REMAINING PRUDENT AFTER STAVING OFF WORST OF THE PANDEMIC

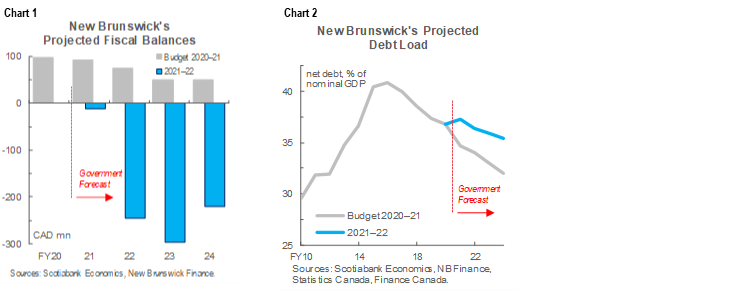

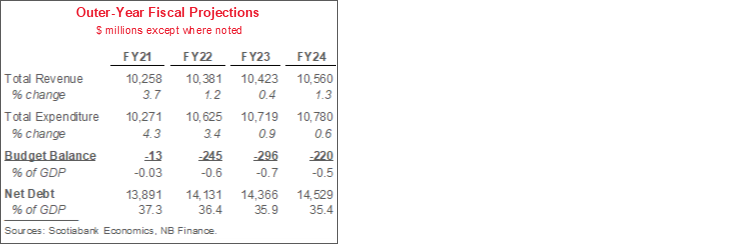

Budget balance forecasts: -$12.7 mn (-0.03% of nominal GDP) in FY21, -$245 mn (-0.6%) in FY22, -$296 mn (-0.7%) in FY23, -$220 mn (-0.5%) in FY24 (chart 1).

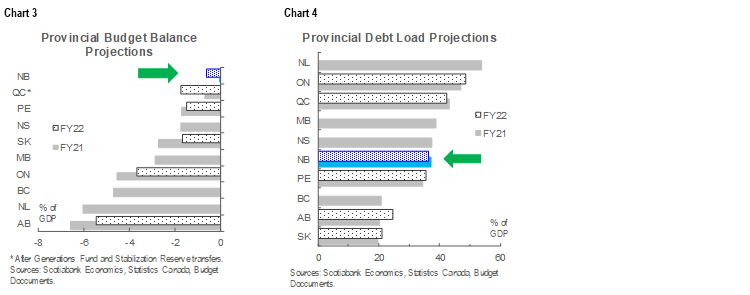

Net debt: expected to decline from 37.3% in FY21 to 35.4% by end-FY24—a slightly higher trajectory than forecast in last year’s budget (chart 2).

Nominal GDP growth: -2.5% in 2020 and +4.2% this year, which puts the provincial economy on track to reach to its pre-pandemic level in FY22.

Borrowing program: $1.85 bn in FY22, of which $1.4 bn was apportioned to long-term borrowing, and $150 mn is associated with the New Brunswick Finance Corporation.

We assess Budget to be a very prudent fiscal plan that leaves room for upside and also maintains New Brunswick’s healthy fiscal position relative to most Canadian jurisdictions.

OUR TAKE

In this first multi-year fiscal plan since the province’s first virus case, we see that COVID-19 has significantly impacted New Brunswick’s finances. Stable surpluses of 0.1–0.2% of GDP had been pencilled in for FY21–24 in the last fiscal blueprint; the government now anticipates deficits for the next three years.

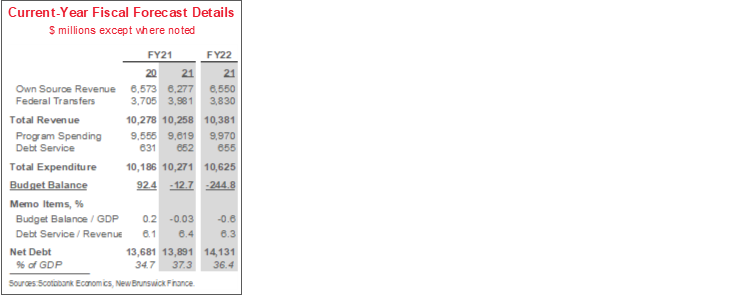

The base case outlook sets New Brunswick up to maintain a strong fiscal position relative to most of its provincial peers. The GDP drop last year is widely accepted to have been much shallower than the national average; that reflects successful containment of the virus and kept FY21 revenues relatively unscathed versus last year’s plan. With expenditure growth of 4.3% expected in FY21—slightly higher than last year’s forecast—New Brunswick has thus far projected the smallest deficit of any Province this year and next (chart 3, p.2). The manageable and declining net debt-to-GDP ratio likewise puts New Brunswick in a solid position relative to other jurisdictions (chart 4, p.2), leaves room to address unexpected costs and should assuage potential creditor fears about debt loads.

Conservative revenue forecasts underlie fiscal plan projections, and leave room for budget balance upside. The 2.9% real GDP growth projection for 2021 is almost one ppt below the private sector mean at the forecast cut-off time, and well below our latest update that incorporates more robust US stimulus. Total revenues are forecast to rise at an average rate of less than 1% over FY22–24—the softest three-year advance since at least FY94. That reflects expected easing of economic growth towards its long-run trend after this year as well as a drawdown of pandemic-motivated, conditional federal transfers that boosted taxable incomes in 2020. If stronger-than-anticipated growth does occur, the use of additional windfalls should be carefully considered.

Budget also sustains pre-pandemic plans for expenditure control. Mean total spending gains of 1.6% are built into FY22–24. That is slightly lower than the 1.9% anticipated over that period in last year’s budget, largely on the back of more significant outer-year restraint. Achieving the targets beyond FY22 may prove challenging in light of the anticipated population and price gains, though any revenue upside could provide room to ease the degree of planned spending restraint. The province also kept total spending growth below the rate of inflation plus population growth in 2019 (chart 5).

Policy supports are incremental and targeted. Wage raises for home support workers, money for Regional Health Authorities, and funds to address ongoing COVID-19 costs seek to bolster a health care system grappling with the pandemic and an aging population. Some $1.7 mn for online learning and an extra 75 cent/hour bump in early childhood educators’ salaries aim to ease transitions in the educational sector. Housing affordability plans—Saint John and Moncton had the tightest supply-demand balances of all Canadian cities last month—are anchored by National Housing Strategy home building goals. Efforts to attract and retain skilled newcomers and diversify trade rightly continue, though we expect New Brunswick’s staple industries to gain from a surge in US growth this year. Infrastructure spending increases were announced in December.

New Brunswick’s FY22 borrowing program is estimated at $1.85 bn. That figure includes $1.4 bn related to long-term borrowing, and $150 mn for the New Brunswick Municipal Finance Corporation.

In all, we assess Budget to be a prudent fiscal plan that leaves room for upside and also maintains New Brunswick’s healthy fiscal position relative to most Canadian jurisdictions. Provincial fiscal planning should eventually provide concrete timelines for balancing the budget once the pandemic has passed. For now, given the present level of uncertainty, we approve of efforts to bolster the economic recovery and keep debt loads on a downward trajectory.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.