- Canadian jobs rise more than expected…

- ...avoiding a feared dip...

- ...even as they post the weakest gain of the recovery

- A positive print adds cover for the BoC to stand pat next week

Canada jobs m/m change (000s) / UR (%), SA, November:

Actual: 62.1 / 8.5

Scotia: 20 / 8.9

Consensus: 20 / 9.0

Prior: 83.6 / 8.9

Not too shabby. That about sums up my take on Canada’s gain of 62k jobs in November and the underlying details. It beat all estimates within consensus including my guesstimate of +20k which was at least on the right side of the ledger One-third of forecasters had anticipated a decline. See the accompanying table for highlights.

Indeed, a job loss was the market fear factor on this one and so when avoidance of a drop was combined with a weaker US payrolls report the result was a shift in market positioning that drove the Canadian dollar to appreciate by about three quarters of a cent to the USD. Canada’s sovereign debt curve bear steepened, but by a little less than in the US following the duel jobs reports.

Canada is now “just” 573,000 jobs away from the pre-pandemic peak in February and has regained 2.4 million of the initial 3 million jobs that were lost from February to April (chart 1). A half million lives still impacted by job loss is terrible and would be viewed as such in any normal recession not to mention one that is imposing a tragic toll in so many other ways. Still, balance requires that we have to acknowledge the almost 2½ million who are able to return to some form of work even if not the same in many instances.

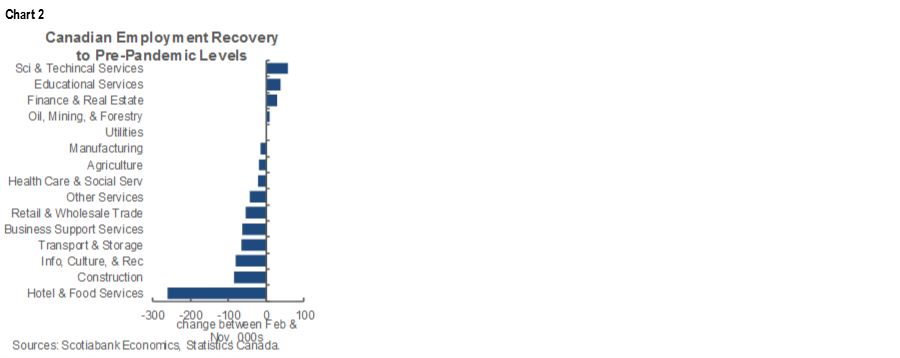

Chart 2 shows the uneven progress in recapturing jobs by sector since the pandemic erupted.

I’ll take it, at least for now and especially since Canada has already extended the job market supports to cover the uncertainty that lies ahead whereas the US is still debating whether to do so and by how much. As previously guided, it’s the next report I was more worried about than this one. A major reason for this is due to tightening COVID-19 restrictions. Ontario basically shut down Toronto and neighbouring Peel region and tightened restrictions elsewhere immediately following the reference week for the Labour Force Survey. Further restrictions are coming in today’s announcement from Queen’s Park at 1:30pmET. Both rounds of restrictions are sure to bite into the next jobs tally for December about one month from now.

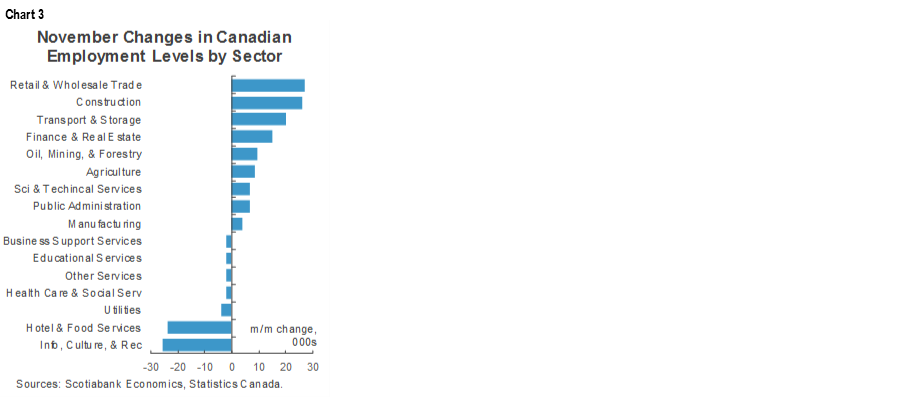

We can get a glimpse at the effects to come in the break down of the sector details to this report. Chart 3 shows the breakdown of the change in employment by sector during November. Breadth was ok as 9 sectors out of 16 were higher, five were little changed and two were down but rather significantly so. It is these last two categories that are likely to continue to be a drag on overall employment in subsequent reports as they are particularly vulnerable to COVID-19 restrictions (e.g. bars, restaurants, travel, accommodations etc).

By sector, goods industries added 44k jobs while services added 18k. Within goods the bulk of the gain was in construction jobs that were up 26k while resources added 10k, manufacturing was up 4k and utilities fell 4k.

Service sector jobs were up 18k. The only real upsides were in wholesale and retail trade (27k), transportation and warehousing (+20k) and finance/insurance/real estate that was up 15k. Downsides came through info/culture/rec that fell 26k and accommodation and food services that fell 24k. Other sectors were flat.

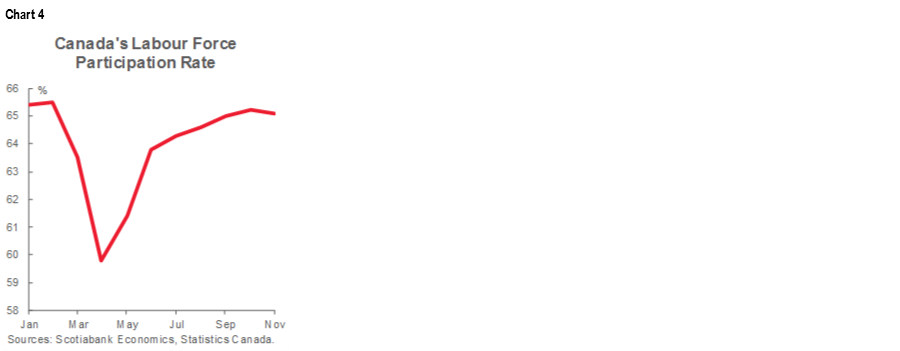

Those counting themselves in the workforce either as employed or actively seeking work have driven the participation rate back up to 65.1% after it bottomed at 59.8% back in April (chart 4). That is just tenths of a percentage point from the peak in February and encouraging evidence of a jobs rebound that has also pulled more people back into looking for work.

Hours worked are tracking a rise of 16% q/q at a seasonally adjusted and annualized rate so far in Q4 (chart 5). The sharp rebound in Q3 is continuing into Q4. Since GDP is an identity defined as hours worked times labour productivity, a solid gain in hours worked bodes well for GDP growth all else equal.

Public sector jobs were up 32k while private sector employment was up 23k. Self-employed jobs were up by just 7k.

By province, the gain was led by Ontario (+37k) and then British Columbia (+24k) followed by Quebec (+10k). Nova Scotia added 10k. Manitoba fell 18k, Alberta lost 11k and Saskatchewan was little changed (-3k) as were other provinces.

Full-time jobs were up 99k as part-time employment fell by 37k. There were 82k fewer unemployed Canadians last month.

The unemployment rate fell four-tenths of a percentage point to 8.5% as the labour force shrank by almost 20k while jobs climbed by 62k.

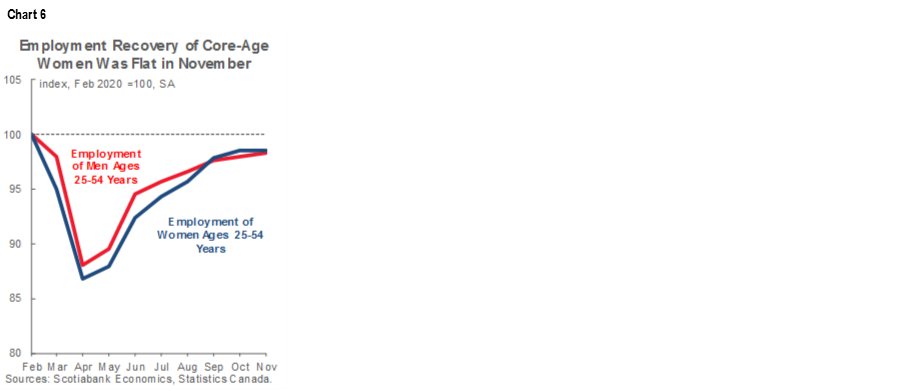

Women have endured a disproportionate hit to employment during the pandemic and so it is encouraging to see chart 6 that shows male and female employment levels recovering on par to one another ever since schools reopened. This continues to emphasize the importance of keeping schools open from the standpoint of the economy and gender effects. Still, disproportionate early hits to employment carry long lived effects on women.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.