ON DECK FOR TUESDAY, OCTOBER 26

KEY POINTS:

- Risk-on sentiment with earnings drivers

- PBOC injects liquidity again

- US tech earnings in focus

- Is US consumer confidence a reliable warning sign?

- US new home sales, Richmond Fed also on tap

- Global COVID-19 case trends: Areas to watch

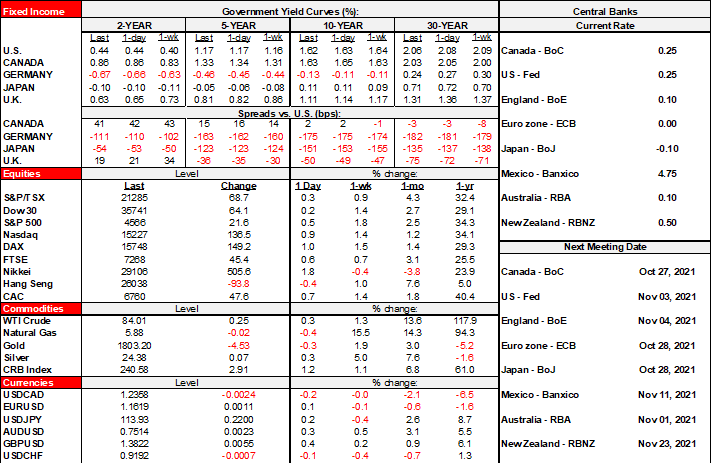

Global market sentiment is in risk-on mode this morning. Earnings are the main driver. N.A. equity futures and European cash markets are up by between ¼% and about 1%. Sovereign bond yields are under mild downward pressure toward the longer ends of US and European curves. The dollar is little changed overall, and oil is slipping by about ½%.

The PBOC once again injected more liquidity at the highest pace since January via 200 billion of gross 7-day reverse repo action that netted to 190 billion yuan after maturities (chart 1). Government bond issuance, tax payments, general month-end needs and nearer term stimulus are the drivers. The overnight repo rate has fallen by 67bps over the past week and back toward the low end of the range since January. Gross flows are likely to pick up with larger maturities through the rest of this week into early next.

38 S&P500 firms release earnings today. Pre-market names include UPS, 3M and GE, but most of the attention will be upon tech names in the after market such as Twitter, Microsoft and Alphabet.

A trio of 10amET US releases will mainly focus upon US consumer confidence for October. Another decline could play to a recent NBER research piece that argues that the decline in confidence points to the risk of a future downturn in the US. I wrote about this in the week ahead, as well as the big caveats around that view.

US new home sales during September are expected to rise given a gain in model home foot traffic and September’s pick-up in mortgage purchase applications that have slipped again this month (10amET). The Richmond Fed’s manufacturing index for October will further inform ISM-manufacturing expectations (10amET).

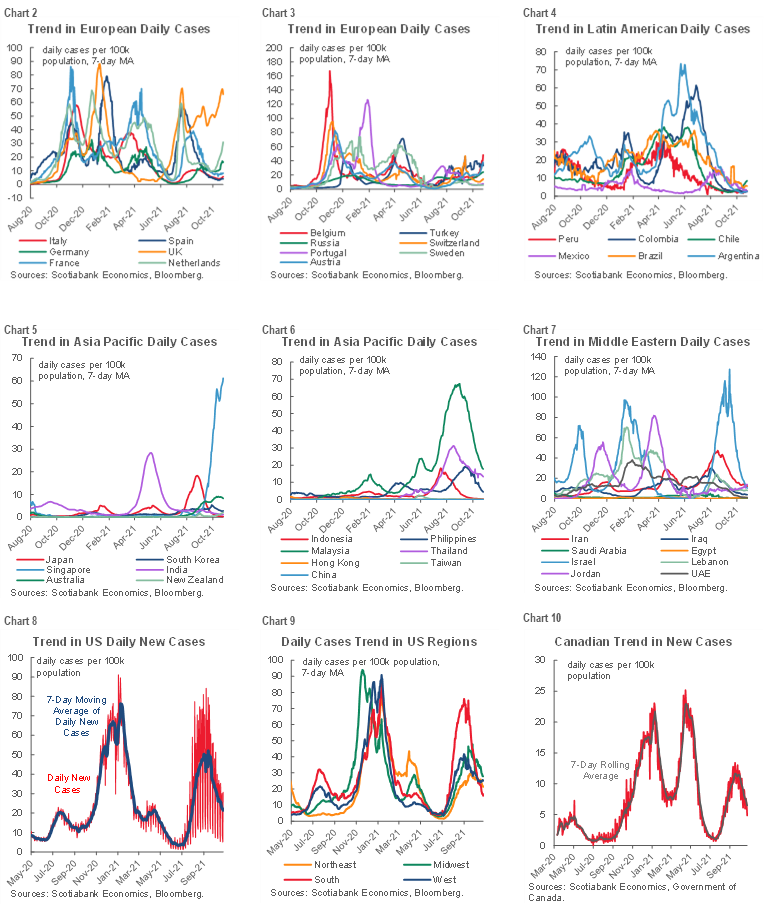

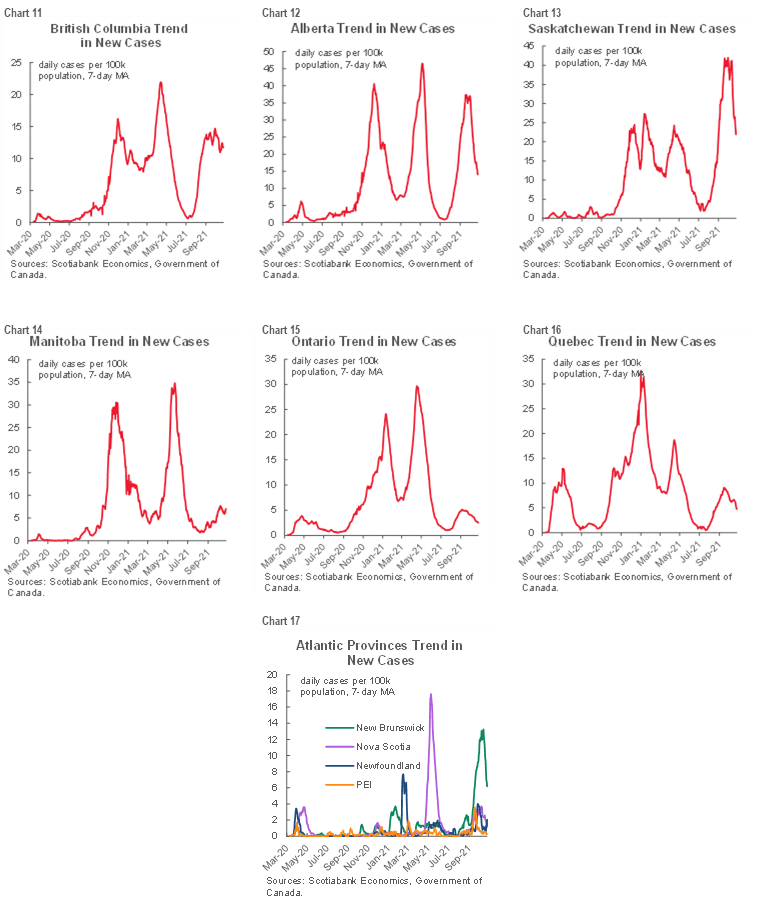

Charts 2–17 offer updated sweeps through global COVID-19 new case trends.

- Canada: Cases continue to decline and are running around one-quarter of the US per capita pace. They have generally remained low throughout this wave in the most populous provinces of Ontario and Quebec, but the nationwide decline in cases is being fed by improvements in Alberta and Saskatchewan.

- United States: Cases are still falling and doing so across all Census regions with much less variation across those regions than when the South drove the late summer surge.

- Latin America: All of the main economies are seeing low cases. A mild upturn in Chile bears monitoring.

- Europe: The UK is relatively out of control compared to most other regions of the world. The Netherlands is trending upward again and Germany’s up-tick needs to be closely followed.

- Asia-Pacific: Singapore remains in the worst position of any of the economies shown across the region.

- Middle East: Israel’s sky-high cases have come back down to earth and most of the countries are in a calmer state.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.