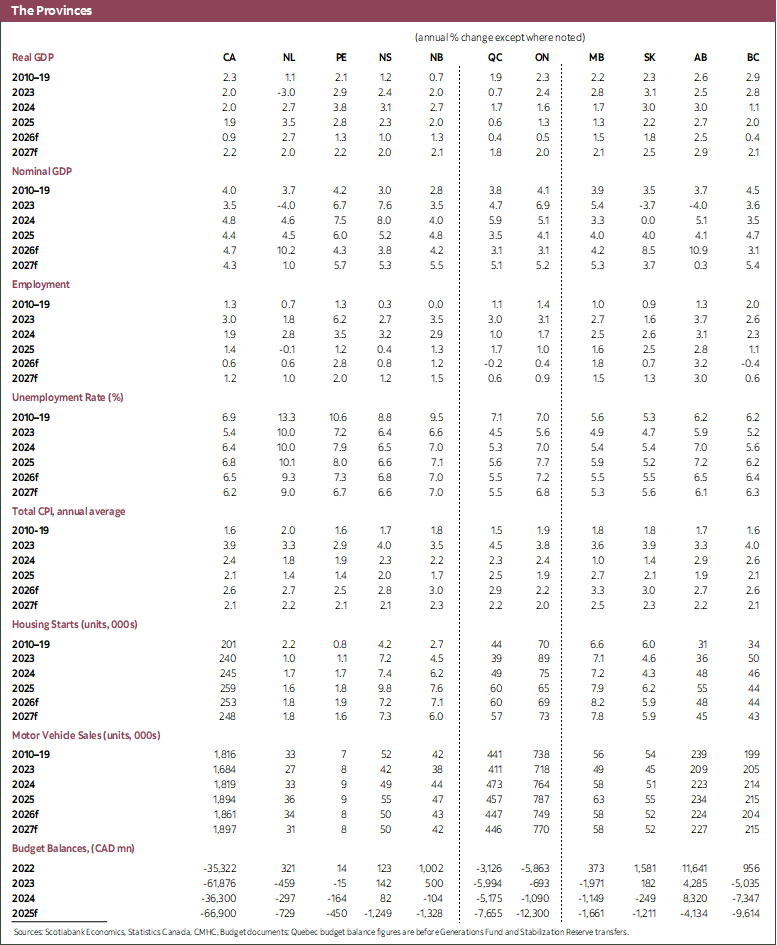

HIGHLIGHTS

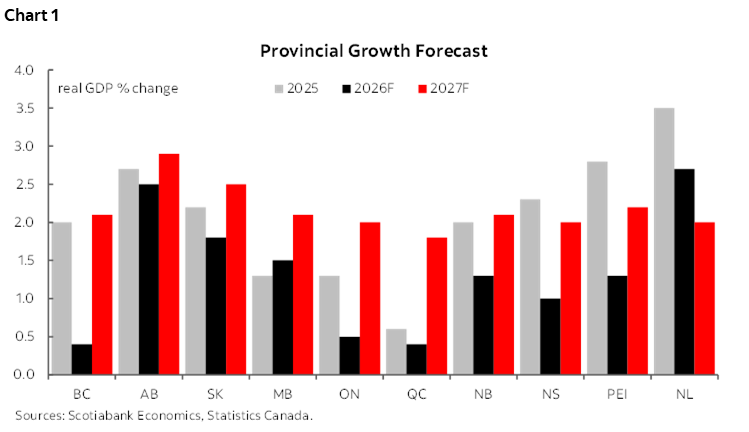

Economic growth in most Canadian provinces has slowed relative to recent years but is picking up (chart 1). The Canadian economy slowed over the course of 2025 due to tariffs, uncertainty, and sharply lower immigration inflows—though the strength of these headwinds have differed across the country. Quebec, Ontario, and British Columbia (B.C.) have seen the biggest impacts, with lower burdens in other provinces. Earlier this year, conflict in the Middle East added an oil price shock to the mix—benefiting oil-producing provinces, but increasing costs for consumers across the country. As we enter the second half of 2026, oil prices have dropped (though not to pre-conflict levels), new tariff announcements have slowed (though tariffs remain), and uncertainty has fallen somewhat (though remains elevated). CUSMA was not extended by the July 1st deadline, and the timing and ultimate outcomes of renewal discussions remain unclear—but the agreement remains in place, ensuring continued tariff-free treatment for the vast majority of our U.S. exports. Signs of higher business investment are emerging in monthly import data, and the labour market seems to have picked up momentum again in recent months—especially in the weakest provinces. For the Canadian economy as a whole, we expect growth to average 0.8% this year, down from 1.9% in 2025. We see Quebec, Ontario, and B.C. growing by only around 0.5% this year, given their higher exposures to the economic headwinds. We expect other provinces to overperform the national average—especially the oil-producing provinces. For 2027, we forecast growth of around 2% or higher in all provinces, predicated on economic headwinds continuing to gradually abate, and business investment growth taking a firmer hold.

TARIFFS AND IMMIGRATION CHANGES WEIGHING ON ALL PROVINCES

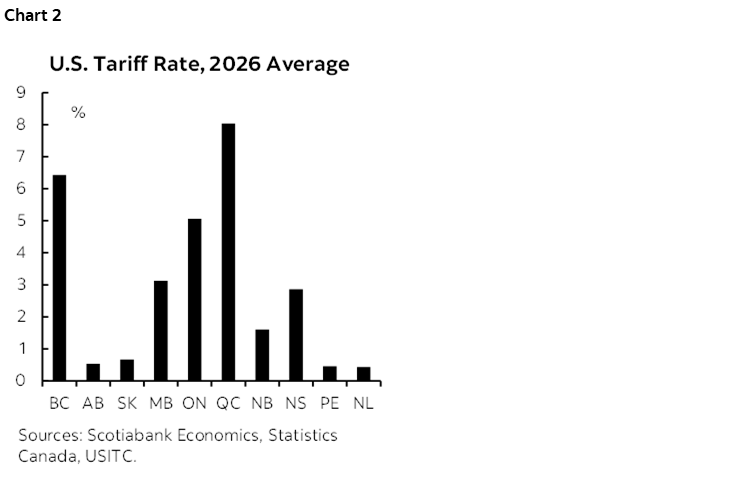

The U.S. sectoral tariffs continue to have significant impacts on some provinces. While the vast majority of Canada’s trade with the U.S. continues to occur on a tariff-free basis under CUSMA, the significant Section 232 tariffs on steel and aluminum, forestry, autos, etc. have continued into 2026 and the provinces with the largest concentrations of those industries are facing the biggest burdens. Quebec, with significant aluminum and aerospace exports, has seen an average U.S. tariff rate of 8% in recent months, with B.C. and Ontario also above 5% (chart 2). On the flip side, several provinces are seeing very little direct impacts from the tariffs, including the oil-exporting provinces. However, all provinces remain impacted by the uncertainty from the changing U.S. tariffs and discussions on CUSMA.

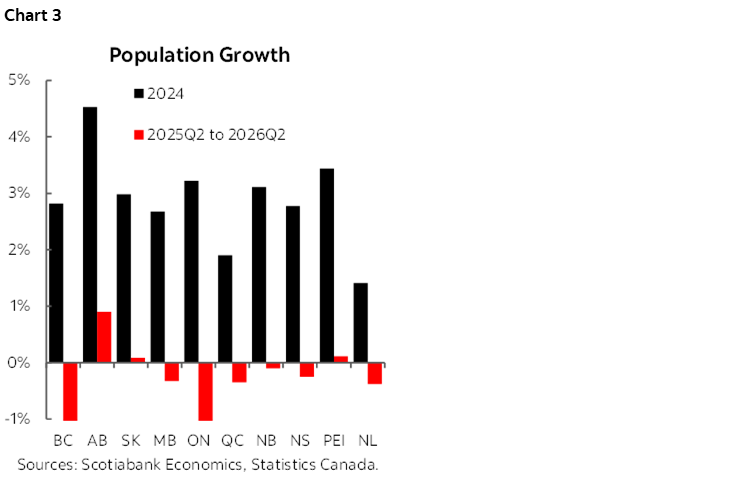

All provinces have also seen a sharp decline in population growth due to changes in national immigration policies. Compared to 2024, when Canada averaged nearly 3% population growth, over the last year population growth has been sharply lower in all provinces. Ontario and B.C. have seen population declines of 0.9% over the last four quarters, and most other provinces have seen essentially flat population growth (chart 3). However, Alberta continues to see above-average population inflows and has seen its population continue to grow (though at a much lower pace than in past years).

JOB GROWTH SLOWER, BUT UNEMPLOYMENT RATES TRENDING LOWER

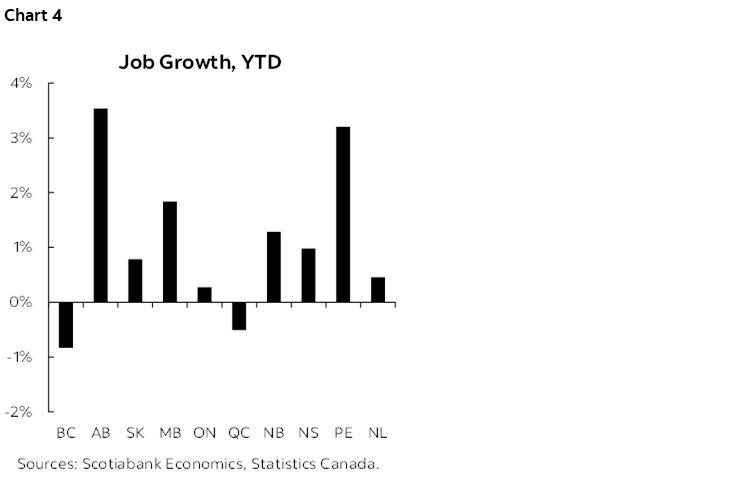

With sharply lower population growth and ongoing impacts from U.S. tariffs, job creation has naturally slowed in most of the country. Quebec and B.C. have seen a loss of total jobs compared to a year ago, and a number of other provinces have seen limited growth. However, several provinces have continued to see decent job growth over that period, especially in parts of the Prairies and the Maritimes where economic headwinds are weaker (chart 4).

Despite the slowdown in job growth, unemployment rates in most provinces have come down, reflecting the sharper slowdown in labour force growth. While monthly provincial unemployment rates are quite volatile given smaller sample sizes, seven provinces averaged a lower unemployment rate in the last three months compared to the last quarter of 2024—led by Prince Edward Island (PEI), Newfoundland and Labrador (NL), Manitoba, and Alberta, which each saw an improvement of more than 0.5 percentage points. We expect unemployment rates in most provinces to continue to trend lower through 2027, driven by modest job growth outperforming very limited labour force growth.

HOUSEHOLD CONSUMPTION SOFTENING

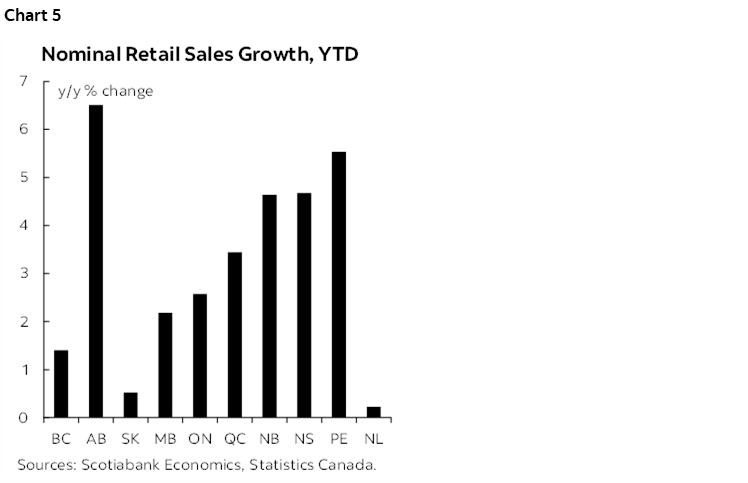

Household spending growth remains resilient. Consumer spending in Canada was surprisingly resilient in 2025—despite the significant tariff, uncertainty, and immigration shocks. Household consumption appears to have picked up further in 2026 in several provinces, especially Alberta and PEI, where nominal retail sales growth is tracking several percentage points stronger than last year, and above 5% overall (chart 5)—supported by the nation-leading job growth in those provinces. However, retail sales growth has slowed considerably in some provinces, and is likely negative on a real basis in B.C., Saskatchewan, and NL. That said, the interest rate cuts late last year and a pick-up in the labour market this year growth should support continued resilience in household spending. We expect the Bank of Canada to keep interest rate unchanged for most of 2026, though our latest forecast anticipates hikes starting toward the end of 2026 that return the overnight rate to 3% in early 2027, as we expect inflation risks to tilt to the upside with the economy getting on a stronger footing.

External factors are also impacting the consumption outlook. Following the increase in oil prices due to the conflict in Iran, retail sales data show that households increased spending on fuel but kept other spending constant, indicating that spending could normalize as oil prices drop. In part due to the lower oil prices, inflation should decline from 3.2% in May to around 2% by the first half of 2027, providing welcome relief to household purchasing power. Tariffs also continue to have impacts across supply chains and consumer prices. Canada’s recent tariffs on canned vegetables could increase food prices somewhat further, though the significant exemptions will mitigate the overall impact.

INVESTMENT GROWTH PICKING UP

Home sales started the year slower but have been bouncing back since April. Despite the significant economic uncertainty that emerged in 2025, the housing market activity was resilient and rose year-over-year in most provinces. However, activity dipped at the beginning of the year in all provinces, alongside a few weak months for the Canadian labour market. Fortunately, resale activity rose again in May and June alongside gains in the labour market, should continue to normalize over the course of the year—especially if the job growth remains positive, as we expect. In Ontario, new home sales will receive a special boost from the temporary HST rebate on new homes. However, the number of recently completed and unabsorbed dwellings remains elevated, which may portend further price adjustments in weaker markets.

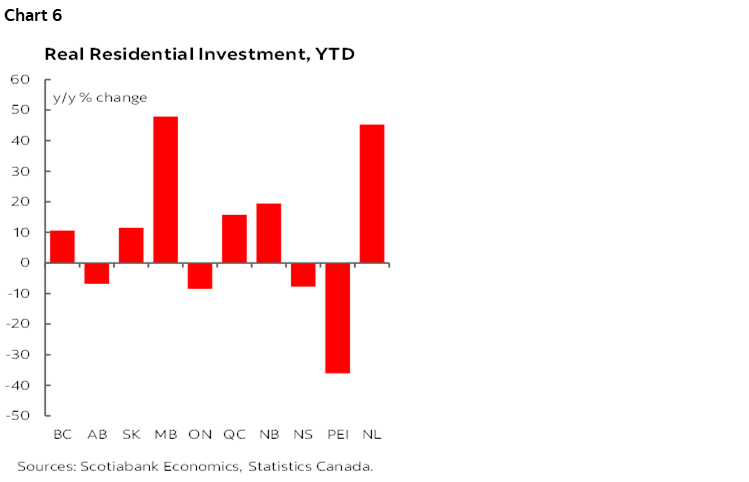

Residential investment is picking up. Real residential construction recorded its best month in April since late-2022, driven by continued strong growth in Quebec and Manitoba, a jump in B.C., and stabilization in Ontario. Overall, residential investment has been trending higher in most provinces, with the exception of some provinces normalizing after strong years in 2024 and/or 2025, including Alberta, Nova Scotia, and PEI (chart 6). Ontario is also lower year-over-year on average through April, though the province saw a pick-up in April, which is likely to continue given the recently announced HST rebate on new properties. Housing starts data point to stronger activity in most provinces compared to last year, indicating that residential investment should contribute positively to growth in most provinces this year. Lower interest rates, government measures, and lower uncertainty are working together to unlock some pent-up demand for housing, though lower immigration flows are also reducing some demand—especially in the largest cities.

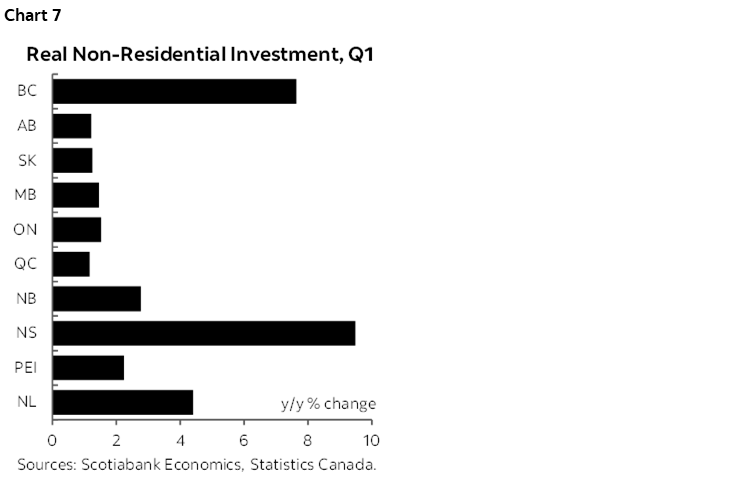

Non-residential investment is subdued but should rebound in the coming quarters. Business investment growth in Canada has been very limited for a number of years, and this has continued since the tariff shock. Higher government capital investment, alongside stable business investment, helped to keep overall non-residential investment growth modestly positive in all provinces in 2025. Early in 2026, that continues to be the story, with most provinces seeing modestly positive non-residential investment growth—aside from Nova Scotia and B.C., which have seen larger increases in public sector investment (chart 7). The ongoing tariffs and persistent uncertainty continue to weigh on new business investment but a modest abatement of uncertainty and the efforts to remove barriers to investment—especially for major projects—should result in business investment picking up momentum over this year and next. In addition, public investment should continue to grow, given stated intentions by the federal and provincial governments. Western Canada should see a particularly strong pick-up in investment, given the number and size of projects in that region already referred to the Major Projects Office—in addition to the Canada-Alberta MOU on energy issues, which could unlock even more. That said, there is still significant implementation risk that warrants caution in fully incorporating these into our baseline just yet.

EXPORTS REMAIN LOWER BUT SOME IMPROVEMENTS SEEN

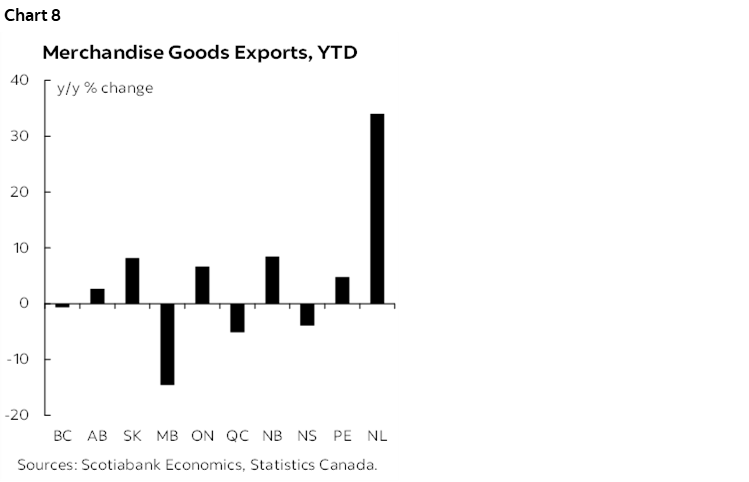

Exports continue to drag in most provinces. Lower exports, especially to the U.S., were a drag on growth in most provinces last year. Through the first five months of 2026, trade data indicate that could occur again this year, as half the provinces are tracking negative or very modest growth in the nominal value of exports (chart 8), and trade volumes are likely somewhat lower. Manitoba’s exports have been particularly weak, running 15% lower than the first four months of last year. On the flip side, NL’s exports are up more than 30%, thanks to higher oil prices as well as increased production that has been easily absorbed by the global oil market in the wake of supply disruptions in the Middle East. Ontario’s exports are also higher, despite the province facing one of the largest tariff burdens. We expect net exports to continue to drag on national growth in 2026 and 2027, though less so than in 2025. Some type of relief from the sectoral tariffs would boost prospects, though renewed turbulence is possible as discussions around renewing CUSMA advance—including potential U.S. threats to withdraw from the agreement entirely.

BRITISH COLUMBIA

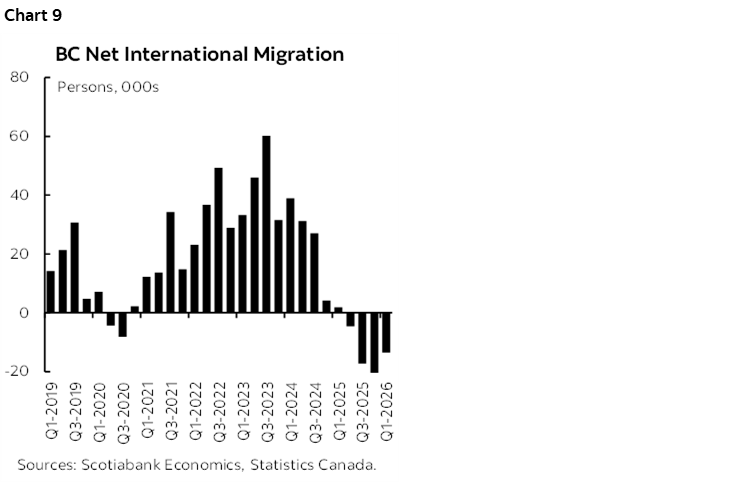

B.C. recorded estimated economic growth of 2% in 2025, led by real estate, health care, and natural resource extraction. This was achieved despite a slowdown in population growth from 2.8% in 2024 to 0.5% last year due to changes in federal immigration policy that has led to negative immigration flows for the past four quarters (chart 9) and declining total population in the past five.

While employment was quite stable throughout 2025, jobs fell by roughly 40k (or about 1.5%) early this year—driven by losses in retail trade and finance/insurance. This led the province’s unemployment rate to rise from 6.1% to 6.8%. However, 33k jobs were added across May and June, bringing the unemployment rate to back down to 6.5%. Nominal retail sales have been fairly stable since a significant rise in the second half of 2024, indicating that household consumption may only contribute modestly or even negatively to provincial growth in 2026 (and certainly less than it did in 2025).

Residential investment is on track to contribute modestly to growth in 2026. Home sales are lower so far this year, though ticked up a bit in May and June. Housing starts have been stable but are not clearly increasing, in part due to the impact on housing demand of the sharp drop in population growth. House prices in the Vancouver area have been trending lower since the end of 2024, and further price adjustments (especially in the condo market) are likely until supply and demand are better balanced—though the recent joint provincial-federal initiative to finance the conversion of unabsorbed condos into affordable rental housing could accelerate the restoration of balance. Non-residential investment could contribute more significantly to growth, especially in the medium-term. In the first quarter of 2026, public investment was up 8%, reflecting the provincial government’s elevated capital spending agenda, though business investment remained flat. We expect business investment to pick up over the course of this year and 2027, especially as B.C. is home to many potential new major projects—including six of the first 18 projects referred to the new federal Major Projects Office. Exports are slightly lower to start the year, led by declines in forest products, which continue to be impacted by U.S. tariffs on top of anti-dumping and countervailing duties, which can sum to over 50% on B.C. lumber exports.

Overall, we expect growth of 0.4% in 2026 and 2.1% 2027—somewhat lower than the national average in both years.

ALBERTA

Despite a drop in population growth from 4.5% in 2024 to 2.8% last year, Alberta’s real GDP growth is estimated to have slowed only slightly from 3% to 2.7% in 2025, led by growth in the oil and gas, construction, and agriculture sectors.

Job growth has accelerated to 3.5% so far in 2026, led by gains in health care jobs. In line with the pick-up in employment, retail sales growth has also accelerated—averaging 6.5% higher than early 2025. Home sales and residential construction trended lower over the course of last year after a very strong 2024, but appear to have bottomed out and started a recovery. Non-residential investment was modestly higher early in 2026 and should continue to pick up steam, given growing investment plans in the oil and gas sector in response to higher oil prices and an improved regulatory environment. However, it will take time for the large projects advancing under the Canada-Alberta MOU to have an impact on overall economic growth.

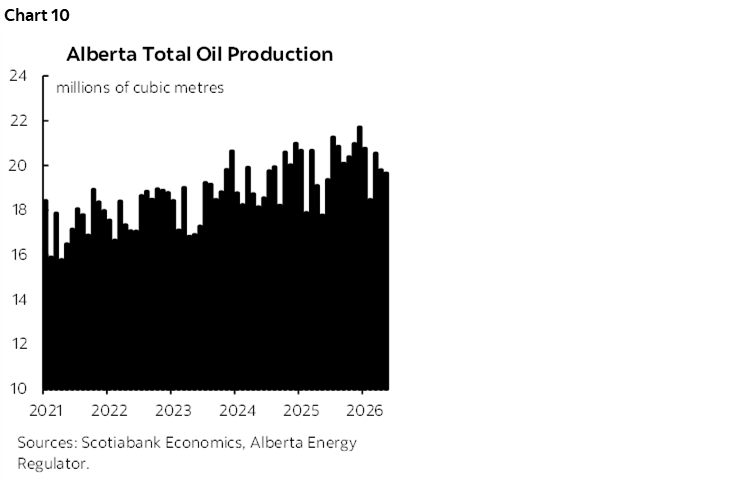

Alberta’s exports are slightly higher so far this year, in part due to LNG Canada Phase 1 continuing to ramp up operations—leading LNG exports to Asia to rise sharply (though they remain small compared to energy exports to the U.S.). The rise in oil prices is a boon for the province, though prices have come down since May, and there has not been a significant ramp-up in production in response to the higher prices (chart 10).

We expect provincial growth of 2.5% in 2026, 2.9% in 2027—significantly above the national average in both years.

SASKATCHEWAN

Saskatchewan’s economy grew at a solid 2.2% rate in 2025, led by 16% growth in agriculture and 9% growth in construction.

Employment was stable in the second half of 2025 but has dipped somewhat in recent months, led by retail jobs (following some weakness in retail spending). After having fallen to 4.5% in 2025Q2, the province’s unemployment rate has risen to 6% a year later—though it remains lower than the national average.

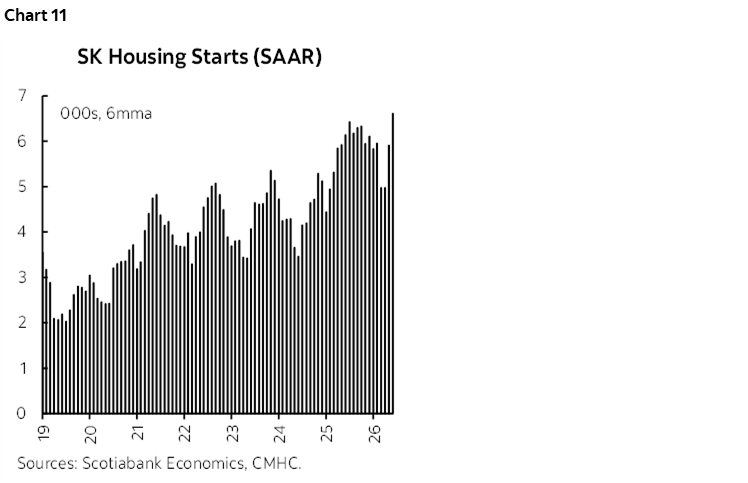

While population and labour force growth have slowed, they remain higher than for Canada overall, helping Saskatchewan maintain above-average potential growth. In addition, business investment growth is likely to continue to strengthen, due to the ongoing construction of the world’s biggest potash mine through 2029, and the potential addition of the Foran Copper Mine—which was one of the five first projects referred to the Major Projects Office. Residential investment is also helping to support growth, and housing starts have rebounded again after a dip early in 2026 housing (chart 11). The higher oil prices are also positive for Saskatchewan, though its production is only about 10% that of the level of its Western neighbour—and also does not appear to have jumped in response to the higher oil prices.

Overall, we expect the Saskatchewan economy to grow 1.8% in 2026 and 2.5% in 2027—above the national average in both years.

MANITOBA

Manitoba’s economy grew by 1.3% 2025, led by 9% growth in agriculture and 5% growth in construction.

Many indicators point to a pick-up in growth in 2026, including a 1.8% increase in jobs so far this year, and an even stronger 2.5% increase in hours worked—led by strong job growth in the construction sector.

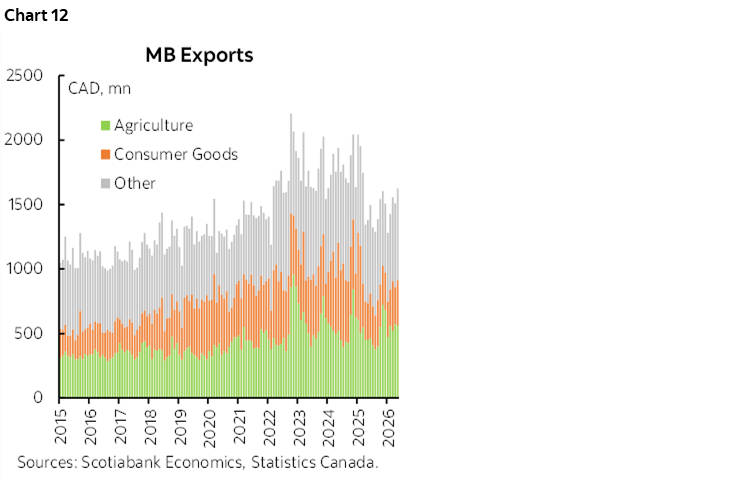

Residential investment is up 48%, and housing starts are up 38%—suggesting a strong contribution from housing (for both growth and employment) for the remainder of the year. However, retail sales are a bit weaker than the national average, and the province has seen a large drop in exports since early 2025 (chart 12). Manitoba has above-average exposure to the U.S. tariffs given its diversified economy, and has experienced a drop in exports in many of the sectors targeted by the U.S., including auto manufacturing, metals, and forestry. Fortunately, the province’s largest export category, agriculture, has been stable—and is up 5% so far this year.

We expect growth in the Manitoba economy of 1.5% in 2026 and 2.1% in 2027.

ONTARIO

The Ontario economy grew 1.3% in 2025, with contributions coming almost exclusively from the service side of the economy—led by 5% growth in the finance and insurance industry. The manufacturing sector shrunk by 1.6%, in part due to the U.S. tariffs on a number of key Ontario exports, including steel and autos.

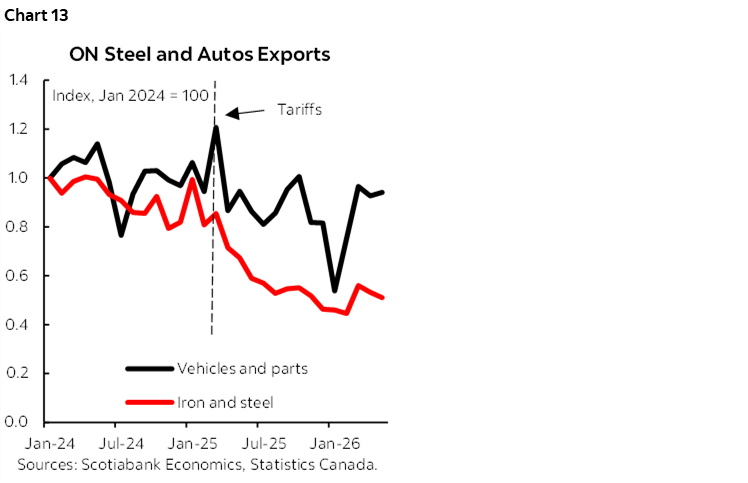

The province’s economy was running 0.5% lower year-over-year in the first quarter of 2026, following its third contraction in the last four quarters. Data for Q2 is looking more positive and we expect the province to record positive growth for the year overall. Employment has bounced back after falling in Q1, and the unemployment rate has dropped to 7.0%—the lowest level in two years. Retail sales have picked up lately, and exports continue to rise. While housing starts remain low compared to 2021–2023, they have been gradually trending higher for the past year. In addition, the temporary HST holiday on new homes appears to be significantly boosting new home sales, which should spur an acceleration in housing starts and help to bring down unabsorbed inventories of condos. However, business investment has remained subdued, and the exports of steel remain about 50% lower than before the tariffs (chart 13). However, exports of some other affected goods, including vehicles and parts (which are five times as large as steel exports), have largely recovered—reflecting the integration of supply chains that can’t be changed quickly.

Ontario continues to face some of the largest burdens of the trade and immigration shocks, given the provincial economy’s significant linkages with the U.S. and its tradition as a destination for many newcomers to Canada. We expect the province to grow 0.5% in 2026 and 2.0% in 2027—slightly below the national average in both years.

QUEBEC

Quebec’s economy grew by only 0.6% in 2025—by far the weakest performance of the provinces last year—weighed down by a 4% contraction in the manufacturing sector. The province’s economy expanded in Q1, after contracting in two of the previous three quarters, bringing its year-over-year growth rate up to –0.2%.

Employment and hours worked have both fallen somewhat, but the unemployment rate held fairly stable in the 5.5%–6% range, due to a drop in population driven by the federal immigration policy changes. Despite the weak labour market readings, consumer spending and residential investment have continued to grow steadily—and even accelerated in recent months.

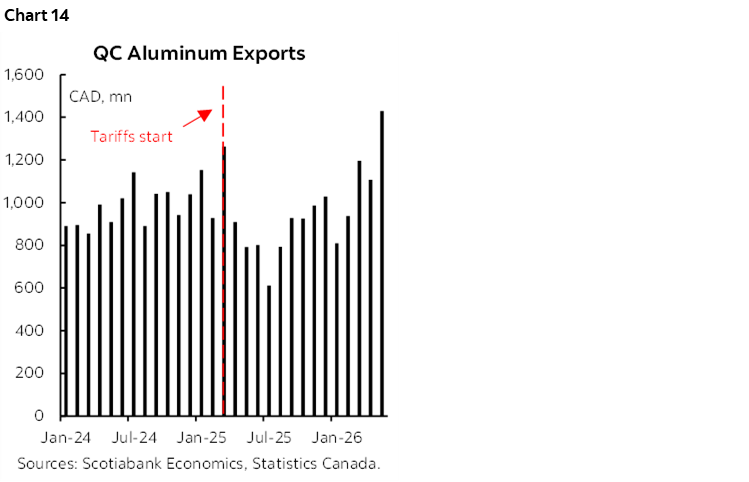

However, total exports remain lower, despite aluminum export values rebounding due to recovering U.S. demand as well as new demand from Europe (chart 14). In addition, non-residential investment remains subdued, despite growing public sector investment.

The U.S. tariffs and the ongoing slowdown in population growth continue to weigh on the Quebec economy, though we expect growth to pick up over the course of 2026 and into 2027. Overall, we see Quebec underperforming the national average, with growth of 0.4% in 2026 and 1.8% in 2027.

MARITIME PROVINCES

All three of the Maritime provinces grew faster than the national average in 2025, with PEI recording the second-best growth rate at an impressive 2.8% (following its nation-leading 3.8% growth in 2024).

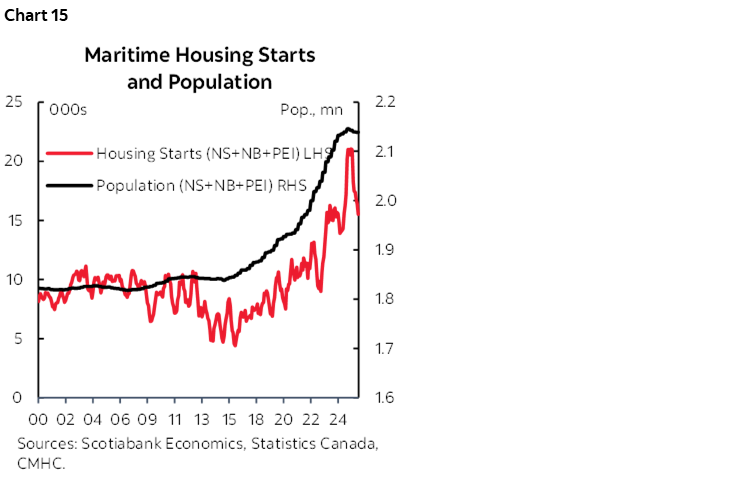

So far in 2026, growth in the region appears to have slowed somewhat, though not as much as in Central Canada and B.C. Employment growth is positive in all three provinces, and retail sales growth has been solid. Home building continues at elevated levels, though has slowed somewhat in Nova Scotia and PEI in recent months after a particularly strong second half of 2025 (chart 15). With population growth much lower, housing starts are likely to contribute somewhat less to growth, but rising non-residential investment could provide an at least partial offset. Nova Scotia in particular is likely to see benefits from the significant increases in federal defence spending.

Exports in the region have also been fairly resilient, reflecting the region’s lower-than-average exposure to U.S. tariffs and the removal of the Chinese tariffs on seafood, though Nova Scotia is tracking a decline in exports through the first five months of the year.

We expect growth rates in the Maritime provinces to moderate somewhat this year, but remain above the national average of 0.8%, before picking up to around 2% next year.

NEWFOUNDLAND AND LABRADOR

Despite both employment and hours worked contracting in 2025, Newfoundland and Labrador’s economy led provinces with growth of 3.5% last year, led by 15% growth in the oil and gas sector.

Both employment and hours worked have returned to modest growth so far in 2026, and both residential investment and exports are up strongly. Countering these positive forces are nominal retail sales up only 0.2% (likely somewhat negative in real terms) and non-residential investment down by double digits.

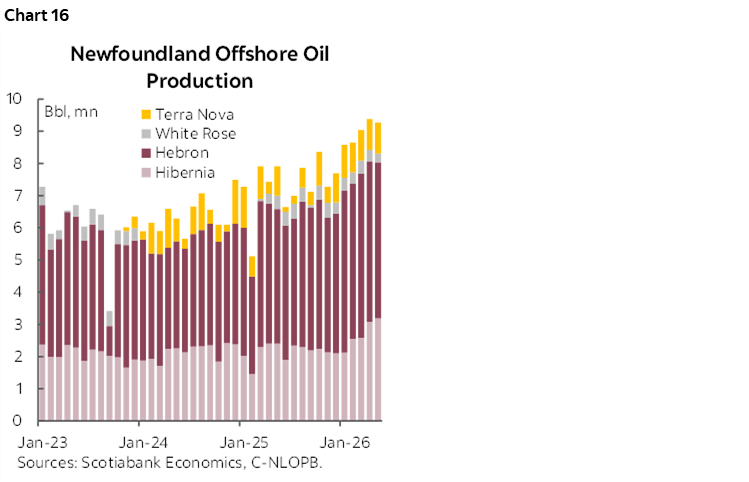

However, oil production has accelerated further, and is up 26% so far this year (chart 16)—helping NL take full advantage of the higher oil prices. This renaissance in the province’s oil production is likely to be temporary, with most industry watchers expecting somewhat lower production in the next couple of years. However, medium-term growth prospects could be boosted by the proposed Bay du Nord offshore oil development as well as the expansion of the Churchill Falls hydroelectric facility—assuming NFLD and Hydro-Quebec can come to an agreement.

Overall, we expect the growth in the province to be strongly above the national average this year at 2.7%, before moderating to 2.0% next year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.