Stocks and Treasuries got a bit of a boost from the Fed’s communications today and mostly through guidance that was provided in the press conference. The S&P500 rallied an extra 0.3% following the communications to bolster a gain of about 1¼% on the day overall as a dovish sounding Fed was generally anticipated. The US 10 year yield fell by about 3bps post-Fed but clawed back over half of that into the close. The USD ended up little changed overall.

Four points are particularly worth emphasizing.

Powell said in the press conference that “we have substantially, not fully restored functioning markets” through asset purchase programs. This is interesting because some would say that market functioning has been restored and then some. Regardless, Powell is saying that the FOMC is not even at the point of shifting motives to, say, emphasizing net stimulus versus repairing markets. Thus, the first goal of boosting market functioning—and with it valuations—has not yet been achieved and that was music to the S&P500’s ears.

Second, Powell emphasized that the FOMC is concerned that the economy may be slowing but wants to see harder evidence including about the magnitude and duration of a slowing period. That indicates they are on heightened alert for downside disappointments, but for now, he also left the door open to the possibility the economy could do just fine. Powell also sloped off a question about upside risk if a vaccine emerges and said they “hope for the best, plan for the worst.” For now, markets may have taken this as a dovish bias in favour of doing more, but the obvious trade-off to risk appetite would be if the economy really does sour.

Third, Powell explicitly noted that markets should not expect the Fed to cut back on facilities or policy for a "very, very long time."

Fourth, dollar swap lines and the repo facility were extended to the end of March (here). This is consistent with Monday’s extensions (recall here) and not especially surprising in that the Fed is just extending the time period that such backstops will be in place throughout a period of heightened uncertainty. Powell explained that while they have served their purpose by restoring markets, the Fed extended them in order to facilitate planning by other central banks so they know they are still there and for as long as needed. He made a point of noting that there is nothing going on in the market that raises any concerns to motivate extensions.

Other developments are highlighted as follows.

STATEMENT ALTERATIONS

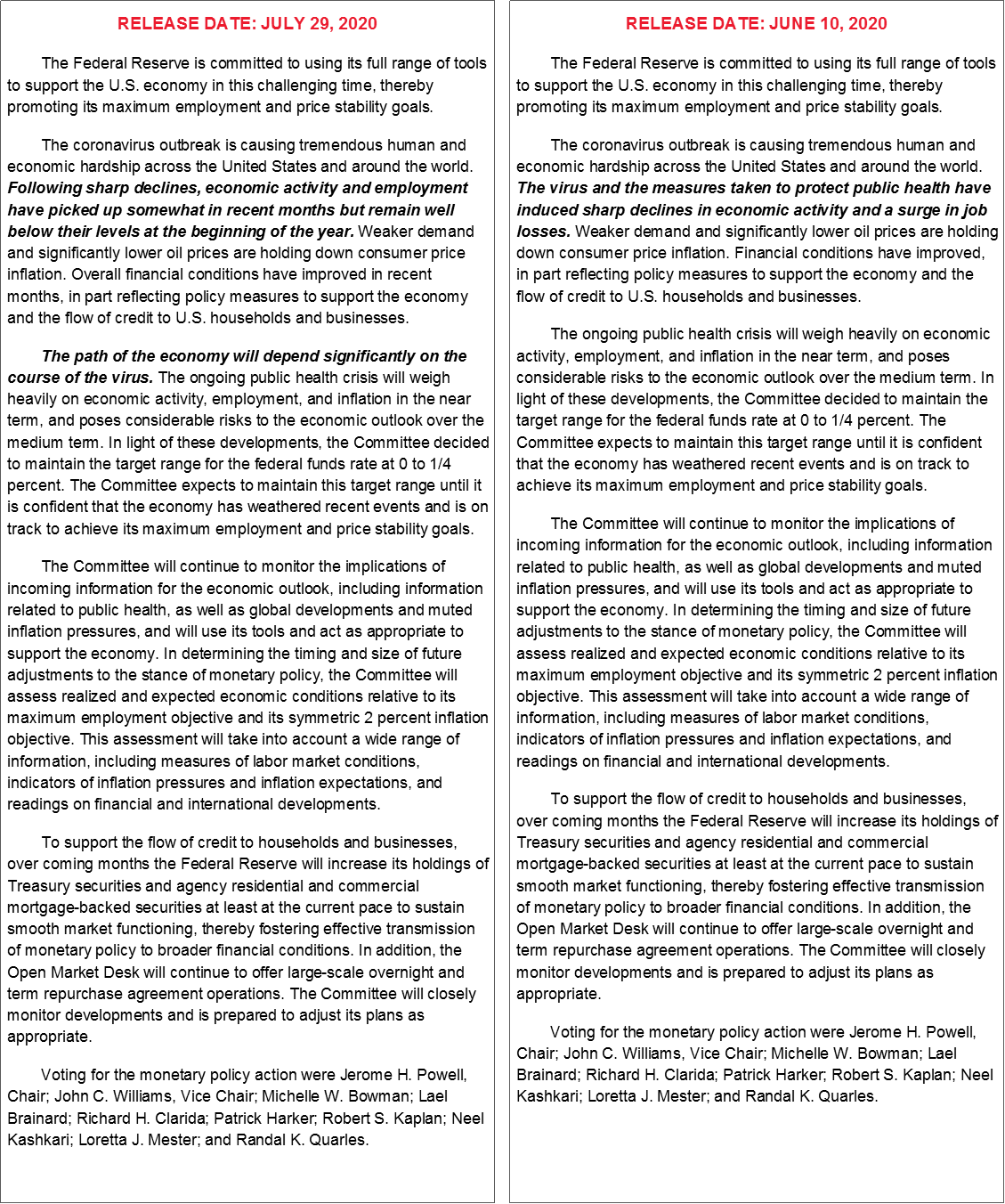

Simply put, hardly anything changed as the statement was like a misleading trailer for the hour long movie that followed a half hour later. Please see the accompanying statement comparison.

The description of current conditions noted some activity improvements;

Nevertheless, the emphasis upon forward risks was retained and the statement spelled out a lack of confidence in forecasting future outcomes by bluntly stating that “The path of the economy will depend significantly on the course of the virus.” Thus, the Fed essentially faded the rebound evidence.

They continue to reference how they will “act as appropriate”

They retained unchanged forward guidance and unchanged purchase guidance.

The decision was unanimous.

FORWARD GUIDANCE—THE STATEMENT VERSUS THE PRESSER

Forward rate guidance in the statement was left unchanged as expected. It still says the target rate range will be left where it is until the FOMC “is confident that the economy has weathered recent events and is on track to achieve its maximum employment and stability goals.”

During the press conference, Powell stated “Don't look to us to cut back on facilities or policy for a very, very long time.” He also repeated his line from the June press conference when he said “we're not even thinking about thinking about raising rates." That’s consistent with the prolonged policy rate hold in the dot plot that foresees no rate hikes throughout the 2020–22 horizon. Markets have already been hit over the head with the message that rates are going nowhere for a very long period of time and it’s unclear that anything they say when they release their strategic review would tell us much more.

Nevertheless, Powell noted that while different forms of forward guidance were discussed again, the FOMC has reached no decisions on the form of potentially altered guidance. He simply repeated that whether calendar-based or condition-based guidance is chosen is “very fact specific”.

STRATEGIC REVIEW—A DAMP SQUIB

Powell’s opening statement immediately headed off questioning about how its strategic review is progressing. He noted that the FOMC resumed discussion at this meeting and discussed enhancements to longer run goals and approaches but that he would have no details to share today. Powell stated that they will wrap up deliberations in the near future. Watch the minutes to this meeting three week’s hence for further clues.

That fended off questioning about potential changes like altered forward guidance, yield curve control, altered asset purchase programs etc.

Powell stated he could not tell us about the exact timing in terms of when they would communicate their decisions. As previously noted, however, I would look to the virtual Jackson Hole style conference at the end of August with its focus upon the decade ahead for clues.

A MESSAGE TO CONGRESS

While Powell generally continued the practice of deferring the fiscal policy dialogue to Congress, he nevertheless had a thinly veiled message for them. First, he emphasized that “we are seeing the results of the earlier strong fiscal response through spending. In a broad sense it has been well spent and kept people in their homes.” He went on to note that there will be a need for more monetary policy and fiscal policy support and that “Even if the recovery continues there will still be lots of people left behind and they are going to need support to pay their bills and spend and keep their accommodations.”

Further, Powell noted that “I would not disagree with the importance of fiscal policy because it can address things we cannot, like grants that can save jobs and businesses as opposed to lending money they may not want or be able to repay.”

The message is to Washington’s hold-outs is to acknowledge that much of the improvement to date has been driven by fiscal policy that he described as rapid and large, and hence the implied reasoning is that ending it prematurely puts those gains at renewed risk.

CONCLUSION

The question now becomes how markets will take it if both the Fed and fiscal puts lie dormant over the months ahead. Fiscal talks appear to be in a mess and the Fed is dragging its feet on its strategic review and next steps. A lagged policy response to potential downside risk would likely have to rely upon the Fed’s limited additional policy tools with pretty much everything priced. At hand is perhaps the last chance for Congress to pass a meaningful stimulus bill that is larger than presently judged to be required because there may not be another chance to counter risks until the new Congress sits in January and likely some time thereafter. In my view, this insurance motive should drive a greater fiscal response.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.