HEALTHY FINANCES, POISED TO BENEFIT FROM HEFTY US EXPANSION

- New Brunswick’s control of COVID-19 helped its economy last year; further success to date this year bodes well for growth in 2021.

- Key export commodities are poised for very strong gains this year.

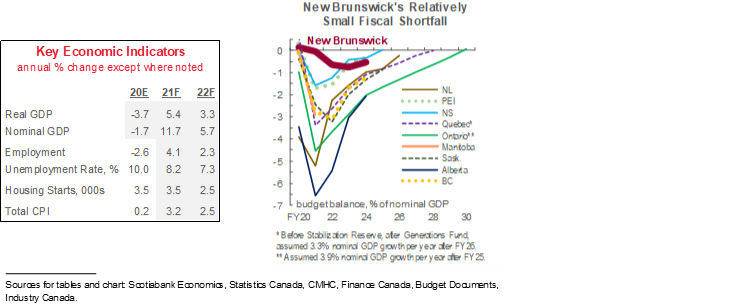

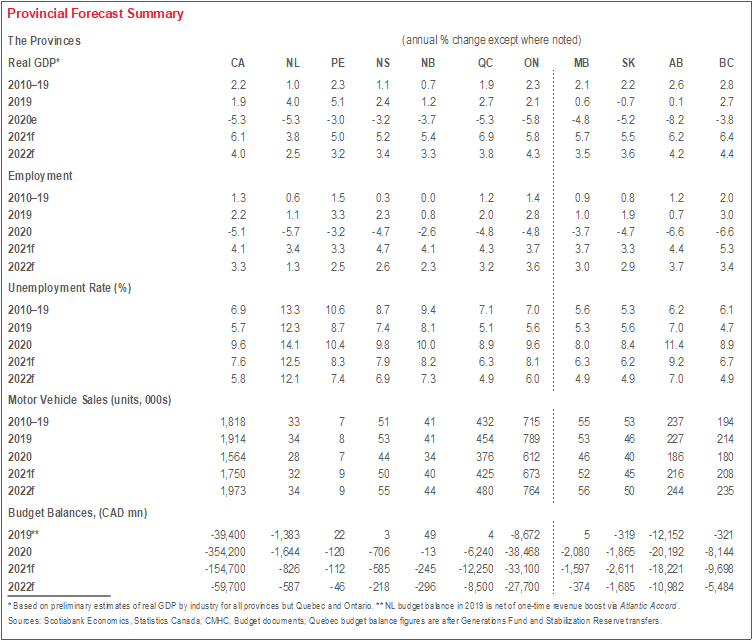

The preliminary estimate of a 3.7% real GDP decline in New Brunswick last year was one of the smallest of any Canadian jurisdiction, and mirrors its successful containment of COVID-19. The only jump in infections witnessed to date in the province occurred in January of this year; other than that period, New Brunswick has consistently maintained one of the lightest caseloads and some of the least restrictive lockdown measures of any region in Canada. At the time of writing, the province had reached the 75% first dose vaccination rate threshold necessary to begin the first phase of its reopening plan. As part of its economic recovery strategy, the province is providing financial incentives for visitors from other Atlantic provinces.

The benefits of successful virus containment are evident in the relatively modest budget deficit and net debt increases outlined in New Brunswick’s 2021–22 budget. Read our full analysis here. The province is the only one in Canada with projected fiscal shortfalls under 1% of nominal GDP in every fiscal year through FY24. Infrastructure outlays—per the province’s Capital Budget released late last year—are set to increase by more than 12% this fiscal year.

We expect base effects to limit the province’s top-line pace of expansion this year. Because of a softer-than-average decline in 2020, the rebound’s effect on economic growth is less significant.

Upgraded crude oil is by far New Brunswick’s largest export commodity; strengthening US fuel consumption and rising prices therefore bode well for incomes and profitability in the province. Those effects are already reflected in hefty 43% y/y ytd growth in nominal petroleum refinery exports through April 2021.

Forest products are another key New Brunswick export industry and should also contribute significantly to provincial growth this year. North American lumber and panel prices remain near all-time records, and we expect demand to remain sturdy amid the strongest levels of US homebuilding since before the GFC. Kraft pulp values continue to benefit from greater tissue paper and packaging use during the pandemic. Upgrades to the St. John pulp mill continue through 2022 and should support short-run capital investment as well as long-run production capacity.

We highlight two developments that may drive economic growth over the longer-term. The first is the potential development of a small modular reactor industry—currently receiving financial support from Ottawa and the province. The second is the $3–4 bn Mactaquac dam refurbishment plan, though the majority of capital costs are not expected to be incurred until the latter half of this decade.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.