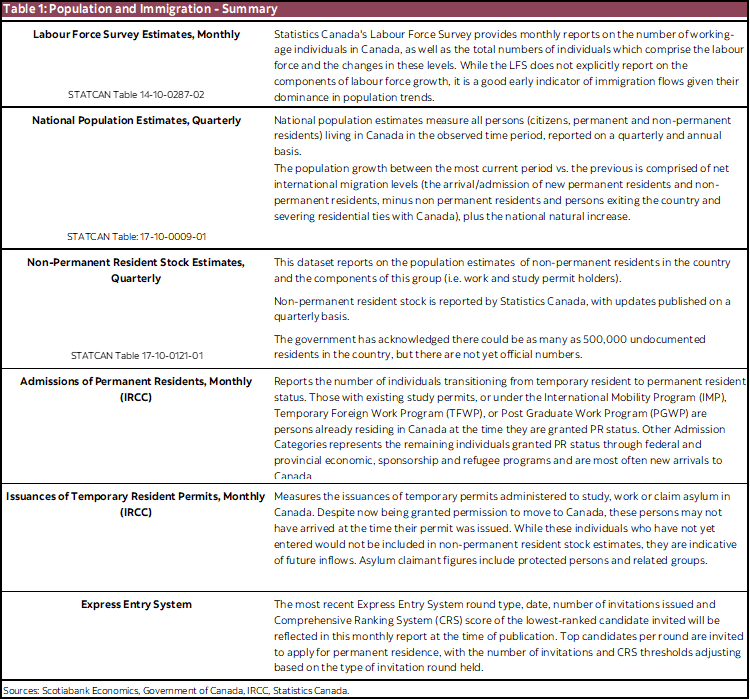

This report tracks admissions and issuances of individuals granted permission to permanently and temporarily reside in Canada, and whether these figures are aligning with federal government immigration targets.

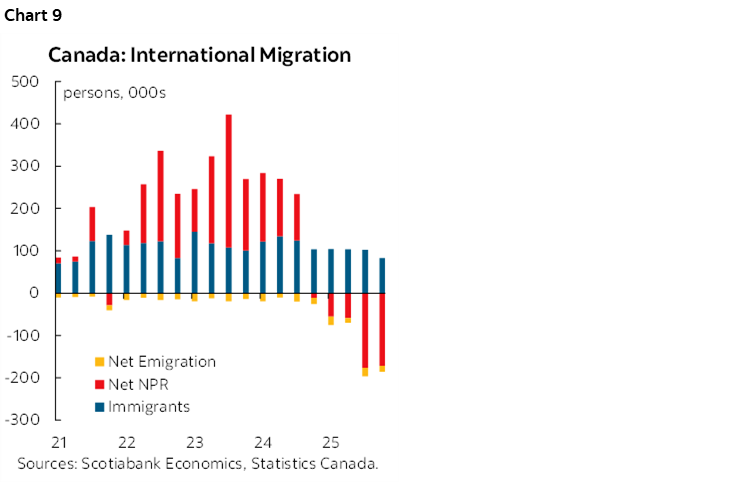

In line with federal plans, the latest Quarterly Population Estimates from Statistics Canada confirmed a first-ever population decline in 2025, as outflows accelerated towards year-end

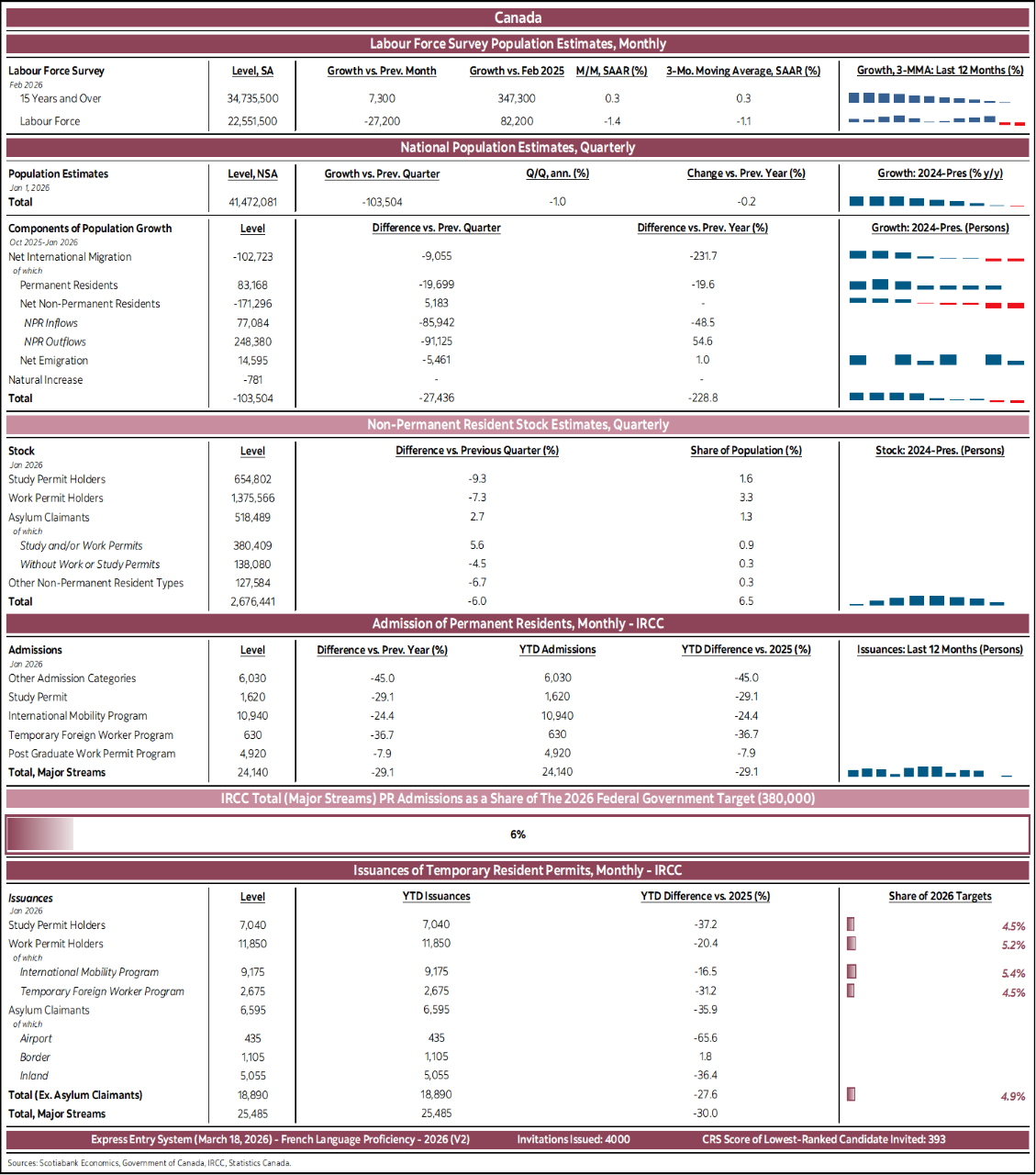

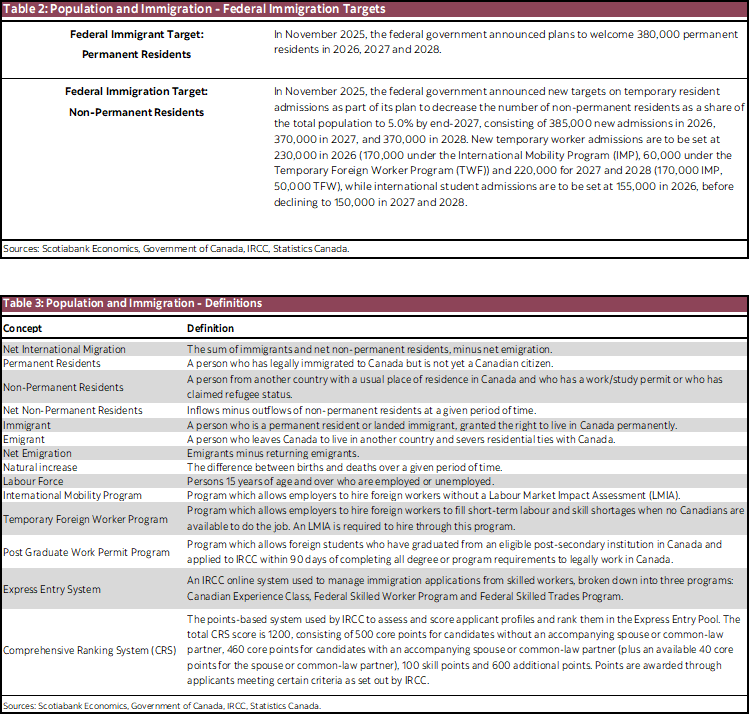

- Lagged quarterly official national estimates recorded a population contraction of over 103,000 (-0.99% q/q ann.) in the period ending January 1st, 2026, the second consecutive quarter to do so. As a result, the federal government can claim a successful first year in their plan to reign in immigration numbers, as the country witnessed its first annual population decline since modern records began, falling by approximately 102,000 when compared to January 1st a year prior, a contraction of 0.25%, driven largely by further declines in total non-permanent residents (NPRs).

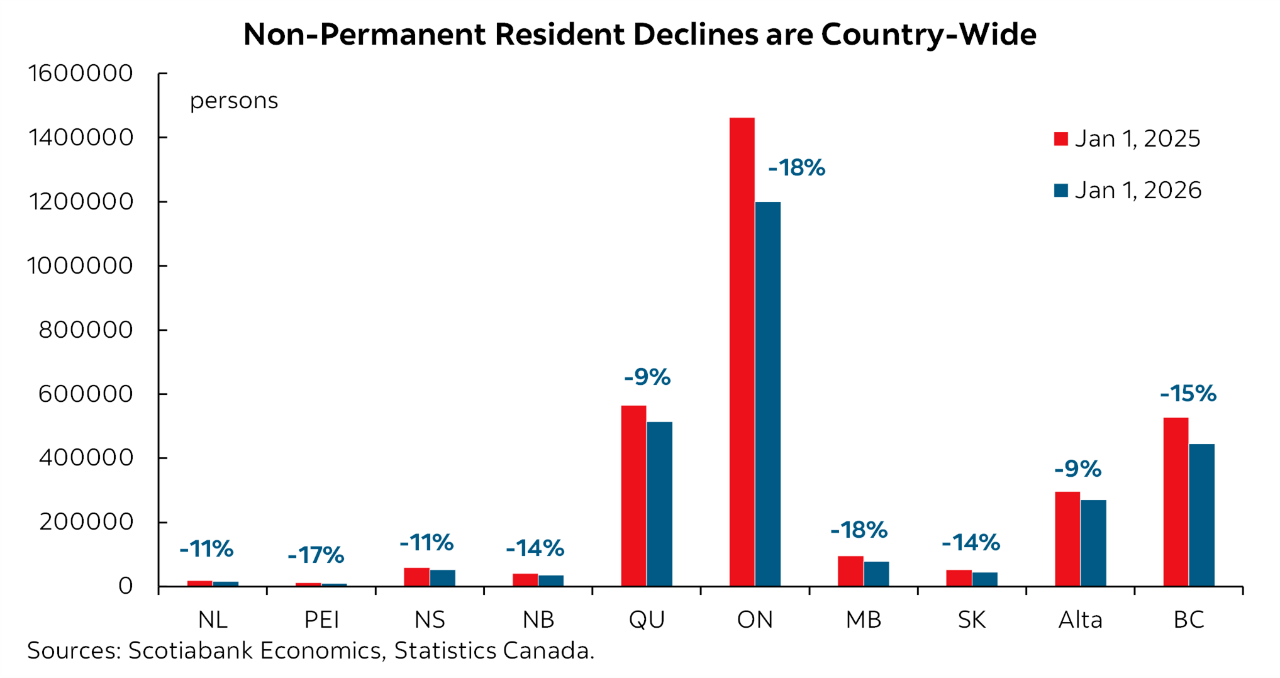

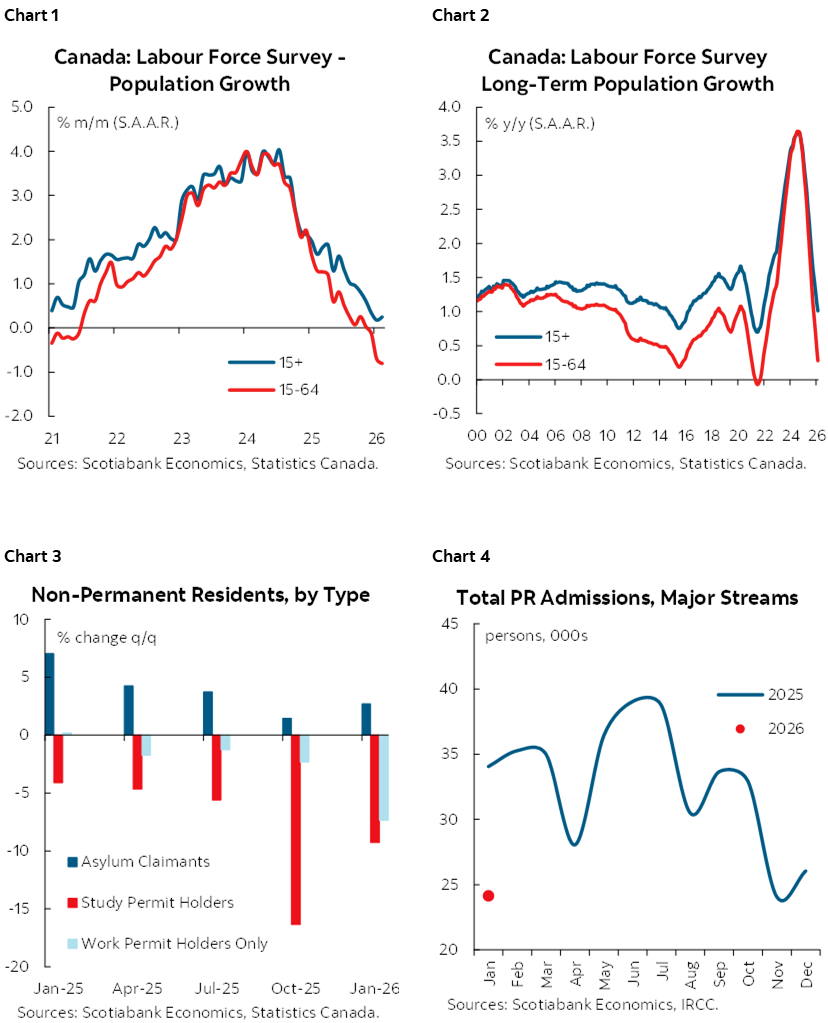

- NPR declines were more broad-based versus previous reports, with the number of work permit holders recording a consistent trend downwards (-108,885 q/q, -12.2% y/y) after plateauing and remaining elevated through the winter and spring of 2025 and likely explaining, in part, some of the softness in early 2026 labour market prints, with supply remaining an important ongoing consideration. While study permit holders, or those with both work and study permits continue to see quarter-over-quarter declines, the pace of net outflows has appeared to slow down, though additional recordings will need to be captured in the months ahead to confirm whether their numbers are beginning to shore up, or whether this was just a temporary blip in an otherwise consistent downturn.

- As a result of sustained exits (along with a portion of those transitioning to permanent residency (PR) status—who, despite not leaving the country, are counted as an NPR outflow by Statistics Canada), the number of NPRs as a share of the total population fell from 6.8% in the previous quarter to 6.5%. While reaching the original 5% goal by end-2026 still seems out of reach, doing so by the end of 2027 appears to be comfortably on track, should the rate of NPR exits continue.

- The recent quarterly declines in total population, along with the rate of which NPRs have been leaving the country, put the country on track for another year of negative growth, in line with the federal plan. However, specific pivots and deviations from policy in a bid to address labour shortages (as we have recently seen with the federal government’s decision to allow rural employers to increase their share of low-wage temporary foreign work permit holders from 10%–15% through to March 31st, 2027) and under-target international student arrivals may dampen the rate of net exits and prove to be the ultimate difference between a year of negative or flat growth.

Fresh permanent resident (PR) targets, with a renewed emphasis on economic immigration and applicants already residing in Canada

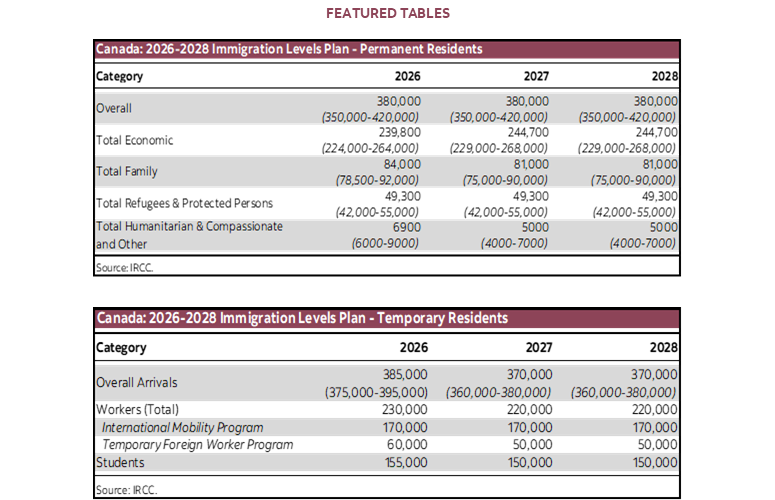

- 2026 PR targets (380,000), although reduced by 15,000 versus the previous year, aims to increase the share of those admitted under the Economic category to approximately 63% of all admissions. As with 2025, the majority of new PR admissions are expected to be from those already living in Canada and previously holding a temporary permit. Close to 60% of the approximately 393,500 admitted in 2025 fell under this category, with 2026 expected to follow suit, if not record even higher proportions this year.

- The first recording of the year points to a strong start, with approximately 66% of the 24,140 applicants who were admitted to PR status in January falling under the Economic immigration category, the majority of whom were admitted via the Canadian Experience and Skilled Worker streams.

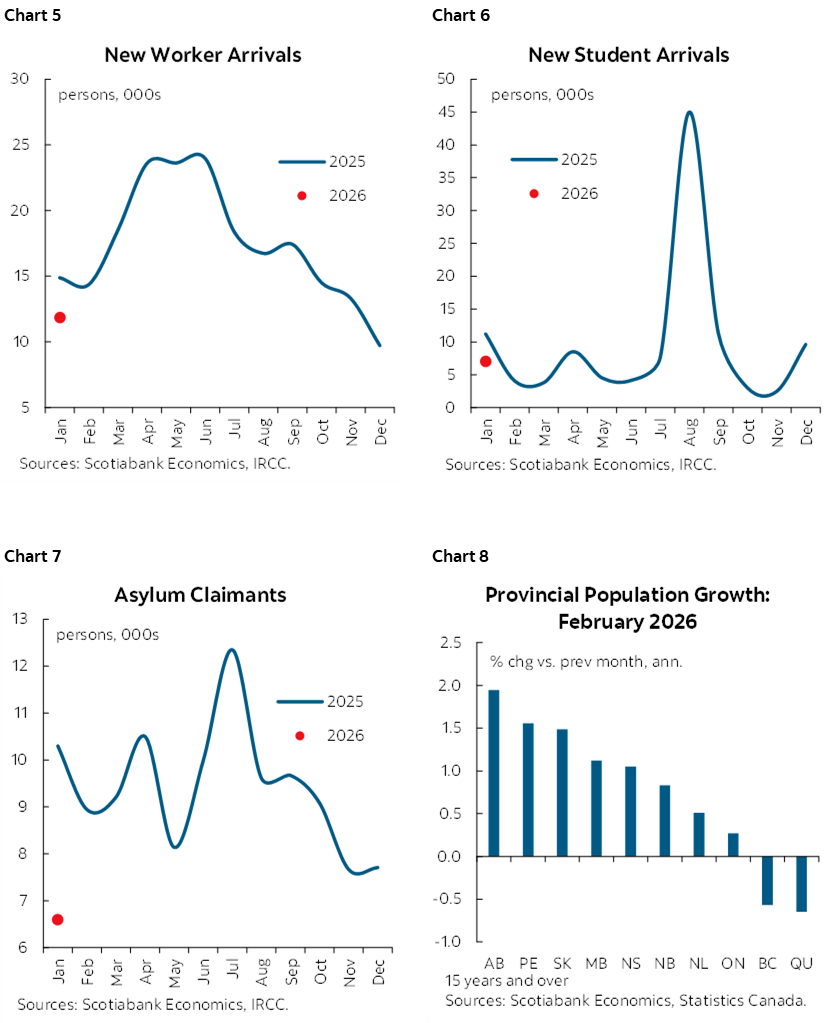

- Beyond raw admission numbers, provincial destinations and long-term residency for these new and existing PRs will be vital in managing the labour market fallout which inevitably comes with such a large and rapid exodus of TRs across the country. TR exits, particularly those who had arrived in Canada for work reasons, will not affect provinces proportionately. Larger provinces, such as Ontario, with its already-large population base, can sustain immigration outflows better, particularly when some of these exits can be offset via interprovincial migration. Smaller provinces, however, such as those in Atlantic Canada, are more exposed to the effects of work and study permit holders leaving the country, while also suffering from some of the lowest PR retention rates country-wide in recent years.

Temporary resident admissions are low. How many actually arrive may be a lot lower…

- New temporary permit arrivals, already having come in below target last year, have also started 2026 at a trickle, with Canada welcoming 7040 new students in January, a 37% drop in new arrivals compared to the same month a year prior. The same story applies to new worker arrivals, which recorded a 20% year-over-year decline versus January 2025, with both Temporary Foreign Worker (TFWP) and International Mobility Program (IMP) permit holders registering lower entries.

- Regular seasonal entry spikes may help bump total entries up closer to annual targets as the year progresses, but sustained low arrival flows could weigh on labour markets and pile existing financial pressure on many cash-starved colleges and universities which have partially relied on international student tuition fees as a trusted revenue source.

Featured Chart

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.