ON DECK FOR MONDAY, APRIL 26

KEY POINTS:

- Slight, uneven risk-on bias on a light start to the week

- US core durable goods orders resume upward march

- German IFO confidence slips a touch

- BoC’s Macklem elaborates on inflation overshoot forecast

- Global COVID-19 new case charts

INTERNATIONAL

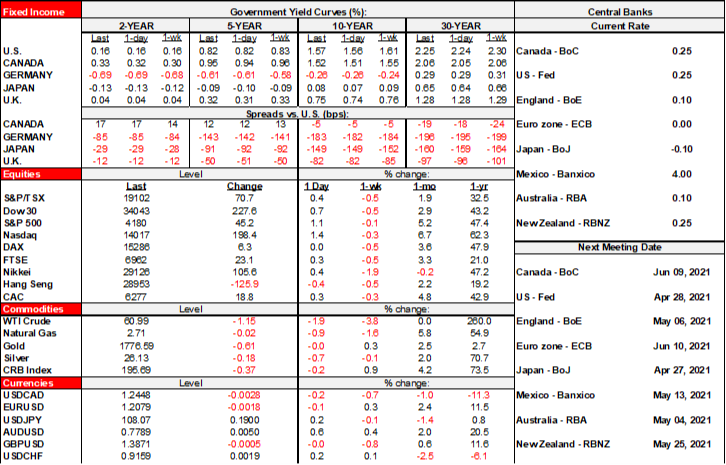

Stocks are little changed overall with Europe a little firmer and N.S. flat to lower. Sovereign bonds have a very slight cheapening bias in N.A. and Europe. The USD is little changed overall, but some higher beta crosses are a bit firmer including CAD despite oil being off 2% this morning.

It’s a relatively quiet start to the trading week and in terms of calendar-based risk. A couple of low-risk releases and a survey that brings forward Fed taper expectations are where the attention is focused.

German IFO business confidence slipped a touch but not in any significant way on either the headline measure or the components that track current and expected conditions.

UNITED STATES

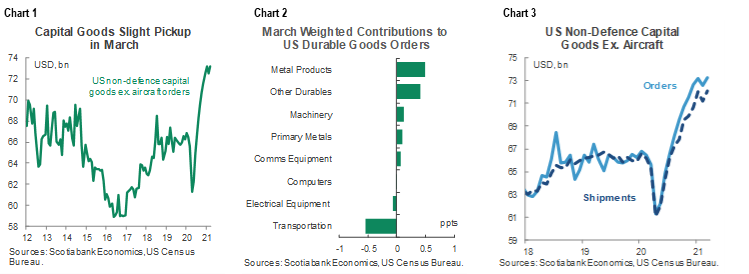

US durable goods orders (here) advanced by only 0.5% m/m (consensus 2.3%) with only a fraction of that miss explained by a small upward revision (-0.9% m/m in February, from -1.2%). Still, the details were more robust than the headline (see charts 1–3). Orders ex-transportation were up 1.6% m/m and on-consensus plus there was a slightly more positive upward revision to that measure (-0.3% m/m from -0.9%). Core orders ex-defence/air were up 0.9%.

Bloomberg’s Fed survey shows 75% of respondents expecting a first taper of bond purchases by 2022Q1 with a slim majority expecting it to occur over 2021H2 and the largest share of 45% expecting a taper to be delivered in 2021Q4. We’ve generally expected 2022Q1. It’s important to note that the survey is light on participation by US primary dealers and very light on participation by US money centre banks. To taper as soon as Q4 while delivering on the Fed’s promise to communicate well in advance would seem to face the high hurdle of starting the signals very soon, yet it seems unlikely to expect Powell to signal material progress on jobs for a while yet.

CANADA

There are no releases on tap today in Canada.

BoC Governor Macklem’s interview in the G&M this weekend (here) elaborated upon the intent behind forecasting a sustained overshoot of the 2% target. He said “That was a very deliberate, calculated decision. We were faced [over the past year] with the situation where inflation was very low, we had a lot of excess supply. Our major concern was deflation, or inflation that was far too low. By providing that exceptional stimulus, that’s helpful in getting inflation back to the target faster. If that means we go a little over the [inflation] target for a period, that is definitely a risk worth taking.”

First off, it hasn’t been just the past year; the BoC has seen inflation undershoot its target by any measure—headline or core—throughout the past dozen years or so and so the BoC still isn’t being anywhere nearly as transparent on the topic as the Fed. Further, pair this set of remarks with his remarks at last Wednesday’s press conference where he said this forecast overshoot was a function of the nature of providing extraordinary guidance to remain on hold for an extended period (now widely viewed to mean until 2022H2) whereas in prior cycles they might have hiked earlier. In other words, in the past, they would have tightened earlier and headed off some inflation but typically too early and/or too much. A distinct third possibility is that the BoC is trying to explain away how slow it was since last Fall’s arrival of vaccines and massive US and Canadian fiscal stimulus to change its narrative and now it faces a protracted path toward shutting down its balance sheet and hiking.

In my view, we’re getting conflicting signals on why the BoC is allowing an overshoot in its forecasts. In any event, pairing the two remarks to one another remains consistent with expecting lift-off over 2022H2 and still ending 2023 at or below the lowest end of the BoC’s neutral rate range which is 1.75–2.75%. Even by the end of 2023 with possibly six hikes in the bag, the BoC would still have a bloated balance sheet and a policy rate at or below any of its definitions of neutral. That’s how you get inflation overshooting.

COVID-19 TRENDS

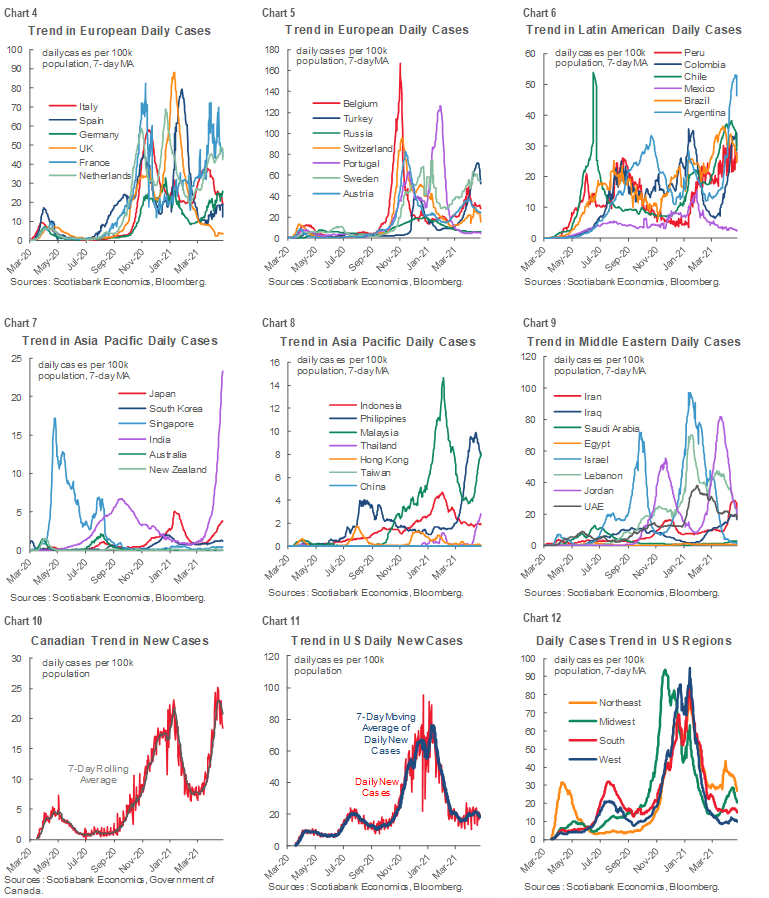

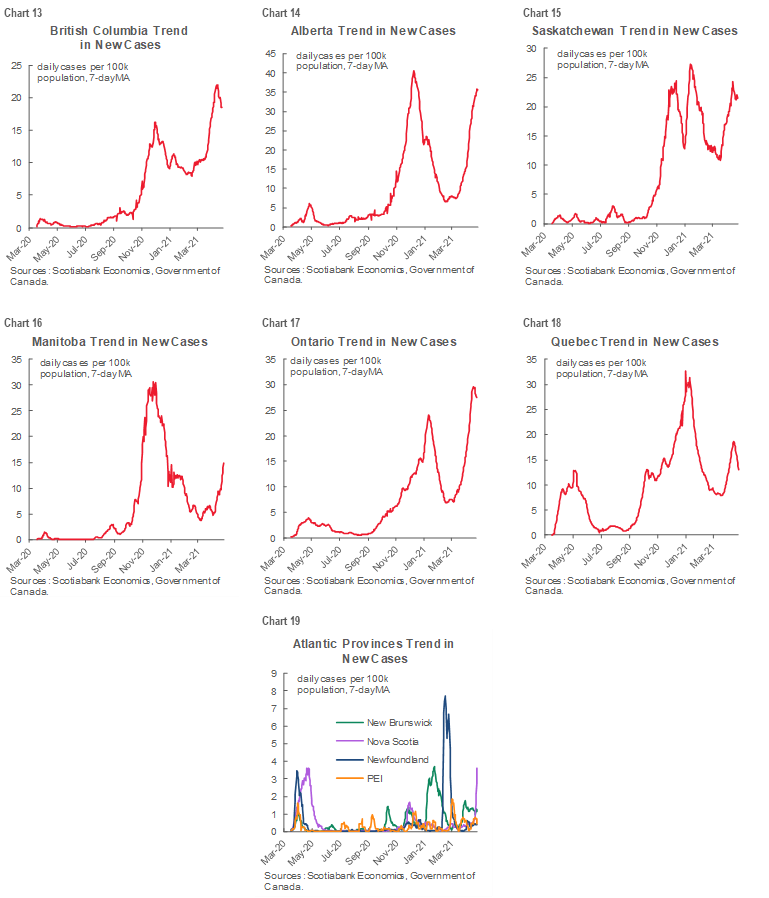

Also please see charts 4–19 that track the seven-day moving average of daily cases per 100,000 population across the world. In general, countries with the quickest vaccine progress (US, UK, soon Canada) are lowest.

- India: India’s very rapid and very sudden rise in new cases per capita is portrayed by a curve that has gone vertical of late. By sheer virtue of its massive population, the per capita new case rates remain well below the rates that have been witnessed across many other countries throughout the pandemic. That could well change and change fast given an explosive mixture of high population density and the features of India’s economy and health care system that make it difficult to contain the virus.

- US: The daily new case trend in the US continues to hover at pre-second wave levels dating back to last September–October. All Census regions are performing similarly, although the highest rates are in the northeast and Midwest.

- Canada: It’s early to call a top and if it is a top then it remains off the highest trend in per capita cases witnessed to date. Maybe BC, Ontario and Quebec are starting to see new cases plateau in the charts showing the regional breakdowns, but it’s premature to be sure of this.

- Europe: France, the Netherlands, Sweden and Turkey are among the countries experiencing high new case rates. New cases in the UK have all but disappeared due to rapid vaccine progress and earlier restrictions. Italy’s new case rate is falling, while Germany and Spain are on an upswing.

- Latin America: Mexico’s new case rate is lower than the rest of the region. Argentina remains the stand-out in terms of very high new case rates. The rest of the major economies are in the middle.

- Asia-Pacific: Apart from India, Japan remains on an upswing along with Malaysia and Thailand. Cases in the Philippines remain high but may be showing signs of a plateau.

- Middle East: All major countries are experiencing declines or—in the case of Iran—may be plateauing.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.