ON DECK FOR WEDNESDAY, DECEMBER 22

KEY POINTS:

- Choppy markets face no new information

- US travel and mobility are holding up so far…

- …with flights still close to pre-pandemic levels

- Canadian mobility is also fairly resilient

- It might be early for US consumer confidence to be impacted by omicron

- Lagging US existing home sales expected to advance

- Final US Q3 GDP revision on tap

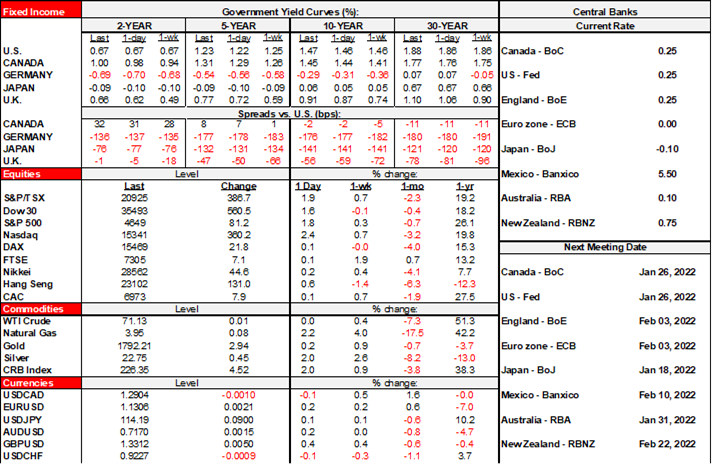

Fresh developments are practically non-existent in thinning holiday trading. There are no materially new COVID-19 developments. Overnight releases were non-existent other than the universally expected hold by the Bank of Thailand and with that we bid adieu to central banks for 2021 and thank them for high inflation... Geopolitical tensions are focused on the Russian devil beseeching the West to make a deal that hopefully they reject. Absent catalysts, US and Canadian equity futures are flat. European cash markets are flat to a touch higher. Sovereign bonds are a little cheaper, with 10 year yields up 1–4bps across the US, Canada and Europe. The gilts curve is up by about 4bps across maturities. Oil is unchanged. The dollar is very slightly softer and primarily versus sterling.

We’ve got some stale data coming our way from the US both today and tomorrow but the fresher readings on how consumers are behaving will follow the round-up of releases.

- It could be the most significant of the releases, but it might be too early for December’s consumer confidence (10amET) to show much reaction to the omicron variant given that only a portion of the sample up to last Friday would capture omicron’s escalating effects. Chart 1 shows the rough connection between new COVID-19 cases and the expectations component of the confidence gauge.

- Existing home sales for November (10amET) are expected to follow pending home sales with a significant gain.

- The third swing at Q3 GDP (8:30amET) incorporates fuller services spending estimates and is expected to be left largely unchanged.

So barring a big shift in consumer confidence, we’re likely staring at another session during which off-calendar risk including random tape bombs will dominate market movements in relatively thin trading that is about to get even thinner.

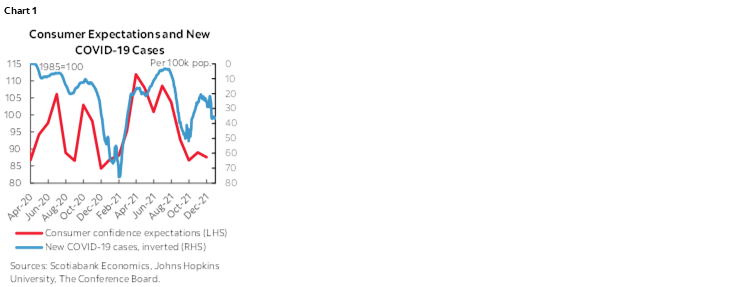

As an aside, it’s how behaviour responds that informs expectations for how economies will prove to be resilient to the new omicron variant. Behaviour is better judged by observing actions rather than surveyed words. As market observers, we can each have our views on how we think people should behave, but what matters is how they are behaving.

To that effect, chart 2 shows that despite headlines about cancelled plans and events, Americans are not changing flight plans in any significant numbers at least as indicated by Transportation Security Administration figures on checkpoint travel numbers. You or I might think they’re nuts to be floating in a tin can thousands of feet above earth surrounded by who knows what, but they’re doing it; in fact, the numbers continue to be close to the pre-pandemic conditions of 2019.

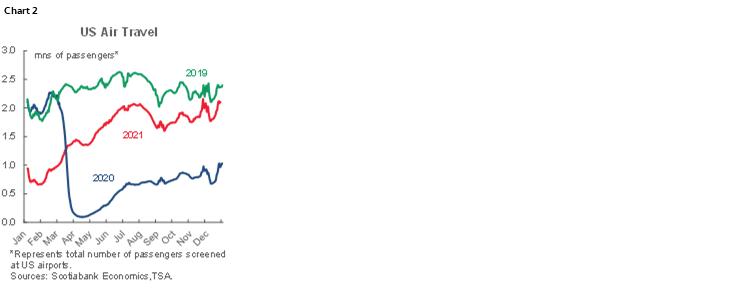

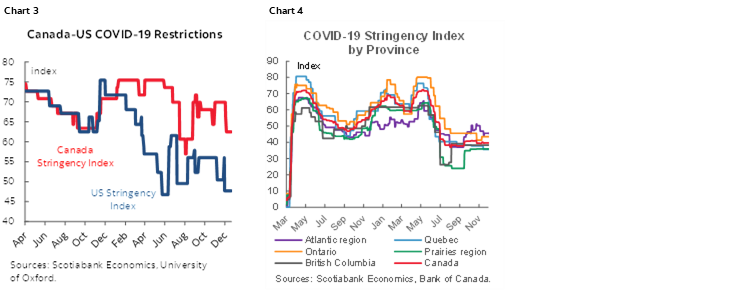

Further, with figures up to the other day, US and Canadian stringency indices remain low (few restrictions) as shown in chart 3. Chart 4 breaks this down in Canada by region.

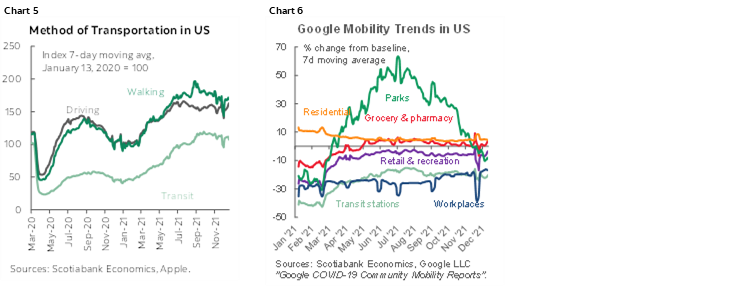

Also check out Apple’s resilient measures of mobility by mode of transportation which is data that is readily accessed because so many folks are a.o.k. with the company tracking all of your movement day and night, 365 days a year (chart 5). Google has similar data for the same reason; other than parks that are less frequently visited in winter months for obvious reasons, travel to other destinations is also holding up well (chart 6).

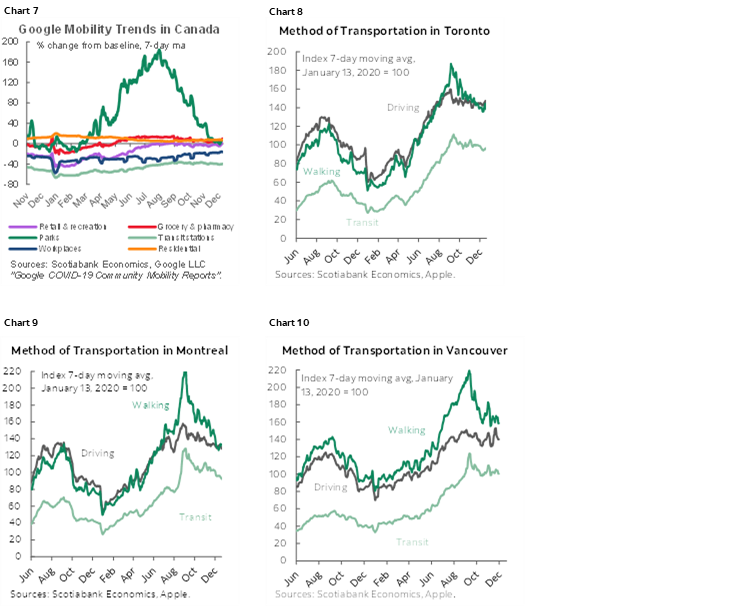

Canadian equivalents are shown in charts 7–10; there isn’t much evidence of softness other than normal seasonality via summertime influences on on driving and walking and park visitations.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.