LIFTED BY OIL PRICE GAINS

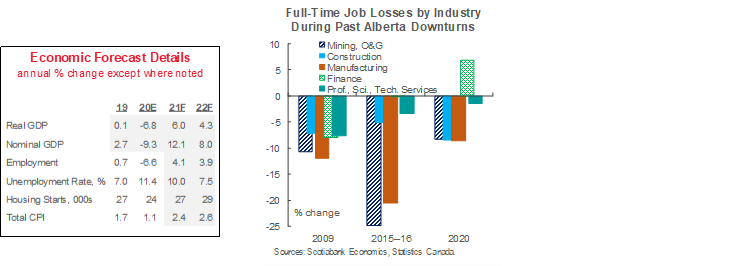

Alberta experienced the deepest recession of any province last year as it dealt with the effects of COVID-19 and a plunge in oil and gas activity.

Rising crude values to begin this year bode well for a solid rebound in 2021, but the pandemic extends recovery from the last downturn to eight years.

For non-energy industries, petrochemicals and forestry face the best near-term prospects, but full economic diversification remains a long-run goal.

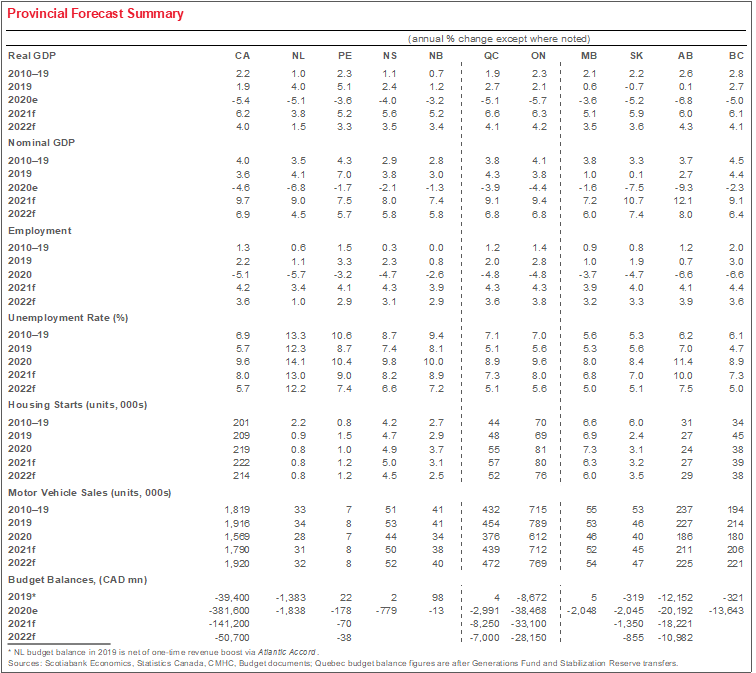

Alberta was harder-hit than any other provincial economy in 2020, a result of its oil and gas industry intensity. It witnessed the steepest drop in wages and salaries last year, the second-largest reductions in hours worked and active businesses, and as of January, its full-time workforce was further from its February 2020 peak than any other jurisdiction. Crude production fell by 5%—more than in 2016 at the height of the last commodity price correction—and drilling activity at one point reached an all-time low, driving a 38% decline in oil and gas investment at the national level in 2020.

As in prior economic downturns, the oil and gas downturn extended to adjacent industries (chart). Full-time employment declines in construction, manufacturing, and professional, scientific, and technical services reflect the role played by energy in generating business for firms in those sectors. Commercial building outlays continue to be held back by the supply overhang accrued since the last oil price downturn.

The surge in crude values to begin 2021—which prompted an upward revision to our price forecast—bodes well for a recovery this year. Crude output rose above year-earlier levels in November and December 2020, and should see further increases following the end of curtailment. With improving fuel demand, egress capacity will likely once again become a factor—we expect the eventual completion of the Line 3 and TransMountain Extension conduits to assist in this respect. Still, investment will likely stay below pre-pandemic levels for at least a few years; the pace and direction of an eventual Biden climate agenda poses additional risk. All told, we do not expect the province to reach the peak GDP it hit before the last oil price downturn until 2022.

Outside oil and gas, petrochemicals and forestry have strong prospects. Chemical manufacturing investment intentions are nearly 25% higher than preliminary estimates for last year, supported by work at the Heartland Petrochemical Complex. Forest product exports should benefit from strong lumber prices and housing market activity. The agricultural outlook is more mixed. Beef production will likely rise this year given early 2020 COVID-19 plant shutdowns. Wheat output could reasonably be expected to ease after stronger-than-average yields in 2020, though prices remain elevated alongside those of oilseeds. Stepped-up FY22 capital outlays concentrated in municipal infrastructure will likely lend further support to the province’s expansion. A number of renewable projects dot the economic landscape.

Budget 2021 announced several new economic diversification initiatives. These include: attraction and development of skilled workers in the technology industry, plans to boost agricultural investment, and efforts to reduce FinTech regulatory burdens. These efforts could help guard against future downturns, but will take time to bear fruit.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.