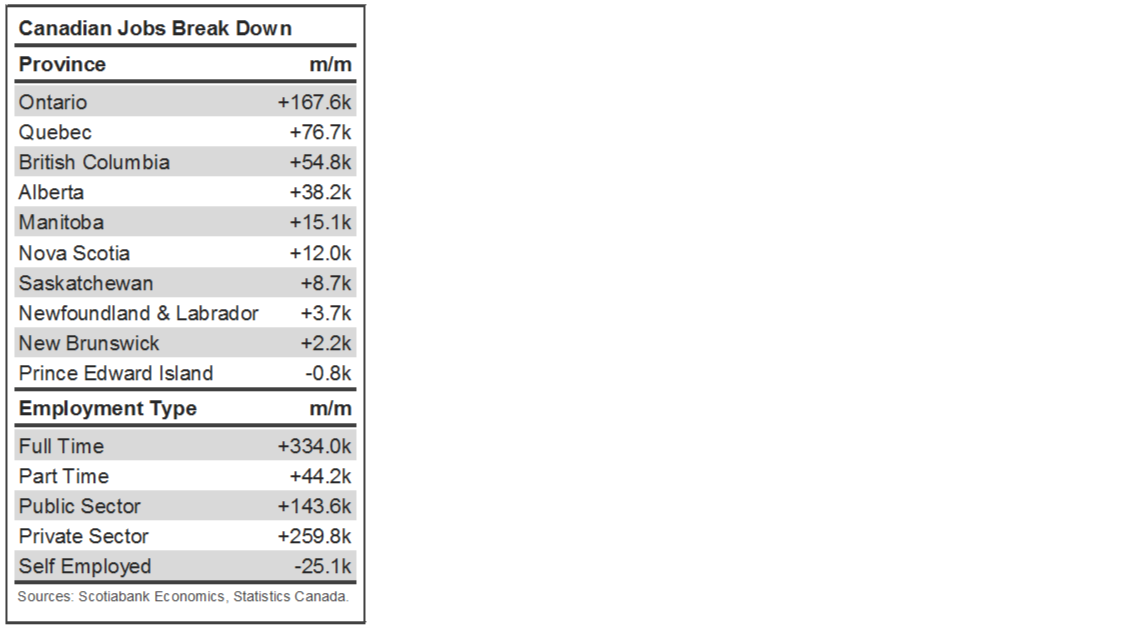

Please see table 1 that provides highlights.

As chart 1 shows, over three-quarters of jobs lost to date have been recouped. Canada is now down a net 720k jobs compared to the peak in February before the pandemic struck and has recouped 2¼ million jobs that were lost.

The unemployment rate fell by 1.2 percentage points to 9.0% from 10.2% because the 378k job gain offset an extra 164k that re-entered the labour force. As chart 2 depicts, the labour force participation rate is edging closer to where it was pre-pandemic. It increased by another 0.4 points to 65% of the population who are either employed or actively looking for work. That is only ½% lower than where the participation rate stood in February before the pandemic shutdowns.

Almost all of the gain was in full-time jobs (+334k) as part-time jobs were up by 44.2k.

Payroll jobs (+403k) drove the gain as self-employed positions slipped by 25k. Private sector payroll positions were up by 260k and public sector payroll spots were up by 144k.

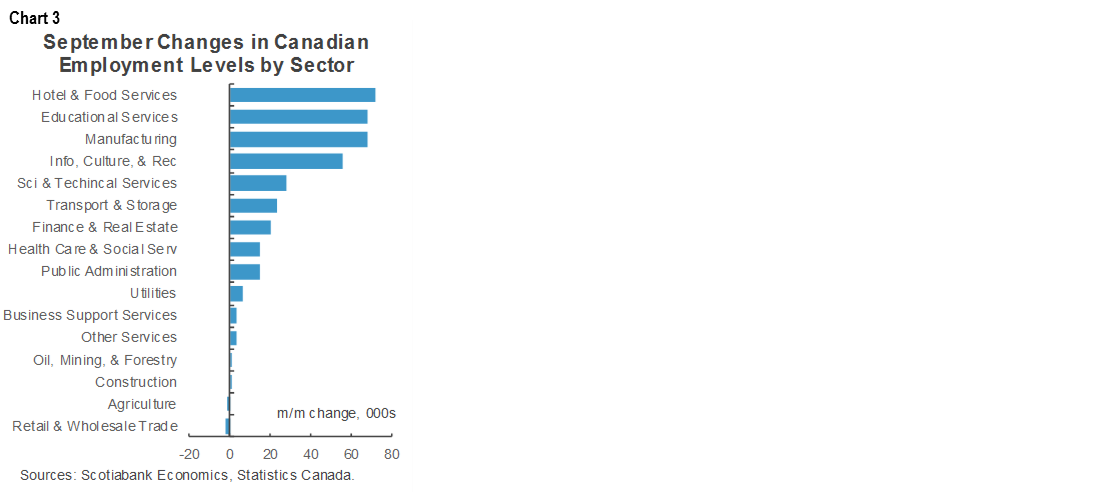

By industry, services led with a gain of 303k while goods producing sectors were up 75k. Chart 3 shows the breakdown by sector. Breadth was high as fourteen of sixteen broad sectors registered gains. Only agriculture and wholesale/retail posted trivial declines.

There was no negative effect on the Canadian education sector as was evidenced in US nonfarm payrolls. The education sector saw a gain of 68k last month.

By province, gains were led by Ontario (+168k) and Quebec (+77k) with BC (+55k) and Alberta (+38k) also posting solid increases. All provinces posted gains except for a tiny loss in PEI. I think Ontario’s large gain reflected its lagging reopening plans particularly in the country’s biggest city of Toronto compared to elsewhere.

Hours worked were up by 1.9% m/m in September which is still strong but the slowest expansion yet. Still, that was enough to drive overall hours worked up by +88% q/q at a seasonally adjusted and annualized rate in Q3. A further 9.0% annualized gain in hours worked is baked into Q4 based solely upon the way Q3 ended and the Q3 average (chart 4). So, since GDP is an identity expressed as hours worked times labour productivity with the latter being real GDP over hours worked, for the massive gain in hours worked to translate into a much lower pace of gain in GDP would have required growth in activity readings to be much lower in Q3 to offset the hours worked gain. That could well have been the case especially after taking into account inventory and import leakage effects on GDP in the quarter.

So now with the headline details out of the way, what really drove it?

Back-to-school effects on mothers and concentrated reopening effects on youth employment drove this gain in that order. Jobs for women 25–54 were up by 134k to lead the pack and the employment index for mothers in this bracket climbed to being on par with fathers for the first time in the pandemic. The report showcases the importance of school re-openings for economic livelihoods.

A major uncertainty had been whether this back to school effect would have occurred in September or been more spread out into October as mothers may have required more time to return to work once the kids were in school. With the mothers-fathers gap now shut, this suggests it all happened in September so don’t look for a repeat of this effect in October. September’s upside poses downside into October.

Youth employment (aged 15–24, both genders) was up by 127k last month. This was the second most powerful driver of the report. Youth gains likely reflected the fact that reopening effects would be more concentrated in high contact sectors upon youths, like restaurants, bars and other service sectors.

So overall, this could be the last great jobs report because the mothers and youth effects are unlikely to repeat. Going forward, there is unlikely to be an additional back to school effect in October because it all seemed to have happened in September. Further, given restrictions that Quebec, Ontario and others have introduced or are about to reintroduce (e.g. Ontario today), the youths category could be particularly vulnerable going forward. The final chart depicts the most vulnerable category of employment to increased restrictions. Over one million Canadians work in the accommodation and food services sector and almost 40% of those work in Ontario.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.