NO SURPRISE: ANOTHER STRONG MONTH FOR CANADA’S HOUSING MARKET!

SUMMARY

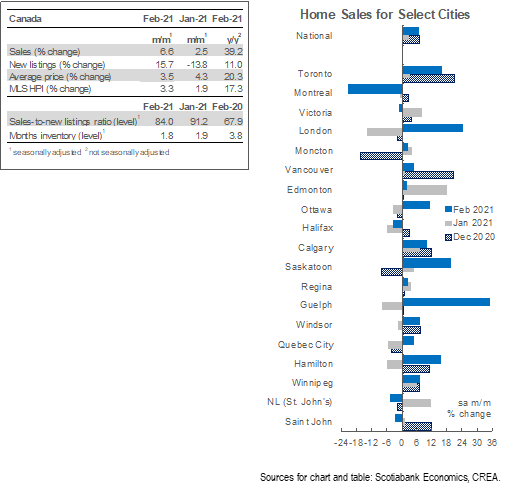

February saw Canadian home sales rise by 6.6% (sa m/m) while listings rebounded by 15.7% (sa m/m). This month’s increase in sales sets yet again another record, but it is accompanied by a welcome increase in listings. The national-level sales-to-new listings fell to 84% from the record reading of 91% in January in which all the markets we track recorded their highest ratio on record. The composite MLS Home Price Index (HPI) rose 3.3% (sa m/m), reflecting the sharp increase the sales-to-listing ratio seen in recent months. Two-storey single-family homes continue to be the main driver of this price appreciation, while apartment prices remain relatively close to pre-pandemic levels.

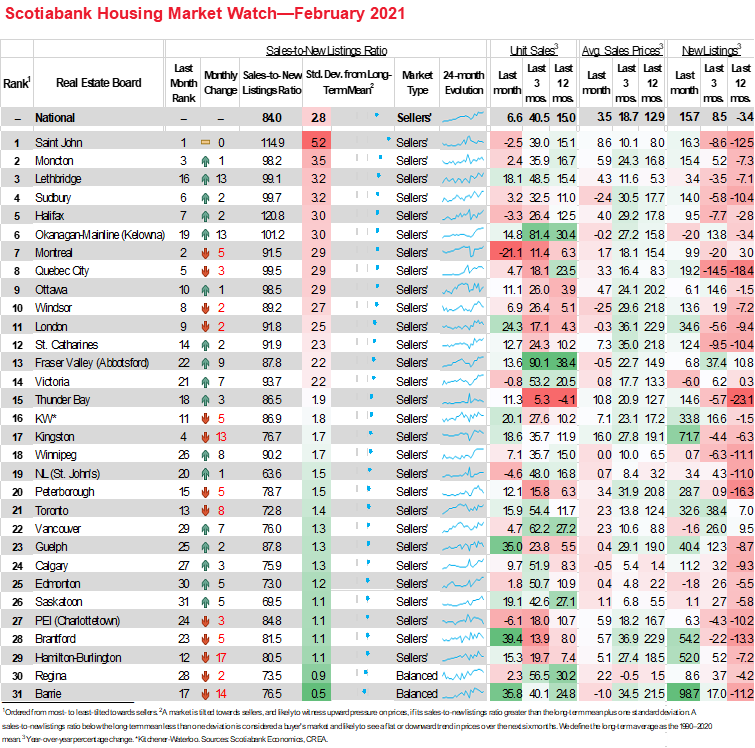

Sales gains continued to be broad-based and felt across much of the country relative to a year ago. The very few markets that experienced a decline from last year were areas with extremely limited supply. Of the 31 local markets we monitor, 30 witnessed sales gains this month compared to February 2020. The exception is Montreal. Compared to January 2021, 25 markets witnessed sales gains, driven mainly by Ontario regions, with Barrie, Guelph, and Brantford averaging almost 36% (sa m/m)—these more than offset the 21% (sa m/m) decline in Montreal.

Listings have rebounded to recoup all of January losses, but months of inventory remain at a record low. New listings increased in 27 of the 31 centres in our list. The areas that witnessed the highest increases in listings are also those that witnessed high sales gains—an indication of the tightness in the market, whereby any new listings are absorbed immediately. The bigger gain in listings compared to sales in February relaxed the sales-to-new listings ratio, from its record-breaking high last month to its second highest level on record (84%), with 29 of our markets being in sellers’ territory. At the current rate of sales activity, national inventories would be liquidated in 1.8 months—the fastest rate on record. Months of inventory were the lowest on record in four provinces, with Ontario having less than a month of inventory.

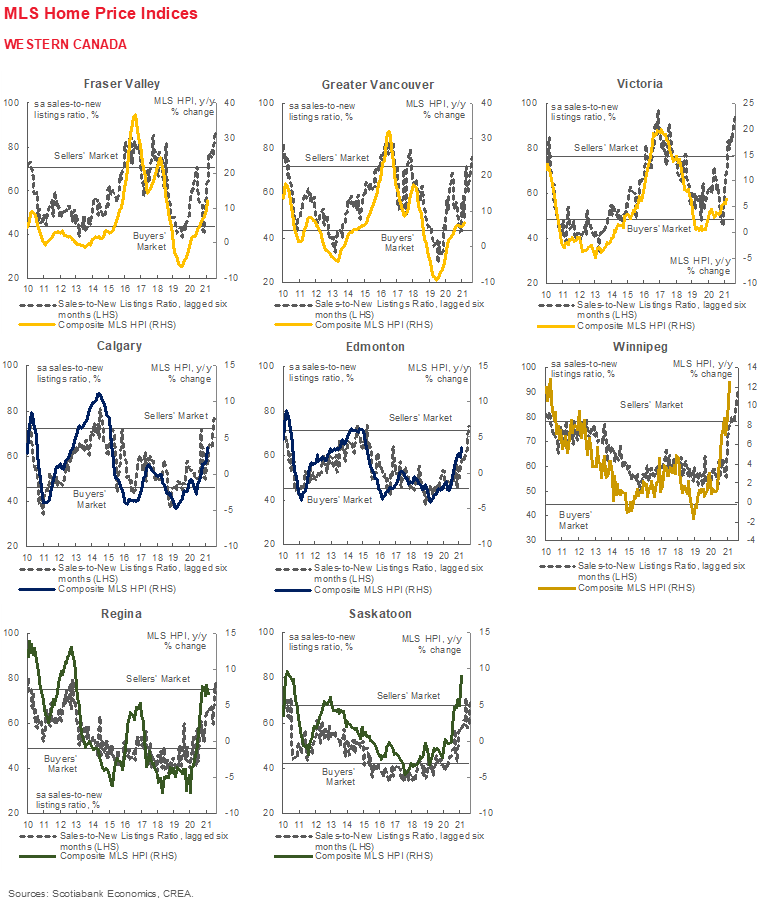

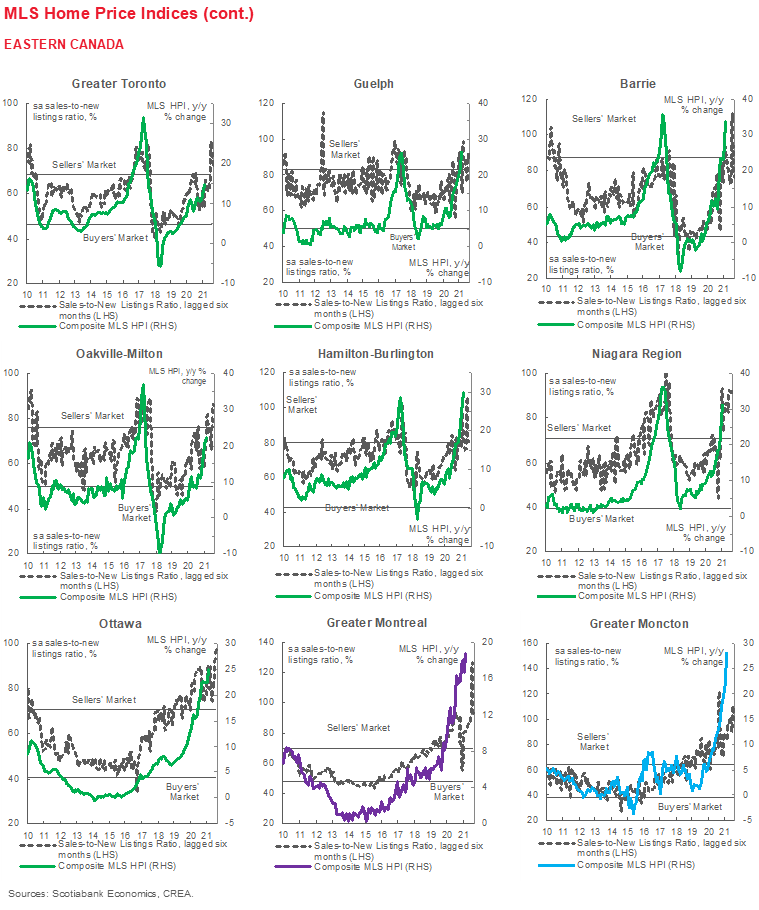

Single-family homes continued to drive growth in housing prices. With a 17.3% (nsa y/y) increase in the composite MLS HPI for all homes in Canada, single-family homes recorded a 22.1% (nsa y/y) increase, considerably outpacing the apartment market which saw an increase of 4.2%. February saw an uptick of 1.6% (sa m/m) in the MLS HPI for apartments, the highest increase during the pandemic and since March 2017—perhaps a result of their now relative affordability compared to other homes.

IMPLICATIONS

The February data suggests the stronger-than-expected trend in the housing market witnessed over the course of 2020 is continuing into 2021 despite the lockdown measures in place early this year. With the Canadian housing market still showing signs of significant undersupply, we are likely to continue to see even further price gains in the months ahead.

Buyers continue to demonstrate a preference for more space as the pandemic and its impact on living and working conditions persist—with more spacious homes driving much of the increase in the composite MLS HPI. Data from the Toronto Regional Real Estate Board released earlier this month demonstrates this trend clearly. While housing conditions were tight across the entire GTA market in February, an almost 15% (y/y) increase in average selling price was mainly driven by annual rates of increase above 20% in the detached, semi-detached and townhouse market segments in suburban areas surrounding the City of Toronto. Whether this trend will continue depends largely on whether this pandemic alters working arrangements after vaccination becomes more widespread.

Incoming data continue to point to very robust GDP growth that might recover COVID losses and close the output gap by the end of the year. Canadian job gains in February almost recouped all the job losses of the previous lockdowns for the months of December and January. Add to that an acceleration in vaccine rollouts in Canada and the US, the long-awaited imported benefit from the US fiscal stimulus, and the likely additional stimulus to be announced in Canada’s spring federal budget. This points to a strong recovery and economic growth during the year, even as the risks for a third wave and virus variants remain. While improved conditions will add steam to the housing demand engine, they should also bring sellers off the sidelines and facilitate more housing starts, easing the present supply-demand tightness. At the same time, they point to earlier rate hikes than previously announced by Canada’s central bank. We expect a further tapering of the Bank of Canada’s quantitative easing program in April, and we further expect a rate hike from the Bank of Canada by Q4-2022. Fixed mortgage rates are already ticking up given the steepening of yield curves resulting from improved growth prospects. This may encourage buyers to rush to join the market to lock in a lower rate.

Strong population growth will continue to drive housing demand in the medium term—an increase in Canada’s immigration targets over the next two years points to a stronger population growth, but achieving these targets will largely depend on global vaccination progress and removal of border restrictions. International migration trends should be monitored in parallel with new household formations and internal migration, which plays a significant role in housing demand patterns and prices. A report by CMHC on the impact of migration on Canada’s housing markets saw that up to 2019, out-migration from Toronto and Vancouver materially influenced prices upwards in neighbouring areas and other CMAs. Policy makers will have to monitor migration patterns as we emerge from the COVID pandemic to better assess how to respond in adjusting supply.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.