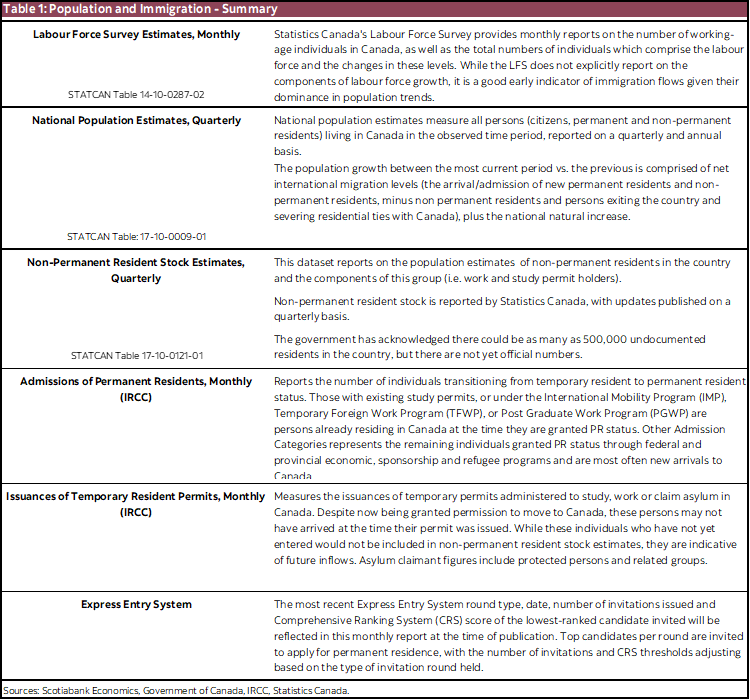

This report tracks admissions and issuances of individuals granted permission to permanently and temporarily reside in Canada, and whether these figures are aligning with federal government immigration targets.

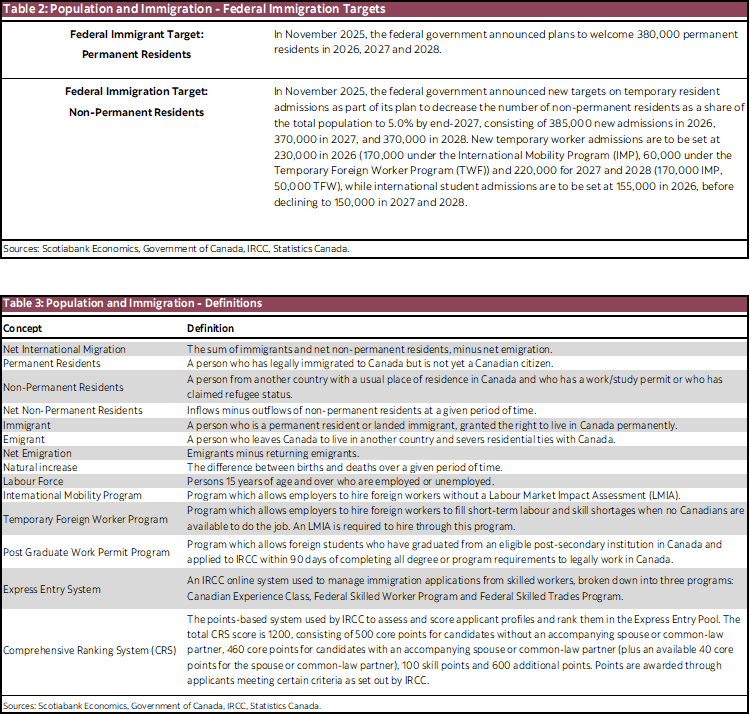

Canada’s population trends are firmly in the negative

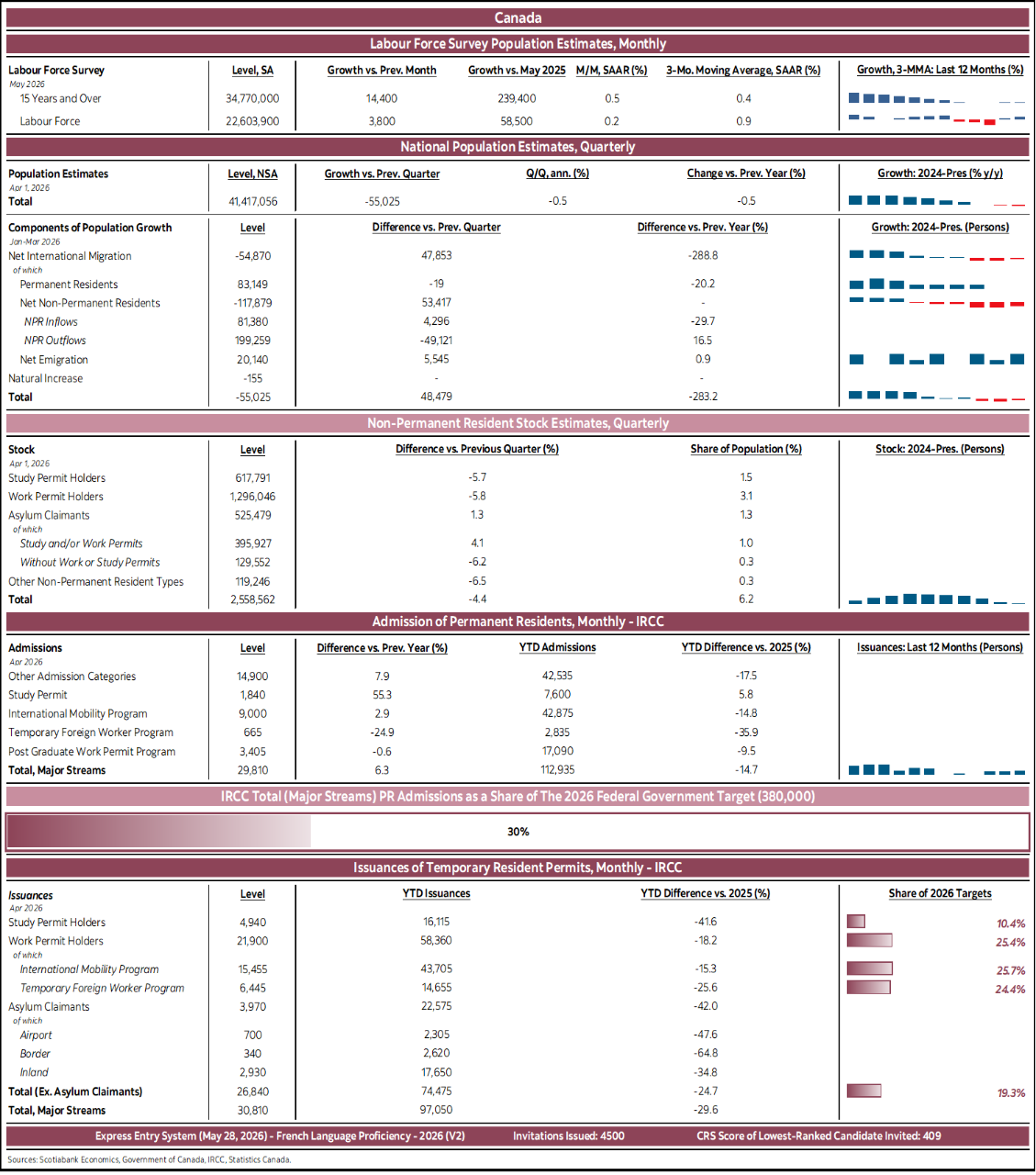

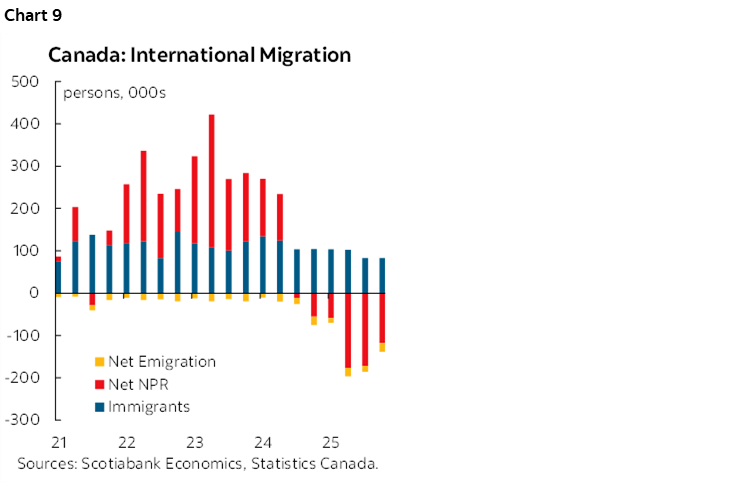

- Lagged quarterly official national estimates recorded a total population contraction of 55,025 (-0.1% q/q) for the quarter ending April 1st, 2026—a third consecutive decline in the total population—albeit the slowest of the three recordings so far, and a slight comedown after a quarterly contraction of approximately 0.25% in the previous quarter.

- Similar to the previous quarter, contributions to Canada’s overall population decline were evenly shared between temporary study and work permit holders, with the former’s population shrinking by 5.7% between January–April, and the latter’s following suit at –5.8%. Notable drops once again (and the main sources of Canada’s population decline), but markedly slower than January’s recordings, despite new intake numbers for both international students and workers currently coming under the Federal government’s 2026 target (further details below).

- As a result, the population of non-permanent residents (NPRs) as a share of the total population now stands at 6.2%, with international students comprising just 1.5% of the population, while temporary work permit holders make up 3.1%. While the decline in the number of temporary work permit holders has been gradual since the introduction of annual temporary permit holder arrival caps, the pace at which the international student population has declined has been rapid, to say the least. After peaking at over a million in mid-2024 (study + study and work permit holders), today’s total stock stands at just under 620,000, a result of effective immigration restrictions and much lower than anticipated international student arrivals.

Permanent residents—a bit behind on quantity, on pace with quality

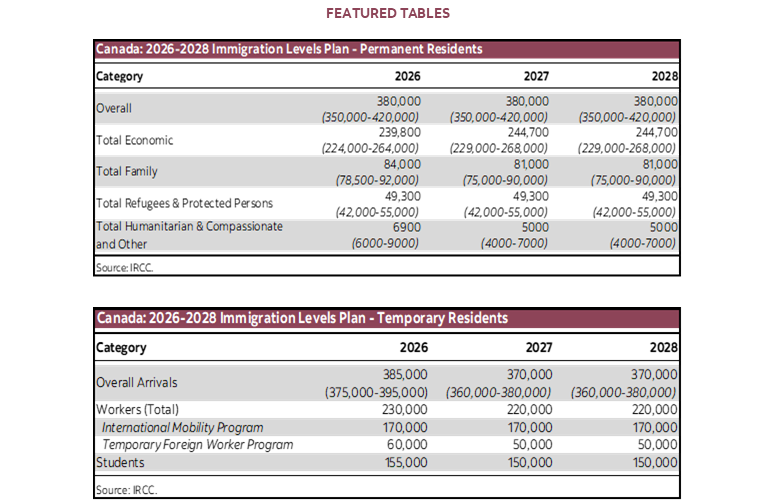

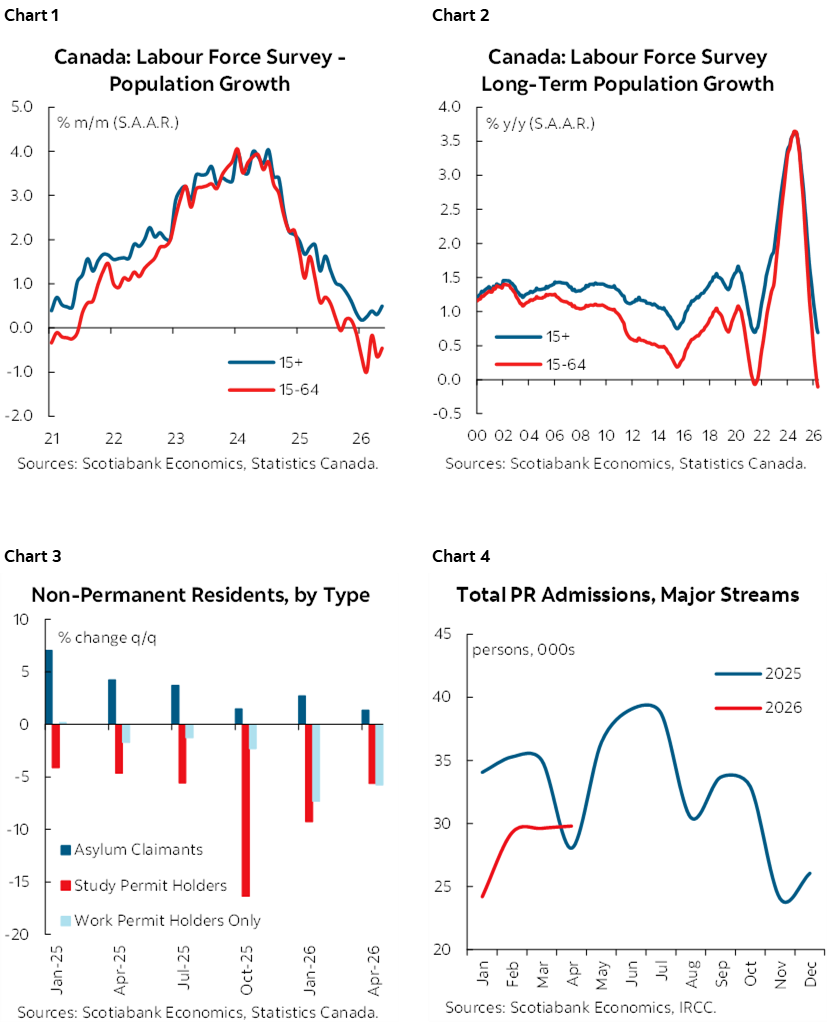

- Between January and April, Canada has welcomed just under 113,000 new permanent residents, accounting for approximately 30% of the 2026 PR target, slightly under the pace needed to reach 380,000 new additions by the end of the year, though still within range to more than make up for the lag as the year progresses.

- Of the roughly 113,000 new admissions, approximately 58% of those are former temporary residents who have made the transition to permanent residency, a noticeable increase in the share compared to previous years, which has so-far remained consistent since the implementation of the new Immigration Levels Plan. In addition, close to 60% of total PR admissions have fallen under the Economic category.

- While Ontario (as expected) holds the largest share of total Economic category PR admissions (slightly over one third of this category admitted this year), remaining provinces have not seen substantial rises or declines of Economic PRs compared to last year’s intake (Jan–Apr. comparison). Additionally, 7000 of the planned 20,000 applicants under the In-Canada Workers Initiative (an accelerated PR program for temporary residents living in smaller Canadian communities and working in in-demand sectors) have so far been granted PR status this year, constituting 35% of the 2026 target. An additional 13,000 are expected to be granted PR status under this plan in 2027.

Temporary residents—have Canada’s tight immigration controls dampened international appeal?

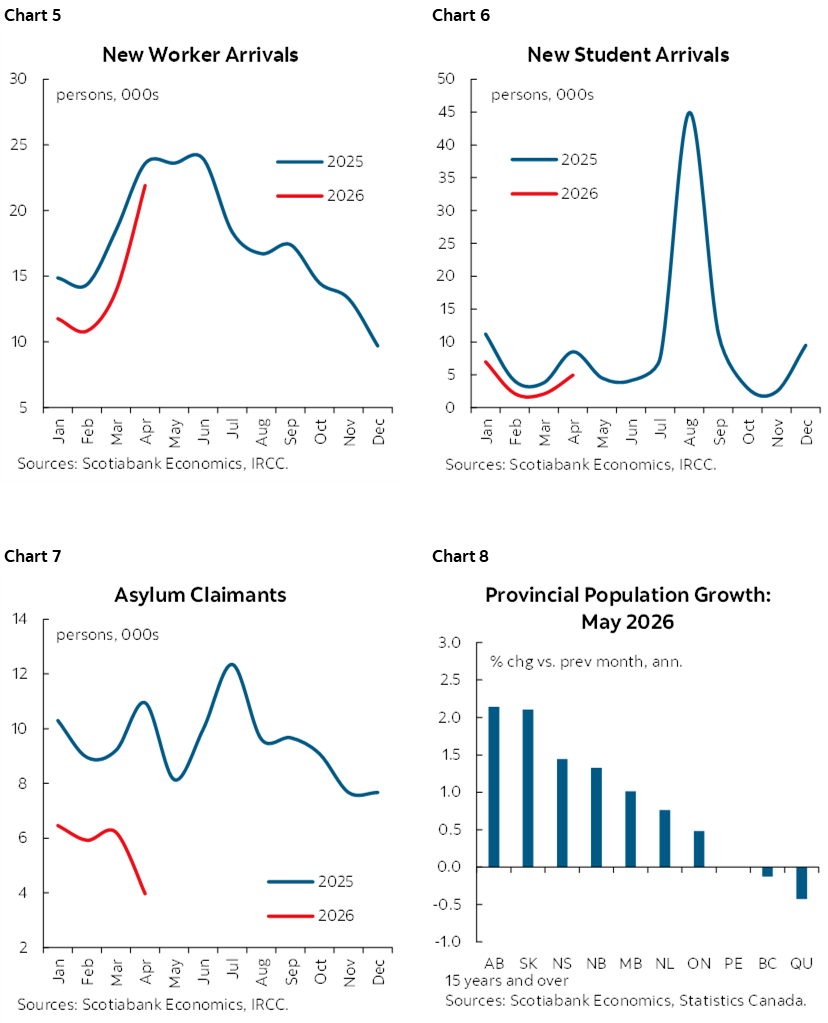

- New temporary work permit arrivals in both the Temporary Foreign Work and International Mobility Program categories have seen recent upticks in March and April, partially offsetting what was initially a very subdued start to the year. As a result, approximately 25% of the Federal government’s 230,000 cap on new temporary worker arrivals has been reached through April.

- Meanwhile, new student arrivals still show virtually no sign of picking up pace and generating a trend which would bring intake numbers even remotely close to the 155,000 cap set for the year. Standing at 16,115 year-to-date, new student arrivals are roughly 42% lower compared to the same period a year prior, and 84% lower vs. January–April 2024.

- Overall, while the pace of temporary resident exits may satisfy the Federal government when it comes to shrinking the total population to numbers in-line with their stated objectives (while also aiding in reaching their 5% temporary resident-to-total population share by 2027), the lack of new temporary workers and students could lead to a population overcorrection in the near future. Should expected arrival flows fail to materialize as the year progresses (particularly during the summer months, where new student arrivals historically peak), regional gaps in the labour force could appear and grow, while colleges and universities, still reeling significantly from lost international student tuition, could see further crunches, despite recent provincial pivots and initiatives.

- While addressing current backlogs will no doubt help with intake flows, the lack of new arrivals could point toward an immigration system which is perhaps going a step further than initially planned, and diminishing Canada’s appeal when prospective immigrants are deciding where to work or study. Not only are pathways to temporary immigration much more restrictive (along with higher financial and non-financial entry requirements), but reduced pathways to permanent residency (and ultimately citizenship), combined with the increased likelihood of not having your study or work visa renewed at the end of your term, can significantly diminish one’s incentive for moving to Canada in the first place. For a country where virtually the entirety of population growth comes from immigration, these can no doubt lead to significant structural economic issues in the long-run.

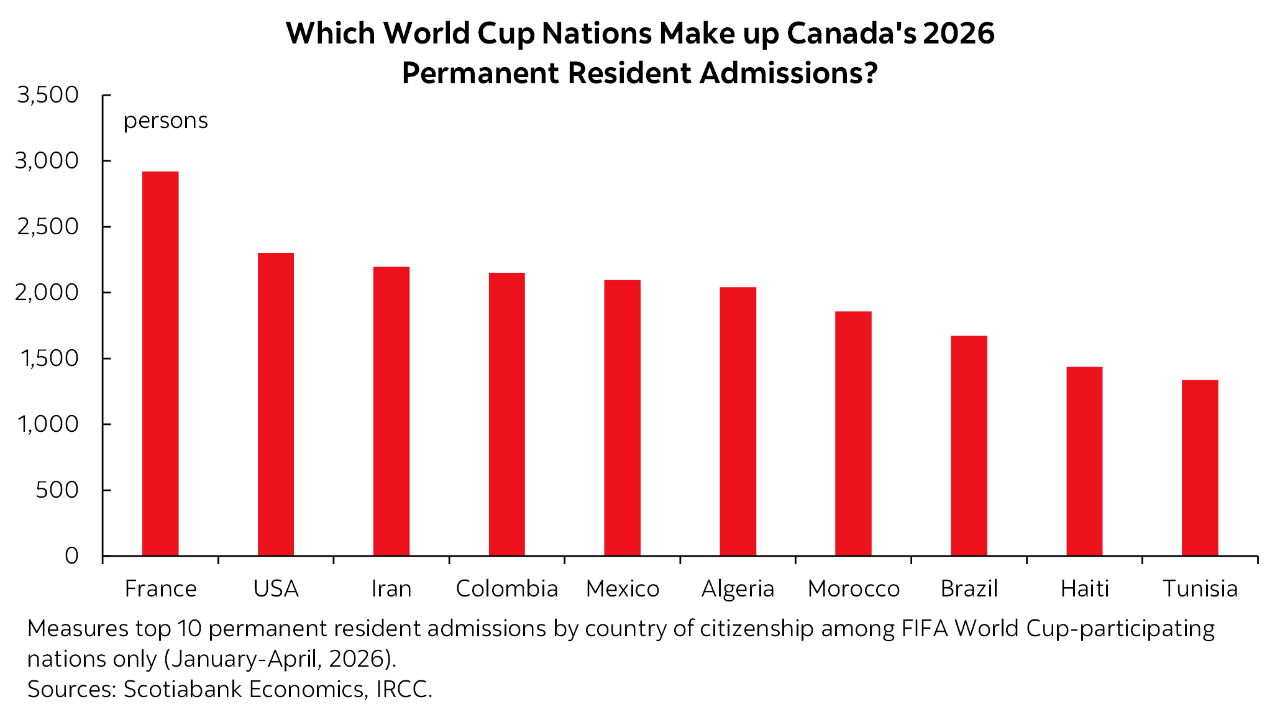

Featured Chart

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.